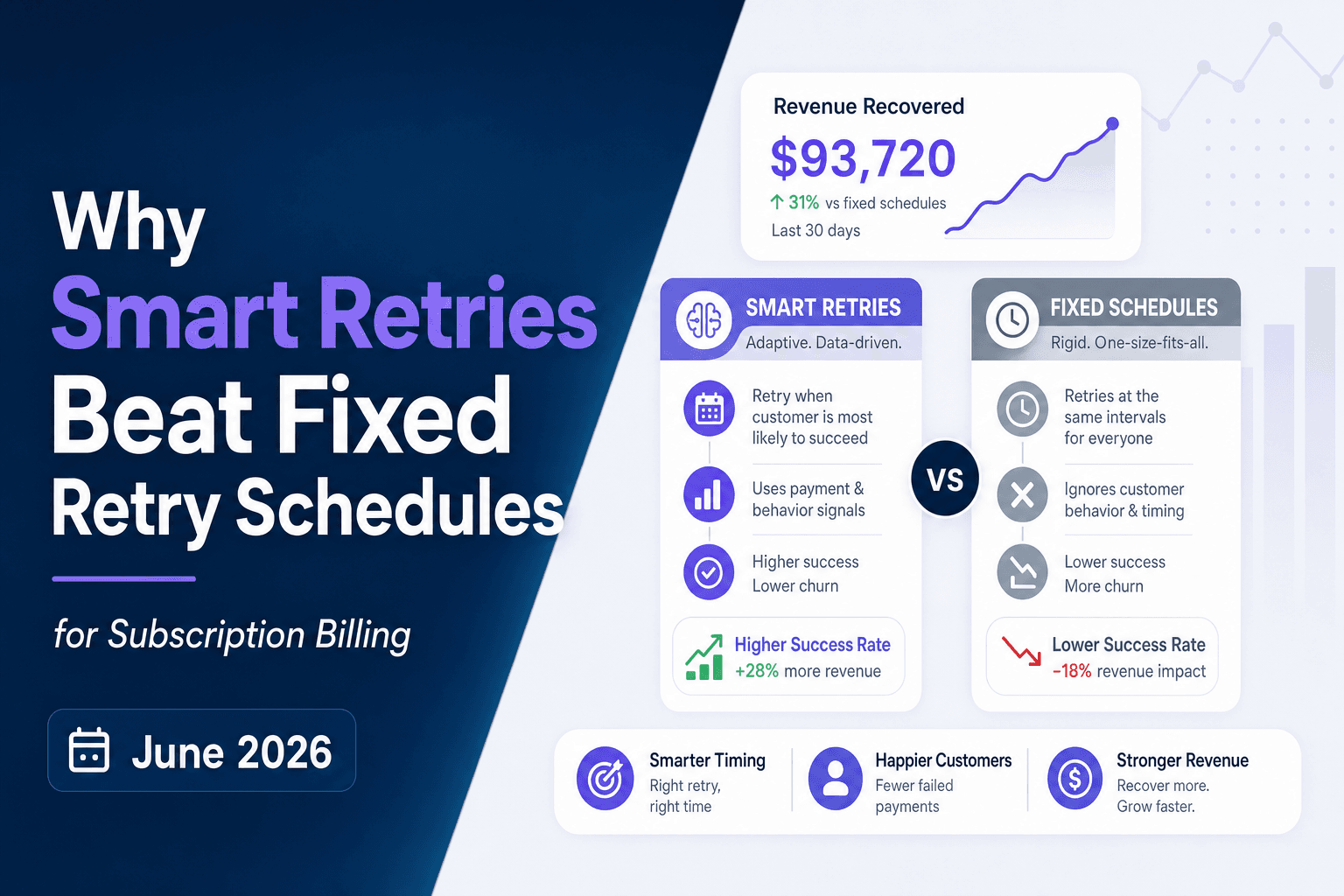

Why Smart Retries Beat Fixed Retry Schedules for Subscription Billing (June 2026)

Most subscription billing teams run a fixed retry schedule. Same intervals, same cadence, every failed payment treated identically. The problem is that a card declined for insufficient funds behaves nothing like one flagged for suspected fraud. Smart retries read the decline code before deciding when to retry, how many times to retry, and when to stop entirely. By matching retry timing to failure type and respecting card network limits, you avoid wasted attempts on unrecoverable declines and concentrate retries where they'll actually convert. The revenue impact at scale is the difference between recovering 40% of failed payments and recovering 70%.

