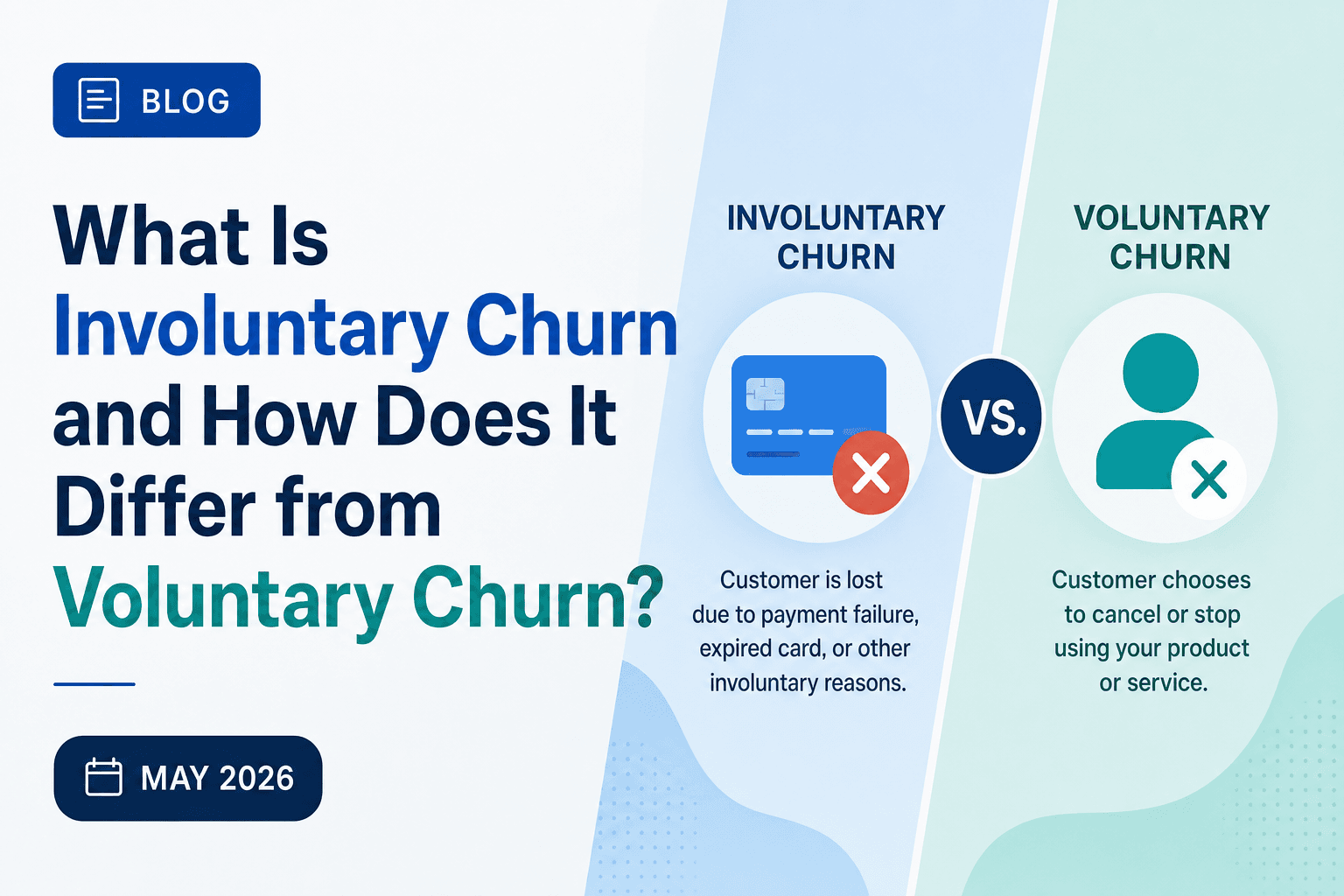

What Is Involuntary Churn and How Does It Differ from Voluntary Churn? (May 2026)

Somewhere between a quarter and 40% of your churned subscribers didn't cancel. Involuntary churn happens when a payment fails and your billing system cuts access before the customer fixes it. No opt-out. No warning. Just a declined transaction that ends the subscription because a card expired or funds ran low. These customers are recoverable with the right retry schedule and dunning approach, but only if you separate them from the subscribers who actually chose to leave.

