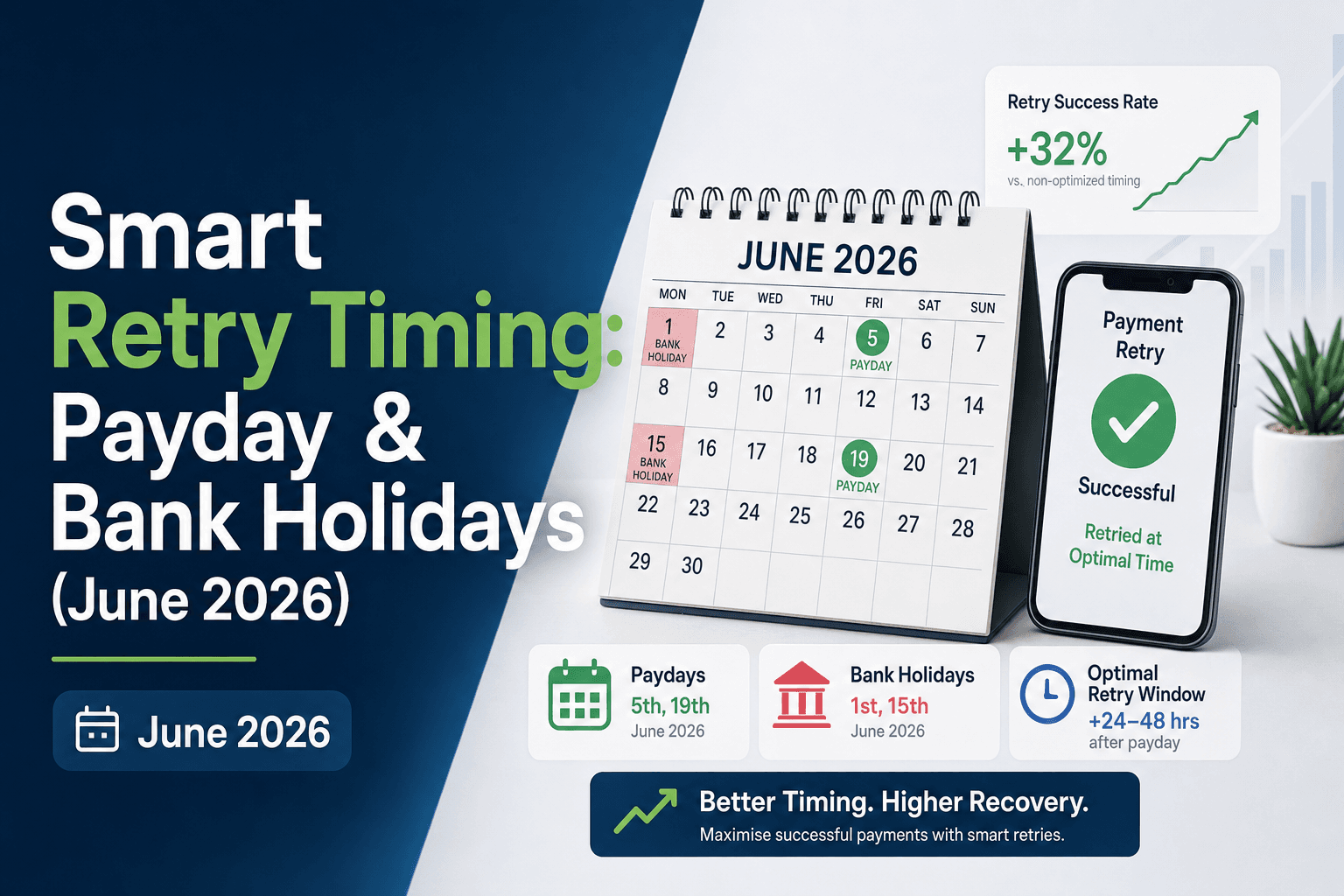

Smart Retry Timing: Payday & Bank Holidays (June 2026)