TLDR:

- Smart retries recover 70 to 85% of failed payments versus 40 to 60% for fixed schedules by analyzing over 40 variables per transaction.

- Fixed retry schedules risk card network penalties up to $25 per excessive retry and can trigger merchant ID suspension.

- Smart retries classify declines as soft (temporary) or hard (permanent) and stop retrying unrecoverable failures.

- At 10,000 monthly failures averaging $50, smart retries recover roughly $75,000 more per month than fixed schedules.

- Slicker deploys in five minutes with no code changes and proves 20 to 50% recovery lift through AA/BB testing before you commit.

How Smart Retries Classify Payment Failures

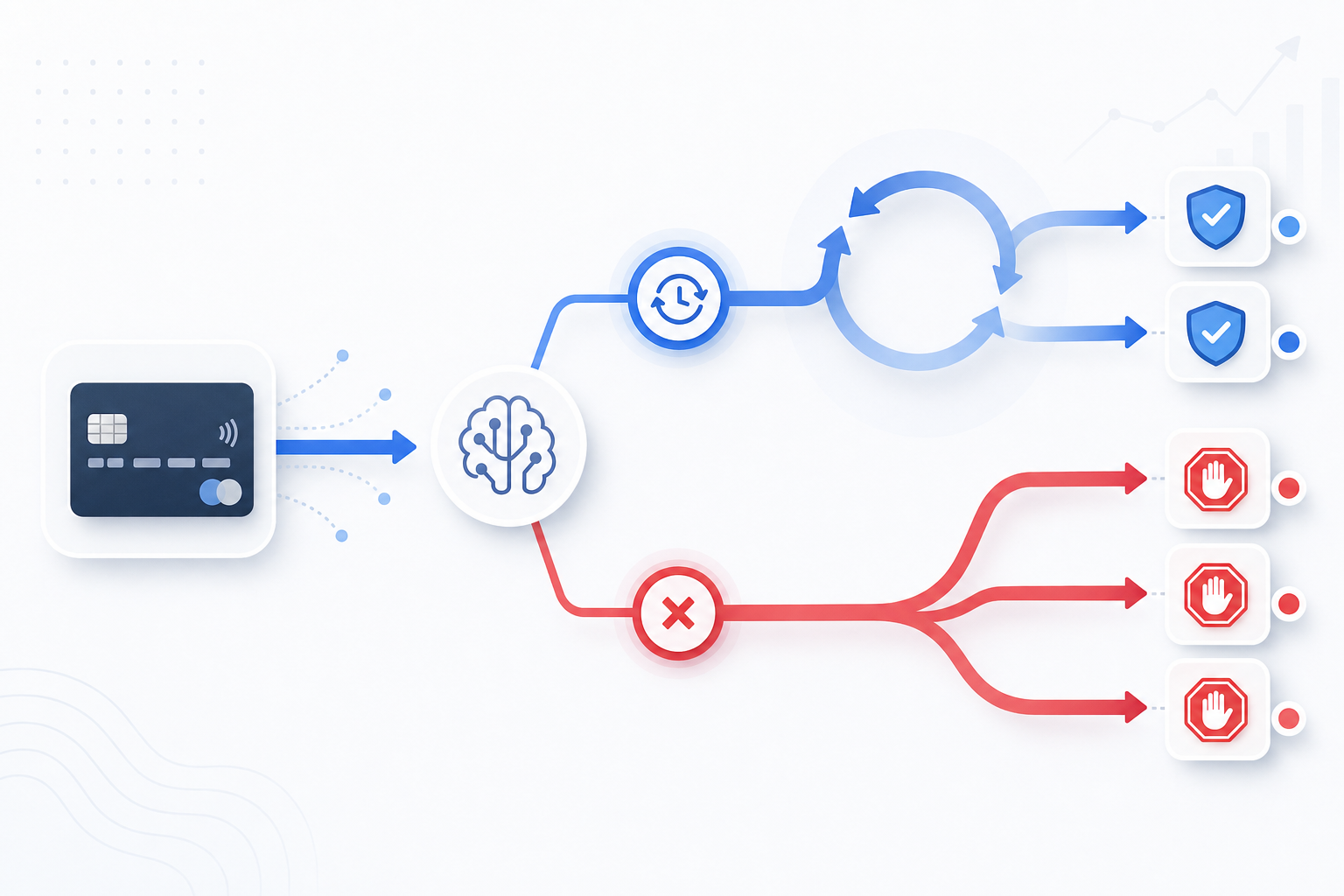

Not all payment failures are the same, and treating them as if they were is where fixed retry schedules break down. Smart retries start by reading the decline code returned by the issuing bank and sorting each failure into one of two categories.

Soft declines are temporary. Insufficient funds, a momentary network timeout, or a processor hiccup all fall here. The card is valid, the customer intends to pay, and a well-timed retry will often succeed.

Hard declines are permanent. A stolen card, a closed account, or a card flagged for fraud won't resolve on their own. Retrying blindly burns goodwill and risks triggering fraud filters.

By sorting failures at this level first, smart retry logic avoids wasting attempts on unrecoverable declines while concentrating retries where they have a real chance of converting.

How Fixed Retry Schedules Work

Fixed retry schedules follow a simple rule: attempt the payment again on predetermined days, regardless of context. A typical setup might retry on day 3, day 7, and day 14 after the initial decline. Every failed payment gets the same sequence, whether the decline was caused by insufficient funds, an expired card, or a temporary bank outage.

The schedule doesn't change based on the customer, the card type, the issuing bank, or the reason for the decline. It runs the same way every time.

How Smart Retries Adapt Timing to Failure Type

Not every declined payment fails for the same reason, and retrying them on the same schedule ignores that reality entirely.