TLDR:

- Involuntary churn accounts for 25-40% of total churn and happens when payments fail, not when customers choose to cancel.

- Failed payments will cost subscription companies $129 billion in 2025, yet most are recoverable with proper retry logic.

- Soft declines (insufficient funds, timeouts) clear with well-timed retries; hard declines (fraud, closed accounts) require customer action.

- Dunning strategies recover 30-50% of failed payments when timed to failure type, not sent on fixed schedules.

- Slicker's ML models answer whether, when, and how to retry each failed invoice, delivering 4-10 percentage point recovery rate improvements.

What Is Involuntary Churn?

Involuntary churn happens when a subscriber loses access not because they chose to leave, but because their payment failed. No cancellation. No warning. The subscription simply stops renewing due to a declined card, expired credentials, or a processor-side error.

This is sometimes called passive churn, delinquent churn, or false churn, since the customer never intended to cancel. For subscription businesses, that distinction matters: these are recoverable customers, and losing them is a billing problem, not a retention one.

Voluntary Churn vs. Involuntary Churn: Key Differences

The two types require completely different responses. Voluntary churn is a product or value problem: a customer decided to leave, driven by dissatisfaction, a competitor, or shifting priorities. No retry logic fixes that.

Involuntary churn is a billing problem. The customer still wants the subscription. The payment just didn't go through.

Voluntary Churn | Involuntary Churn | |

|---|---|---|

Cause | Customer decision | Payment failure |

Customer intent | Chose to cancel | Never intended to leave |

Share of total churn | 60-75% | 25-40% |

Right fix | Product, pricing, retention | Smarter retries, dunning |

Recoverable? | Rarely | Yes |

That 25-40% slice represents subscribers who already said yes to your product. They didn't opt out; the billing system failed them. That distinction changes everything about how you respond.

Common Causes of Involuntary Churn

Not every failed payment calls for the same fix. Insufficient funds drives over 30% of failed subscription payments on its own, but the causes span a wider range, and each points to a different recovery approach.

- Insufficient funds: Correct card, wrong balance. Often recoverable with a well-timed retry.

- Expired cards: On-file credentials have lapsed. Fixable via card updater services or a targeted email.

- Generic declines: Vague error codes requiring deeper analysis to determine if they are retryable at all.

- Fraud flags: The issuer blocked the charge as suspicious. Rarely retryable without customer action.

- Outdated billing info: Billing details or CVV mismatches that fail verification checks silently.

Which type dominates your failed invoices shapes everything about where you focus recovery efforts first.

How to Calculate Your Involuntary Churn Rate

Most billing systems lump all lost subscribers into a single churn bucket. To measure involuntary churn accurately, filter specifically for subscriptions that ended due to payment failure, not explicit cancellations.

The formula:

Involuntary Churn Rate = Subscribers lost to payment failure / Total subscribers at period start × 100

For revenue-focused teams, run the same logic on MRR: divide MRR lost to failed payments by total MRR at period start. This gives you a clearer picture of revenue exposure, since high-value subscribers failing to renew hurt more than lower-tier ones.

Where to Pull the Data

In your billing system, look for invoices tagged as past_due, unpaid, or delinquent rather than cancelled. Stripe, Chargebee, and Recurly all separate these statuses. Run the calculation monthly. That baseline number is what every recovery strategy gets measured against, and without it, you are guessing whether your retry logic or dunning emails are moving anything at all.