You set your retry schedule years ago. Three attempts, maybe four, spaced out by some number of days that felt reasonable at the time. The system fires retries on that fixed calendar, and no one has questioned whether the timing itself is leaving money on the table. It is. A retry landing at 12:01am when credit limits refresh clears at a measurably higher rate than one fired during business hours, and a retry scheduled for a bank holiday burns an attempt against a skeleton-staff authorization system that was never going to approve it. Payday timing varies by region, and your payment retry schedule should read that calendar. US workers get paid biweekly on Fridays. UK salaries clear at month-end. Russian state employers pay on the 5th and 20th. Retrying mid-cycle, when balances are naturally lower, recovers fewer dollars than waiting for the next pay window. The optimal retry time isn't arbitrary, and treating it like a constant costs you recoverable revenue every month.

TLDR:

- Retries at 12:01am see higher success rates for insufficient-funds declines because card limits reset at midnight.

- Payday windows vary by region: US biweekly pay peaks Thursday-Saturday, UK monthly pay concentrates end-of-month.

- Bank holidays create dead zones where retries face higher decline rates and can trigger issuer flags.

- Industry data shows 3-4 retry attempts spaced around pay cycles recover most payments; attempts beyond four show diminishing returns.

- Slicker's AI schedules retries by reading payday proximity, issuer reset patterns, bank holidays, and card-level history.

Why Retry Timing Determines Payment Recovery Success

Retry timing is one of the most consistently overlooked variables in payment recovery. Most billing teams set a retry schedule once. The problem is that a retry fired at the wrong moment has a measurably lower chance of clearing, and at scale, those misses compound into real revenue loss.

The timing of a retry attempt interacts with several factors that change throughout the month: when a customer's account is funded, whether their bank is processing normally, and what day of the week it is. A retry landing at 12:01am on a bank holiday against an unfunded account is not the same as one landing the afternoon after a customer's paycheck clears. The authorization outcome will differ, and the gap in recovery rates between good and poor timing can be substantial.

Getting the schedule right means accounting for payday cycles by region, avoiding bank holidays, and understanding intraday processing windows. Each of those variables deserves separate attention.

The 12:01am Phenomenon: When Card Balances Reset and Funds Clear

Many subscription billing systems process end-of-day settlement batches at midnight, which means card balances and credit limits often refresh at 12:01am. A customer who was over their limit at 11:59pm may have available funds just two minutes later. Retry timing that accounts for this window consistently outperforms schedules built around business hours alone.

Industry data suggests that retries in the 12:01am to 12:15am window see meaningfully higher success rates for soft declines tied to insufficient funds. The logic is straightforward: funds clear, limits reset, and your retry lands before the cardholder's next transaction competes for that headroom. Card transaction authorizations typically settle after midnight, creating this predictable refresh window.

Why This Window Gets Overlooked

Most payment retry schedules are built around what's convenient for billing teams instead of issuer behavior. Retrying at 9am or during business hours feels intuitive, but it ignores how card networks and issuing banks actually batch their settlement cycles.

- Midnight resets are not universal, but they are common enough across major US and European issuers that treating 12:01am as a priority retry window produces measurable lift on insufficient-funds declines.

- The window is narrow, typically 10 to 15 minutes, before competing transactions from subscriptions, autopay bills, and scheduled transfers begin drawing down the refreshed balance.

Getting this timing right on a per-issuer basis is where a fixed retry schedule leaves recoverable revenue on the table.

Payday Patterns: Aligning Retries with When Customers Have Funds

Payday timing varies more than most retry schedules account for. In the US, most salaried workers are paid biweekly, meaning funds typically clear on Fridays. In the UK, monthly pay cycles concentrate purchasing power at the end of the month. In Australia, weekly and fortnightly pay are both common, spreading recovery windows more evenly across the calendar. Pay frequency differences across countries create distinct optimal retry windows that fixed schedules miss.

