What Are Merchant Advice Codes and How Do They Affect Payment Recovery? (May 2026)

Your payment gateway receives visa response codes and merchant advice codes with every declined authorization. One identifies why the transaction failed. The other tells you what to do about it: retry later, cancel the subscription, or request updated card details. The data arrives in milliseconds, gets written to a log file, and rarely connects to any decision logic. Without routing MAC 03 to a hard stop and MAC 02 to a delayed retry queue, you're guessing at timing. Guessing means retrying too soon on insufficient funds, too late on expiring dunning windows, or too many times on fraud blocks that trigger network penalties. The instructions are already there. The question is whether your retry logic reads them.

TLDR:

- Merchant advice codes (MACs) tell you whether to retry, wait, or cancel after each decline

- Ignoring MACs costs $0.03-$0.50 per excess retry; Mastercard fees jumped 400% since 2022

- Code 51 with MAC 02 recovers after 2-3 days; Code 05 with MAC 03 burns retries and raises fraud risk

- Most billing systems receive MAC data but never route it to retry logic

- Slicker layers MAC guidance with card type and issuer behavior to recover 25% of "never retry" declines

What Are Merchant Advice Codes?

When a recurring payment gets declined, the issuing bank sends back more than a rejection. It includes guidance on why the payment failed and, in many cases, what should happen next. Merchant advice codes (MACs) are standardized signals embedded in authorization responses that tell merchants the optimal action to take after a decline.

Mastercard introduced MACs primarily to reduce unnecessary retry traffic on their network. Without guidance, merchants retry blindly on card-not-present recurring transactions. MACs cut through that noise by indicating whether to retry immediately, wait a specific number of days, or stop retrying altogether.