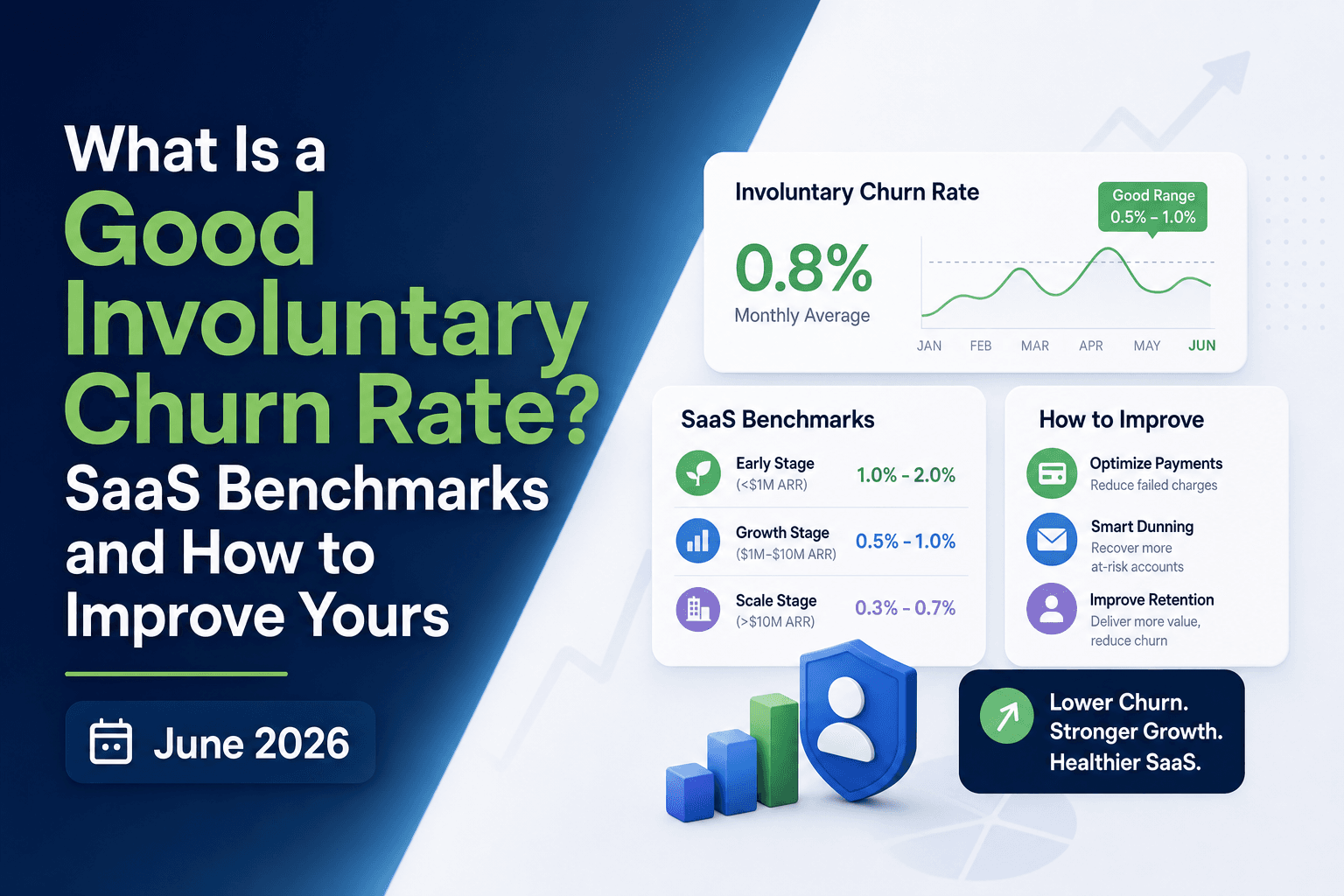

Industry Benchmarks: What's a Normal Involuntary Churn Rate?