Getting this right by region makes a measurable difference. Consider these concrete retry windows:

Region | Dominant Pay Cycle | Optimal Retry Window | Rationale |

|---|---|---|---|

United States | Biweekly (Fridays) | Thursday evening through Saturday morning | Biweekly deposits have cleared and account balances are at their peak |

Western Europe (UK, Germany, France) | Monthly (end-of-month) | Final 2-3 business days of the month | Captures the bulk of monthly salary deposits |

Russia | Semi-monthly (5th and 20th) | 5th and 20th of each month | State and corporate salaries cluster around these dates |

Australia | Weekly and fortnightly (mixed) | Monday and Thursday | Spreads coverage across mixed weekly and fortnightly pay cycles |

Chasing a failed payment mid-cycle, when balances are naturally lower, recovers fewer dollars than waiting for the next pay window. The calendar is a variable your retry logic should read.

Bank Holidays and Payment Processing: Why Some Days Are Dead Zones

Bank holidays create genuine dead zones in payment processing. When a bank is closed, its authorization systems are either offline or running on skeleton staff, meaning retry attempts that land on those days face dramatically higher decline rates with no compensating upside.

The scope is wider than most teams expect. A subscription business serving customers across the US, UK, EU, and Australia will encounter overlapping holiday calendars that collectively block out dozens of processing days per year.

Why Retrying on Bank Holidays Costs You Twice

The first cost is the failed retry itself. The second is subtler: repeated failures on the same card can trigger issuer-level flags that make subsequent retries harder even after the holiday ends. You burn attempts and damage your standing with the issuer simultaneously.

The practical fix is straightforward. Map your customer base to their local bank holiday calendars, and shift retries to the next business day. Recovery rates on those rescheduled attempts will reflect normal processing conditions instead of a degraded holiday window.

Decline Code Intelligence: Different Failure Reasons Require Different Timing

Not every failed payment fails for the same reason, and the reason behind a decline should shape when you retry.

Soft declines like "insufficient funds" follow predictable cash flow cycles. Retrying 24 to 48 hours after payday windows tend to outperform midnight retries for these codes. Hard declines from lost or stolen cards, however, should not be retried on any schedule since the card itself is invalid and no timing adjustment will change that outcome.

Key decline categories and retry timing

There are a few broad categories worth separating out when building a payment retry schedule:

- Insufficient funds declines respond well to payday-aligned timing, since the account balance recovers after a deposit clears, not at an arbitrary hour.

- Do not disturb or card velocity declines often resolve within a short cooling-off window, making same-day or next-day retries worth testing.

- Expired card and stolen card declines require customer action before any retry attempt, so automated retries waste attempts and can trigger issuer flags.

Treating all decline codes with one schedule leaves recoverable revenue on the table by retrying unrecoverable failures and missing the right window on soft declines.

Time-of-Day Effects: Business Hours Versus Evening Peaks

Retry success rates shift across the day, and ignoring that pattern leaves recoverable revenue on the table.

Payment retries attempted during business hours (9am to 5pm, local time) tend to see higher approval rates than late-night attempts. The likely reason: cardholders are active, banks have full staffing on fraud review queues, and automated risk models see daytime activity as lower-risk.

That said, there is a secondary peak worth scheduling around.

The 8pm to 10pm Window

Evening hours see a lift in approvals for consumer subscription products. Cardholders checking accounts after work often resolve insufficient-funds situations by transferring balances or moving money between accounts. A retry queued for 8pm to 10pm local time can catch that liquidity before midnight resets it.

Structuring your payment retry schedule around these two windows instead of batching retries at arbitrary intervals connects timing directly to approval probability and recovered revenue.

The Economics of Retry Frequency: How Many Attempts and How Far Apart

Industry data shows that most failed payments aren't recovered on the first retry. The question is how many attempts to schedule and how to space them.

Industry research suggests three to four retries recover the majority of recoverable payments. Attempts beyond four show sharply diminishing returns, and excessive retries risk triggering fraud flags from issuers.

Spacing Matters as Much as Volume

Retrying too quickly after a decline often hits the same decline reason. A common pattern that performs well:

- Retry 1 at 24 to 48 hours, giving short-term cash flow issues time to resolve

- Retry 2 at 5 to 7 days, targeting the first payday window after the initial failure

- Retry 3 at 14 days, capturing the next pay cycle for biweekly earners

- Retry 4 at 21 to 28 days, as a final sweep before the account moves to dunning

Spacing retries around pay cycles instead of arbitrary calendar intervals is where most generic billing tools fall short. A subscriber paid on the 15th and 30th has a very different optimal retry window than one paid weekly.