How Merchant Advice Codes Work in Transaction Processing

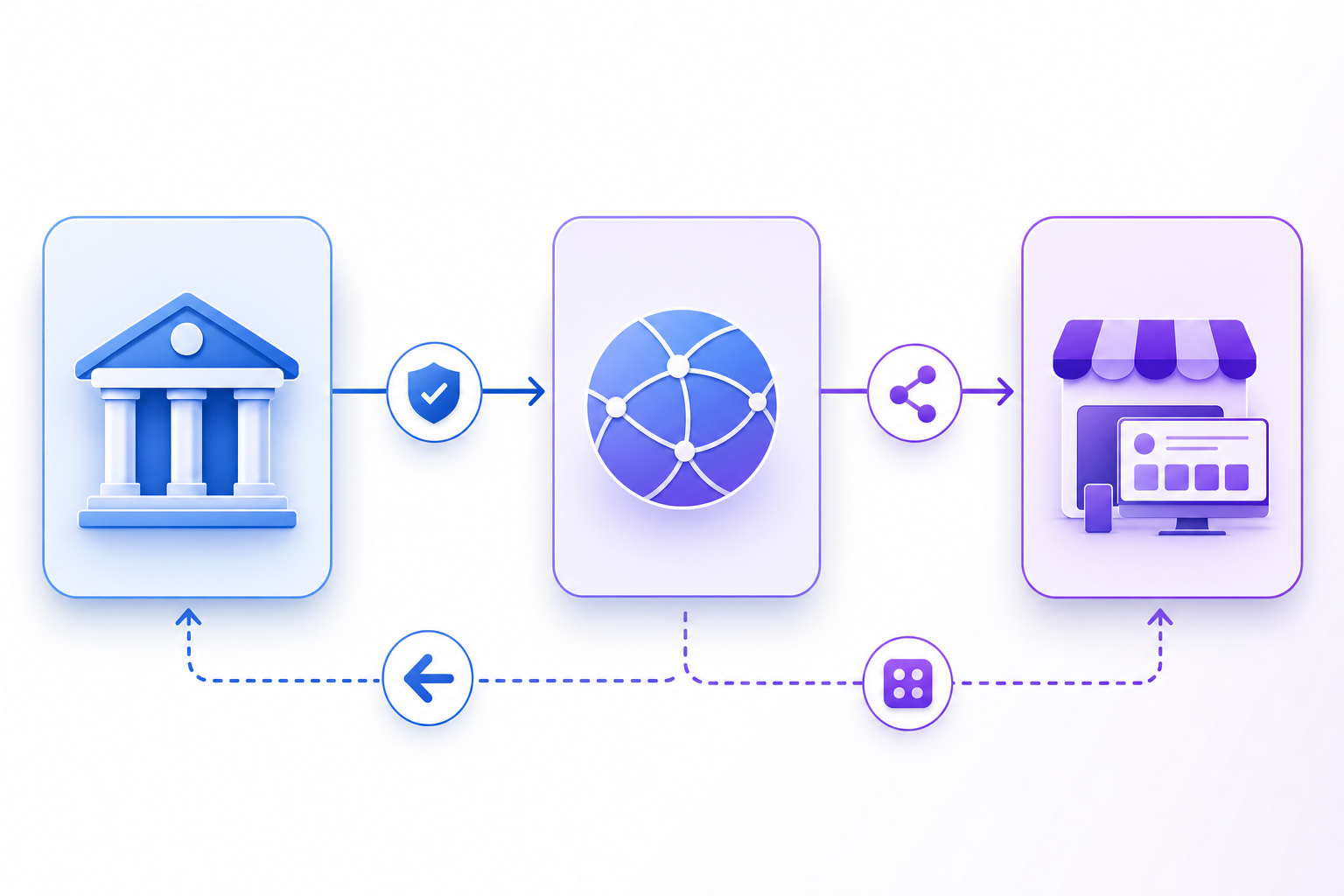

When a card transaction is declined, the issuing bank returns an authorization response code to the payment network, which then forwards a merchant advice code (MAC) to the merchant. These codes travel through the processing chain in milliseconds, carrying instructions the issuer wants you to act on. MACs sit on top of standard decline codes and tell you more than just that a transaction failed: they tell you what to do next: retry, cancel the subscription, or contact the cardholder.

The Complete List of Mastercard Merchant Advice Codes

Mastercard publishes a standardized set of merchant advice codes that processors return alongside decline responses. Each code tells you precisely why a transaction failed and, more importantly, what action to take next.

Code | Description | Recommended Action |

|---|---|---|

01 | New account information available | Update card details via account updater |

02 | Cannot approve at this time, try later | Retry after a waiting period |

03 | Do not try again | Cancel the subscription |

04 | Token requirements not fulfilled for this token type | Update token or request a new payment method |

05 | Negotiated value not approved | Contact issuer or adjust transaction terms |

21 | Payment cancellation | Stop all retry attempts immediately |

22 | Merchant does not qualify for product code | Contact issuer; do not retry with same product code |

24 | Retry after 1 hour (Mastercard use only) | Queue retry for 1 hour from decline time |

25 | Retry after 24 hours (Mastercard use only) | Queue retry for 24 hours from decline time |

26 | Retry after 2 days (Mastercard use only) | Queue retry for 2 days from decline time |

27 | Retry after 4 days (Mastercard use only) | Queue retry for 4 days from decline time |

28 | Retry after 6 days (Mastercard use only) | Queue retry for 6 days from decline time |

29 | Retry after 8 days (Mastercard use only) | Queue retry for 8 days from decline time |

30 | Retry after 10 days (Mastercard use only) | Queue retry for 10 days from decline time |

40 | Consumer non-reloadable prepaid card | Request an alternate payment method from the cardholder |

41 | Consumer single-use virtual card number | Request updated card details; virtual card cannot be reused |

Visa Response Codes and Category Classifications

Visa groups its response codes into four broad categories: approval, referral, decline, and error. Within declines, the split between soft and hard codes determines whether a retry is worth attempting.

The most common Visa response codes include 00 (approved), 05 (do not honor, soft decline), 51 (insufficient funds, soft decline), 57 (transaction not permitted, hard decline), 59 (suspected fraud, hard decline), and 83 (fraud/security violation, hard decline). Codes 57 and 59 should trigger immediate customer outreach instead of automated retries, since the issuer is signaling a policy or fraud block instead of a temporary funding gap.

Understanding Authorization Response Codes vs. Merchant Advice Codes

Response codes identify the failure reason. MACs prescribe the recovery action. That distinction is what separates a structured retry strategy from guesswork.

A code 51 decline (insufficient funds) can arrive with MAC 24 (retry in 24 hours), MAC 27 (retry in 72 hours), or MAC 30 (retry in 10 days), depending on what the issuer signals. Same failure reason, three very different retry windows.

Without the MAC, you're guessing at timing, which means retrying too soon, frustrating the issuer, and accumulating retry fees.

The Financial Cost of Ignoring Merchant Advice Codes

Mastercard charges a fee for every retry after receiving MAC 03 or MAC 21 within 30 days. That fee has climbed from $0.10 per excess authorization in 2022 to $0.50 by January 2025, with regional variation ranging from $0.03 to $0.50 per transaction. At volume, those cents compound fast.

Visa runs a similar program. Exceed 15 retry attempts in 30 days for certain decline categories, and you're looking at $0.10 per domestic transaction and $0.15 per international one in excess reattempt fees.