Benchmarks shift by industry and business model. In telecom, total annual churn runs between 15-25%, with payment failures accounting for a meaningful share. Software subscription businesses typically see monthly churn split closer to 2.41% voluntary versus 0.86% involuntary.

That 0.86% monthly rate looks small in isolation. Annualized, it compounds to nearly 10% of your subscriber base lost to billing failures before a single customer actively cancels.

For most subscription businesses, if involuntary churn exceeds 1% monthly, recovery is already overdue.

The Financial Impact of Involuntary Churn on Subscription Businesses

Failed transactions are projected to cost subscription companies $129 billion in lost revenue in 2025. Average payment failure rates reach 7.9%, with certain sectors experiencing rates as high as 14.7%. That figure captures only the direct loss.

Every subscriber lost to a billing failure carries their full lifetime value out the door. A $50/month customer retained for three years represents $1,800 in revenue gone, not from a cancellation decision, but from a payment that could have been recovered.

Soft Declines vs. Hard Declines: Understanding Payment Failure Types

Not all failed payments are created equal. Soft declines are temporary: insufficient funds, processor timeouts, velocity limits. A well-timed retry often resolves them with no customer involvement at all.

Hard declines won't clear on a second attempt. Stolen cards, closed accounts, and fraud blocks require customer action. Retrying them doesn't recover revenue; it damages your merchant reputation and triggers penalty fees from Visa and Mastercard for violations of their retry policies.

"Blanket retry logic is one of the most common ways subscription businesses quietly hurt themselves. Treating every decline the same wastes retries on hard failures and burns goodwill with card networks."

Dunning Management: The First Line of Defense

Dunning is the systematic process of recovering failed payments through automated email outreach, retry scheduling, and payment update workflows. A dunning period typically runs 7 to 21 days after the initial failure, giving the recovery system time to attempt retries and prompt the customer to act before access is cut off.

When executed well, dunning requires no manual work at all. Effective strategies recover 30-50% of failures, making it among the highest-ROI retention investments available to subscription businesses.

Why Generic Dunning Sequences Fall Short

Not all dunning logic is equal. A generic "please update your payment method" email sent on a fixed schedule recovers a fraction of what a well-timed, failure-specific campaign can. The difference lies in whether the dunning logic knows what actually failed and tailors the response to the specific decline type.