Getting retry frequency right protects revenue without overloading your issuer relationships or burning customer goodwill through repeated failed charge notifications.

How Slicker Optimizes Retry Timing with AI-Powered Precision

Slicker's AI doesn't rely on fixed retry schedules. Instead, it reads signals across issuer behavior, cardholder history, and calendar context to decide when a retry has the highest probability of clearing.

The retry timing engine accounts for the patterns covered in this post: payday windows by region, issuer processing resets at midnight, and bank holiday blackouts. A subscriber paid on the 15th in Germany gets a different retry window than a weekly-paid worker in the US.

What the AI Weighs

Before scheduling a retry, Slicker's ensemble of AI models weighs several timing factors:

- Estimated payday proximity based on country, employer type, and card BIN data

- Known issuer reset patterns, including the 12:01am authorization window

- Upcoming bank holidays in the subscriber's region that could delay settlement

- Prior retry history for that specific card and issuer combination

This isn't guesswork. Every retry decision feeds back into the model, tightening predictions over time on your actual subscriber base.

The result: retries land when funds are statistically more likely to be present, timed by probability instead of arbitrary intervals.

Final Thoughts on Smart Payment Retry Scheduling

Timing a retry well is the difference between recovering revenue you already earned and watching it walk away permanently. The patterns are there: payday windows by country, midnight credit resets, bank holiday blackouts. What's missing in most billing systems is logic that actually reads those signals and adjusts per subscriber. That's the gap Slicker closes, turning retry timing from guesswork into a data-driven decision that lands when your customer can actually pay.

FAQ

Can I optimize retry timing without replacing my billing system's built-in retries?

Yes. Slicker works alongside your existing billing system and can run in parallel with native retry logic from Stripe, Chargebee, or Zuora. The system uses AABB testing to prove incremental lift over your current setup: measuring only the additional revenue recovered by Slicker's timing intelligence beyond what your existing setup already captures.

What's the best retry schedule for insufficient funds declines versus expired card failures?

Insufficient funds declines respond to payday-aligned timing because account balances recover after deposits clear, typically 24 to 48 hours after regional pay windows. Expired card failures require customer action before any retry succeeds, so automated retries waste attempts regardless of timing. The optimal schedule depends on the specific decline code: it determines whether timing adjustments or customer outreach will produce recovery.

Retry timing: fixed schedule vs AI-powered?

Fixed schedules apply the same retry intervals to every failed payment regardless of region, card type, or failure reason. AI-powered timing reads issuer behavior, payday cycles, and bank holiday calendars to schedule each retry when that specific card is statistically most likely to clear. Well-timed retries measurably outperform poorly timed ones at scale, translating to material revenue differences for subscription businesses processing thousands of failures monthly.

When should I schedule retries around the 12:01am window?

The 12:01am retry window works for soft declines tied to insufficient funds or credit limit exhaustion, particularly on consumer debit cards where midnight settlement batches refresh available balances. The window is narrow (typically 10 to 15 minutes) before competing transactions draw down the refreshed balance. This timing performs poorly on hard declines like stolen cards or fraud blocks, where no timing adjustment will change the outcome and customer action is required instead.

Related Articles

How to Build a Retry Allowlist and Blocklist From Declines (July 2026)

I'll be frank: most retry logic is built on assumptions, not data. A retry allowlist tells your system when to try again; a payment retry blocklist tells it...

Country Retry Rules: India RBI, UK Direct Debit & Germany PayPal July 2026

Failed payment recovery looks very different depending on where your customer is. India's RBI retry rules limit attempts and require pre-debit notifications...

Static vs Adaptive Retry: ML Differences (June 2026)

When a payment fails, static retry logic fires on a fixed schedule: day 3, day 7, day 14. Every customer gets the same sequence regardless of why the payment...

Stop losing revenue to failed payments

Join leading subscription businesses using Slicker to recover failed payments automatically.

Get Started