A card flagged for insufficient funds on the 3rd of the month looks very different from one declined due to a suspected fraud flag. The first may resolve within days when the account refills after a paycheck clears. The second may never recover without cardholder action. Smart retries read the decline code and time each attempt accordingly, instead of firing on a fixed cadence that treats both failures identically.

Timing by Failure Category

Different failure types call for different retry windows.

- Insufficient funds declines respond best to retries timed around common payroll deposit windows, typically 1 to 5 days after the initial failure when balances are most likely to have refreshed.

- Suspected fraud or do-not-honor codes warrant a longer hold, since the issuer needs time to resolve the flag or the cardholder needs to intervene.

- Temporary network or processor errors can often be retried within hours, since the underlying issue is rarely tied to the customer's account at all.

Collapsing these into a single fixed retry schedule means you are either retrying too soon on fraud-flagged cards or waiting too long on simple cash-flow gaps. Both outcomes cost you recovered revenue.

Dimension | Fixed Retry Schedules | Smart Retries |

|---|---|---|

Recovery Rate | Recover 40 to 60% of recoverable failed payments | Recover 70 to 85% of recoverable failed payments |

Decision Inputs | One input: days elapsed since initial failure | Over 40 variables including card type, issuer behavior, decline code, geography, and timing |

Response to Hard Declines | Fire on calendar regardless of decline reason, wasting attempts on closed or stolen cards | Read decline code first and stop immediately when further attempts would be futile |

Card Network Compliance Risk | Structurally prone to exceeding Visa's 15-attempt and Mastercard's 10-attempt limits, triggering $1 to $25 penalties per excessive retry | Stop when further attempts would violate network rules, keeping you inside compliance guardrails |

Card Network Retry Limits and Penalty Fees

Visa and Mastercard both enforce strict retry limits on declined transactions, and exceeding them triggers fines that compound fast. Visa caps retries at 15 attempts within 30 days for a single card and transaction amount. Mastercard allows 10 retries in 24 hours. Breach either threshold and you're looking at penalties ranging from $1 to $25 per excessive retry, applied per transaction.