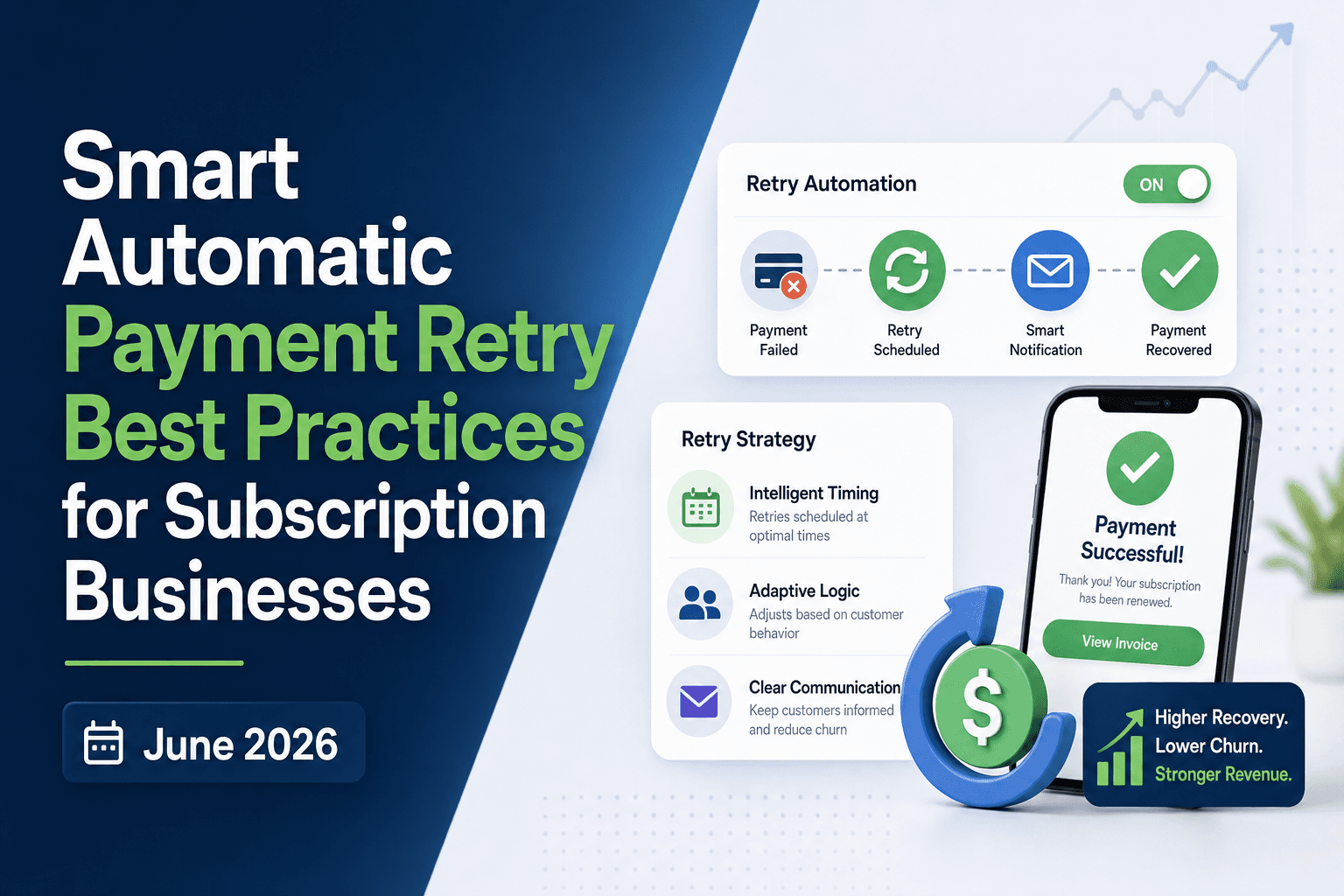

Smart Payment Retry Strategies

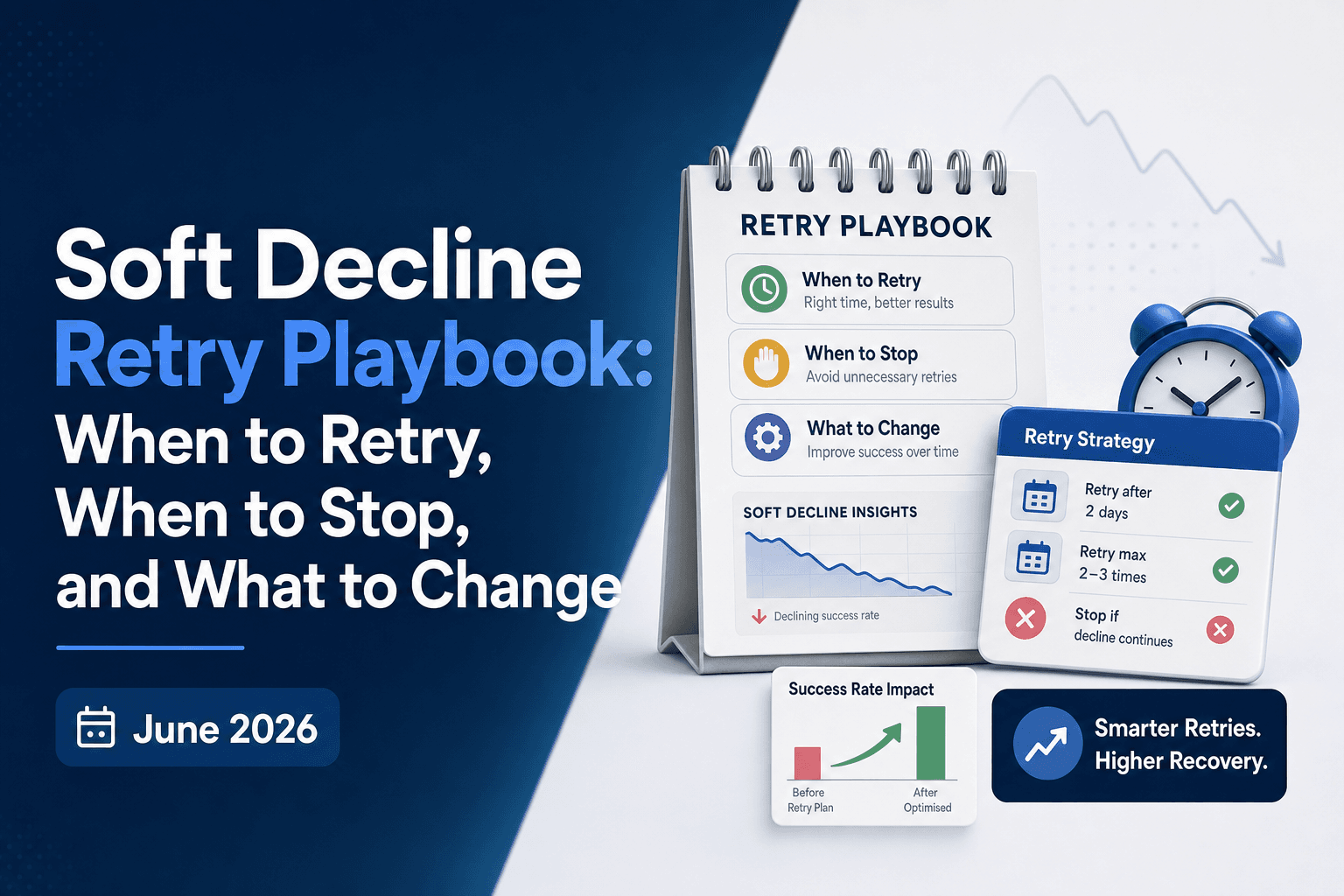

Retry timing matters more than retry volume. A consumer debit card is more likely to clear right after payday. A corporate card follows a different pattern entirely. Retrying both on the same fixed schedule is a recoverable failure.

Decline codes give you a roadmap. Insufficient funds typically calls for a retry within a few days; velocity limits suggest waiting until the next billing cycle. Merchant Advice Codes from Visa and Mastercard often specify exact retry windows. Ignoring them hurts recovery rates and triggers $0.10 per-retry penalty fees per violation.

Spacing matters too. Clustering attempts within hours on a soft decline can push an issuer toward a harder block. Three to five well-spaced attempts across a 14 to 21 day window consistently outperform aggressive rapid-fire schedules, protecting the merchant reputation your future authorizations depend on.

Proactive Prevention: Reducing Involuntary Churn Before It Happens

Card updater services like Visa and Mastercard account updater services automatically refresh expired or replaced credentials before any charge attempt, requiring no customer action whatsoever.

Pre-expiry alerts sent 15 to 30 days before a card lapses consistently outperform post-failure dunning on completion rates. When there is no access interruption adding friction, customers respond faster with less drop-off. Pre-renewal reminders sent 3 to 7 days before billing work on the same principle, giving subscribers a low-pressure window to update payment details before a decline occurs.

Every failure prevented is one less retry to schedule and one less subscriber at risk.

How Slicker Eliminates Involuntary Churn Through AI-Powered Payment Recovery

Every strategy covered in this article, smart retries, failure classification, dunning, proactive prevention, Slicker handles automatically.