Network | Trigger Condition | Fee Per Transaction | 30-Day Lookback Window |

|---|---|---|---|

Mastercard | Any retry after receiving MAC 03 or MAC 21 | $0.03 to $0.50 (regional variation; $0.50 as of Jan 2025) | Yes, penalties apply to excess retries within 30 days of initial MAC |

Visa | More than 15 retry attempts on certain decline categories | $0.10 domestic, $0.15 international | Yes, 15-attempt threshold measured over rolling 30-day period |

The networks designed these penalties to protect authorization quality across their infrastructure. When merchants flood the network with retries on fraud-flagged or cancelled cards, everyone's authorization rates suffer. The fees are a signal: respect the guidance, or pay for the noise you're creating.

How Merchant Advice Codes Reduce Involuntary Churn

For subscription businesses, involuntary churn from failed payments is one of the most preventable sources of revenue loss. Merchant advice codes give you a direct signal from the card networks about why a transaction failed and, more importantly, what to do next.

Instead of treating every decline the same way, you can act on the specific guidance embedded in each code. Retry when timing is the issue. Cancel when the card is flagged as fraudulent. Update payment details when the account has changed.

That targeted response is what separates passive revenue recovery from an active one.

Common Decline Codes and Their Merchant Advice Code Pairings

Not every decline is the same, and treating them as if they were is one of the most expensive mistakes in subscription billing.

The Most Common Code Pairings

Decline Code | Meaning | Typical MAC | Recommended Action |

|---|---|---|---|

Code 05 | Do not honor | MAC 03 | Do not retry |

Code 51 | Insufficient funds | MAC 02 | Retry after 2-3 days |

Code 54 | Expired card | MAC 24 | Request card update |

Code 57 | Transaction not permitted | MAC 03 | Do not retry |

Code 59 | Suspected fraud | MAC 03 | Do not retry |

- Code 05 with MAC 03 signals the issuer has flagged the account, and retrying burns retry attempts while increasing fraud exposure.

- Code 51 with MAC 02 is recoverable with optimal retry cadence, often resolving within days once a paycheck clears.

- Code 54 pairings almost always require an account updater or dunning outreach instead of a raw retry.

Implementing MAC-Based Retry Logic in Payment Systems

Most billing systems receive MAC data in authorization responses without routing it to any retry logic. The implementation gap is that common: the guidance arrives, gets logged, and goes ignored.

The fix is a conditional layer mapped directly to each code. MAC 03 and MAC 21 trigger a hard stop with no further attempts. MAC 02 queues a adaptive retry schedule after 48 hours. MAC 01 fires an account updater request before any retry runs. Each code needs a defined outcome, or the network's guidance is useless.

"The data is already there. The problem is the action layer that should follow it."

Gateway integrations vary. Some processors surface MACs natively in response fields; others bury them in extended data objects that require parsing. Whichever the case, your retry engine should parse and act on this data automatically, not route it to a manual review queue.

The Difference Between Merchant Advice Codes and Merchant Category Codes

MACs (Merchant Advice Codes) and MCCs (Merchant Category Codes) both appear in payment processing conversations, but they operate in entirely separate layers of the payment stack.

MCCs are four-digit codes that classify what type of business you run. Code 5411 identifies grocery stores; 7399 covers business services. Issuers use these classifications to set interchange rates, determine rewards eligibility, and flag restricted transaction categories. They describe your company to the network before a transaction even attempts authorization.

MACs are post-decline guidance codes that prescribe recovery actions after a transaction fails. One identifies your business. The other tells you what to do when a payment gets rejected. Same abbreviation structure, entirely different function, and searching for the wrong one will cost you time.

Smart Retry Strategies That Go Beyond Basic MAC Compliance

Following MACs is the floor, not the ceiling. MAC 02 creates retry loops when subsequent attempts return the same code, and ten-day retry windows can outlast your dunning period entirely, recovering nothing after the subscription is already cancelled.

Even MAC 03 carries nuance. Policy blocks get lifted. Fraud flags get resolved. A rigid no-retry rule misses those recoveries.

Intelligent systems layer MAC guidance with additional signals before making a recovery decision:

Recovery Approach | Basic MAC Compliance | Slicker's Intelligent MAC Approach |

|---|---|---|

MAC 02 (retry later) handling | Wait exactly as prescribed, even if 10-day window exceeds dunning period; miss recovery opportunity when subscription cancels at day 5 | Find optimal retry window within dunning constraints; balance MAC guidance against subscription lifecycle to maximize recovery before cancellation |

MAC 03 (never retry) handling | Hard stop with zero retry attempts; leave 25% of recoverable revenue on the table | Layer issuer behavior data and card type signals; identify the 25% of MAC 03 cases that recover under specific conditions while avoiding penalty fees |