Fixed retry schedules are structurally prone to these violations. A static schedule fires the same attempts at the same intervals regardless of the underlying decline code, which means it will repeatedly hit hard declines or exhausted soft-decline windows just to fill out the schedule. Smart retries read the decline code first and stop when further attempts would be futile or penalized, keeping you inside network rules while protecting your merchant account standing.

Recovery Rate Benchmarks: Fixed Versus Smart Retry Systems

Industry data shows fixed retry schedules recover roughly 40 to 60% of recoverable failed payments. Smart retry systems consistently reach 70 to 85% recovery on that same pool, a gap that compounds fast at scale.

At 10,000 monthly failures with an average subscription value of $50, closing even half that gap means roughly $75,000 in additional monthly recovered revenue.

The difference comes down to signal use. Fixed schedules ignore decline codes, card type, and issuer behavior. Smart retries read all of it and act accordingly, which is why the recovery gap widens as transaction volume grows.

Variables That Smart Retries Analyze

Forget the calendar. A fixed retry schedule has exactly one input: how many days have passed since the original failure. Smart retry logic reads dozens of signals at once.

Ensemble AI models analyze over 40 variables per transaction, including:

- Card type (consumer debit versus corporate credit versus prepaid), since each carries different funding patterns and failure profiles

- Issuing bank and BIN data, which reveal issuer-specific behavior and decline tendencies

- Geographic region and local payday cadence, so retries land when funds are likely to be present

- Time of day, because hour-level timing materially affects authorization rates

- Transaction amount, customer payment history, and public holidays in the cardholder's region

A consumer debit card in the US, for instance, succeeds at 12:01am after payroll deposits. That kind of precision is what separates multivariate retry logic from a schedule that only knows what day it is, and it translates directly into more recovered revenue per attempt.

How Smart Retries Prevent Wasted Attempts on Hard Declines

Hard declines are permanent rejections. Retrying them wastes money, risks card network penalties, and can get your merchant ID flagged. Smart retries read the decline code before acting, and when a hard decline appears, they stop.

Fixed retry schedules have no such filter. They fire on a calendar regardless of why the payment failed, burning attempts on cards that are closed, stolen, or fraudulent.

The business cost is real: hard-decline retries trigger excessive fees and, in serious cases, merchant ID suspension, which cuts off your ability to process payments entirely.

The ROI Impact on Subscription Revenue

For subscription businesses, the math on payment retry logic is unforgiving. roughly 15% of recurring payments fail, and 50% of subscription churn from failed payments. Without an intelligent recovery layer, a meaningful share of that revenue simply disappears. Fixed retry schedules recover some of it, but they leave money on the table by ignoring the variables that actually predict success.

Smart retries close that gap. Where fixed schedules treat every declined payment the same, smart retries factor in decline code, card type, issuer behavior, and timing to make each retry count.

Implementation Approaches for Smart Retry Logic

Subscription billing teams typically have three paths when setting up payment retry logic: build it in-house, rely on their billing tool's native scheduler, or adopt a dedicated smart retry solution.

Building in-house gives you control, but maintaining a rules engine that accounts for decline codes, card types, and issuer behavior across geographies is an ongoing engineering burden most teams underestimate.

Native billing schedulers are fast to deploy but default to fixed retry schedules with little to no customization. They treat every failed payment the same way regardless of why it failed.