The core is an ensemble of models trained across billing systems and payment processors, layered with industry heuristics for issuer-specific behavior. Together, they answer three questions per failed invoice: whether to retry, when to retry, and how to route it. Across 1 million recovered payment failures, that approach delivers a 20% recovery rate uplift, or 4 to 10 percentage points above standard retry logic.

Soft declines clear silently. Dunning emails fire only when customer action is required. And before any commitment, AABB testing borrowed from clinical trial design proves improvement with statistical certainty against your own data. If we don't outperform, you don't pay.

Final Thoughts on Stopping Subscribers From Churning Due to Payment Failures

The subscribers you lose to involuntary churn never decided to cancel. They hit a billing failure, and your payment system gave up too soon or retried at the wrong time. Between intelligent retry scheduling, dunning sequences that match the decline type, and proactive card updaters, you can recover 30 to 50% of those failed payments and stop losing revenue to a problem that was never about your product in the first place.

FAQ

Voluntary vs involuntary churn: what's the difference?

Voluntary churn occurs when a customer actively decides to cancel, driven by dissatisfaction or competitive alternatives. Involuntary churn happens when a payment fails and the subscription ends despite the customer's intent to stay. The latter accounts for 25-40% of total churn and requires billing fixes (smart retries, dunning), not product improvements.

Can I recover involuntary churn after it happens?

Yes. Soft declines (insufficient funds, processor timeouts) clear with well-timed retries in 30-50% of cases. Hard declines (stolen cards, fraud blocks) require customer action through targeted dunning. The key is matching your recovery strategy to the specific decline code and not retrying failures that will trigger penalty fees from card networks.

What's the best way to reduce involuntary churn without diverting engineering resources?

At scale, AI-powered payment recovery platforms analyze decline codes, card types, and issuer patterns to determine optimal retry timing automatically. For CFOs assessing vendor ROI, Slicker's ensemble ML models handle this across billing systems with zero engineering lift, delivering 4-10 percentage point recovery rate improvements that translate directly to recovered MRR. Card updater services (Visa Account Updater, Mastercard Automatic Billing Updater) also prevent failures before they occur by refreshing expired credentials automatically, reducing the volume your payments team needs to manage manually.

How do I know if my dunning strategy is actually working?

Calculate your involuntary churn rate monthly: subscribers lost to payment failure divided by total subscribers at period start. Track it against recovery rate (failed payments recovered divided by total failures). If involuntary churn exceeds 1% monthly or you are recovering less than 30% of soft declines, your dunning logic is leaving revenue on the table. Run AABB testing to measure improvement with statistical certainty before committing to new vendors.

What's a normal involuntary churn rate for subscription businesses?

Software subscription businesses average 0.86% monthly involuntary churn (roughly 10% annualized). B2B churn rates typically run lower due to higher-value contracts and corporate payment methods. If your rate exceeds 1% monthly, recovery is overdue. Failed transactions will cost the subscription industry $129 billion in 2025, the majority of which is recoverable with proper retry logic and dunning.

Related Articles

What Is a Good Involuntary Churn Rate? SaaS Benchmarks and How to Improve Yours (June 2026)

Most SaaS companies lose 1 to 3% of MRR every month to involuntary churn, and half of that is preventable with better retry logic. These aren't customers who...

Soft Decline Retry Playbook: When to Retry, When to Stop, and What to Change (June 2026)

You retry soft declines because you know they're recoverable, but if your retry timing is the same for every decline reason, you're burning through attempts...

Smart Automatic Payment Retry Best Practices for Subscription Businesses in June 2026

Most subscription businesses lose 15% of their recurring revenue to payment declines, and the majority of that is recoverable if you retry at the right time...

Stop losing revenue to failed payments

Join leading subscription businesses using Slicker to recover failed payments automatically.

Get Started