Infinite loop protection | No safeguards; retry hourly when MAC prescribes it, accumulate fees on circular guidance | Track MAC response patterns; break retry loops when same MAC returns repeatedly; escalate to dunning outreach instead of burning attempts |

Retry timing precision | Follow network windows blindly; ignore subscriber-specific patterns like payday cycles or issuer-specific approval windows | Combine MAC windows with payday timing, issuer approval patterns, card product type, and historical recovery data by bank to pinpoint highest-probability attempt timing |

Network penalty risk | Manual monitoring required; risk $0.03-$0.50 per transaction fees when logic errors cause MAC 03 or MAC 21 violations | Built-in guardrails prevent penalty-triggering retries; stay under Mastercard and Visa thresholds while maximizing safe recovery attempts |

- Historical recovery rates by issuing bank and card product

- Payday timing relative to the attempt date

- Card type (consumer debit vs. corporate credit)

- Geography and payday timing relative to the attempt date

- Transaction amount relative to typical account activity

- Prior retry outcomes for that specific customer

How Slicker Uses Merchant Advice Codes to Maximize Payment Recovery

Slicker treats merchant advice codes as strong signals, not hard rules. The system respects Mastercard and Visa penalty thresholds to stay clear of excess retry fees, but the recovery logic builds on that foundation instead of stopping at it.

When a MAC prescribes a 10-day retry window but your dunning period expires in five, Slicker's AI pinpoints the optimal attempt within that constraint. When MACs signal "never retry," our data shows roughly 25% of those transactions still recover under the right conditions, something a rigid compliance-only approach will always leave on the table.

Ensemble ML models weigh MAC guidance alongside card type, issuer behavior, and subscriber history to find the highest-probability recovery window for each individual transaction.

Final Thoughts on Maximizing Recovery With Merchant Advice Codes

The card networks send merchant advice codes with every decline to cut down on blind retries and protect authorization quality across their infrastructure. Following that guidance keeps you out of penalty territory, but pairing it with issuer behavior data and transaction history is what turns compliance into real recovery gains. Your billing system already receives the codes, the question is whether your retry logic acts on them.

Talk to us about turning MAC data into measurable revenue recovery.

FAQ

What's the difference between merchant advice codes and standard decline codes?

Decline codes tell you why a payment failed, while merchant advice codes tell you what to do next. A code 51 decline (insufficient funds) can arrive with different MACs prescribing retry windows of 24 hours, 72 hours, or 10 days, depending on the issuer's guidance.

Can I retry a transaction after receiving MAC 03 or MAC 21 from Mastercard?

No, retrying after MAC 03 or MAC 21 triggers excess authorization fees that now reach $0.50 per transaction as of January 2025. These codes signal hard stops like fraud flags or card cancellations where retries damage your authorization rates and cost you money.

Mastercard merchant advice codes vs Visa response codes: which should I focus on?

Both matter, but they operate differently. Mastercard MACs provide explicit retry guidance (MAC 02, MAC 03), while Visa uses category-based response codes (05, 51, 57) that require interpretation. Your retry engine should layer both signals to avoid network penalties and maximize recovery.

How much do excess retry fees actually cost at scale?

Visa charges $0.10 domestic ($0.15 international) per retry beyond 15 attempts in 30 days on certain decline categories. Mastercard's fees range from $0.03 to $0.50 per transaction when ignoring MAC 03 or MAC 21 guidance. At 10,000 monthly declines with a 20% violation rate, you're looking at $2,000-$10,000 monthly in avoidable fees.

Should I always follow MAC 02 retry timing recommendations?

Not blindly. MAC 02 creates recovery gaps when the prescribed 10-day window outlasts your dunning period. Roughly 25% of "never retry" transactions still recover under specific conditions involving card type, issuer behavior, and payday timing. The optimal approach layers MAC guidance with ML models trained on your actual recovery patterns by issuing bank, geography, and subscriber history.

Related Articles

Merchant Advice Codes: Retry Guide (June 2026)

A payment declines, and your billing system sees both a response code and a Mastercard advice code in the authorization message. The response code tells you...

What Is a Good Involuntary Churn Rate? SaaS Benchmarks and How to Improve Yours (June 2026)

Most SaaS companies lose 1 to 3% of MRR every month to involuntary churn, and half of that is preventable with better retry logic. These aren't customers who...

Soft Decline Retry Playbook: When to Retry, When to Stop, and What to Change (June 2026)

You retry soft declines because you know they're recoverable, but if your retry timing is the same for every decline reason, you're burning through attempts...

Stop losing revenue to failed payments

Join leading subscription businesses using Slicker to recover failed payments automatically.

Get Started