Dedicated smart retry solutions sit on top of your existing billing infrastructure and bring AI-driven decision logic without requiring engineering work. Slicker, for example, deploys in roughly five minutes with no code changes, running on your existing rails and recovering payments silently before a customer ever needs to be contacted.

The right path depends on your transaction volume and internal resources, but at scale, the gap between a fixed retry schedule and AI-powered smart retries compounds fast. Every miscategorized decline, every retry fired at the wrong time, represents MRR you already earned walking out the door.

How Slicker's AI Powers Smarter Retry Decisions

Slicker's AI analyzes dozens of signals per transaction before deciding whether to retry a payment, when to retry it, and at what amount. Instead of applying a fixed retry schedule, the system weighs card type, issuer behavior, decline code, geographic patterns, and account history simultaneously.

An ensemble of AI models handles each decision independently, then combines outputs to produce a single optimized action. Slicker customers typically see a 20 to 50% lift in recovery rates over standard retry logic, measured on their own data through clinical-grade AABB testing with statistical significance confirmed before any commitment is required.

Frequently Asked Questions

What is the difference between a soft decline and a hard decline?

A soft decline is a temporary rejection, such as insufficient funds, a momentary network timeout, or a processor error. The card is valid and a well-timed retry will often succeed. A hard decline is a permanent rejection, such as a stolen card, a closed account, or a fraud flag. Hard declines will not resolve on their own, so retrying them wastes attempts, risks card network penalties, and can damage your merchant account standing.

How many variables do smart retry systems analyze per transaction?

Smart retry systems analyze over 40 variables per transaction, including card type, issuing bank and BIN data, geographic region, local payday cadence, time of day, transaction amount, customer payment history, and public holidays in the cardholder's region. Fixed retry schedules use exactly one input: how many days have elapsed since the original failure.

What card network limits apply to payment retries, and what are the penalties for exceeding them?

Visa caps retries at 15 attempts per card within 30 days. Mastercard allows 10 retries within 24 hours on soft declines. Exceeding either threshold triggers penalties ranging from $1 to $25 per excessive retry. Fixed retry schedules are structurally prone to these violations because they fire on a calendar regardless of decline reason. Smart retries read the decline code first and stop when further attempts would violate network rules.

How quickly can a smart retry solution be deployed?

Dedicated smart retry solutions like Slicker deploy in roughly five minutes with no code changes. The system runs on your existing billing rails, recovering payments silently before a customer ever needs to be contacted. There is no engineering lift required on your team's end.

How is smart retry performance measured before full commitment?

Slicker measures recovery rate improvement through clinical-grade AABB testing, which compares retry outcomes on your own transaction data with statistical significance confirmed before any long-term commitment is required. This distinguishes verified recovery lift from vendor marketing claims, giving your finance or payments team a falsifiable performance baseline specific to your transaction volume and card mix.

Final Thoughts on Recovering Failed Payments

Fixed retry schedules fire on a calendar regardless of why the payment failed, which is why they recover 40 to 60% of what's recoverable while smart retries hit 70 to 85% on the same pool. The difference comes down to signal use: one input versus dozens. If you want to close that gap on your own transaction volume, let's run the test. At 10,000 monthly failures with a $50 average subscription, even half that lift is $75,000 in additional recovered revenue every month.

Related Articles

Code 51 Declines: Insufficient Funds Recovery Playbook (August 2026)

Not every failed payment means a lost customer, and code 51 is probably the clearest example of that. Your subscriber's card is fine; their balance was just...

Failure Reason Dunning Cadence: Route Every Decline Right (August 2026)

A payment failure is a signal, and the signal means something different depending on the decline code behind it. Treating them all the same way, one email...

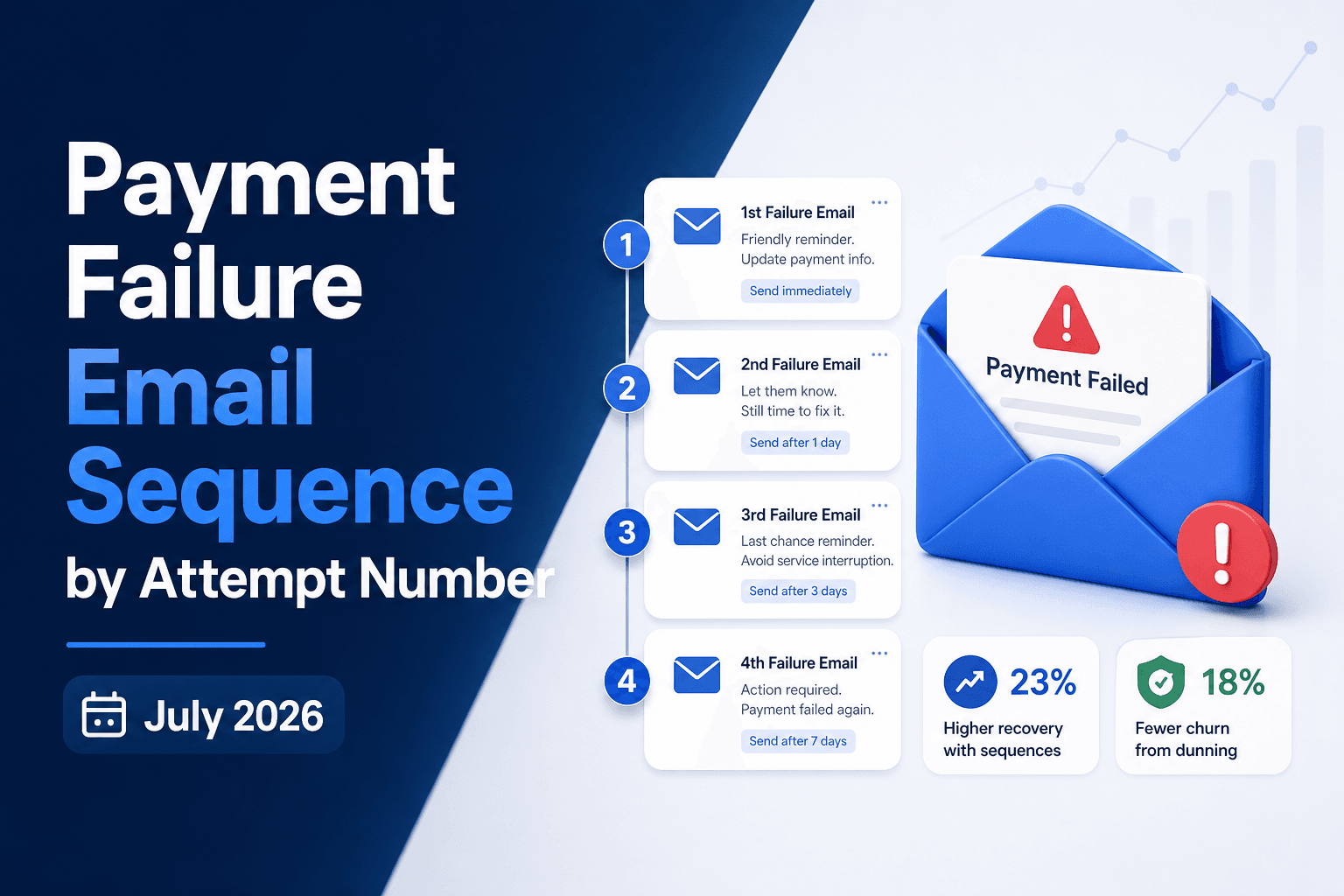

What to Send in Payment Failure Emails at Each Attempt (July 2026)

A recurring payment failure email on attempt 1 should feel like a friendly heads-up. By attempt 5, that same friendly tone reads as if you're not paying...

Stop losing revenue to failed payments

Join leading subscription businesses using Slicker to recover failed payments automatically.

Get Started