Country Retry Rules: India RBI, UK Direct Debit & Germany PayPal July 2026

Failed payment recovery looks very different depending on where your customer is. India's RBI retry rules limit attempts and require pre-debit notifications before each one. UK direct debit retry rules under Bacs allow one re-presentation, full stop. Germany's PayPal cancellations bypass your retry logic entirely and route straight to a customer action. If your retry schedule doesn't account for these, you're leaving money on the table and exposing your business to compliance risk.

TLDR:

- India's RBI 2026 framework requires a ~24-hour pre-debit notification window before each retry attempt; for transactions above ₹15,000 INR, the customer must explicitly approve the charge before it can proceed.

- UK Direct Debit gives you one re-presentation within 30 days; wasting it on hard failures forfeits your only recovery attempt.

- In Germany, PayPal billing agreement cancellations are hard terminations, not soft declines, and no retry schedule can reverse them.

- Aligning retry timing to local payday windows (UK: month-end, India: 1st and 7th) recovers more than fixed calendar schedules.

- Slicker's AI models build regulatory constraints and regional pay cycles into each retry schedule by country, by default.

Why Retry Rules Differ by Country

Payment networks, banking regulators, and local consumer-protection laws each set their own rules for how and when a failed payment can be retried. A retry attempt that complies with Visa and Mastercard retry rules may still violate RBI mandate limits in India, breach UK Direct Debit Scheme rules, or trigger a PayPal account suspension in Germany.

Three forces shape these differences:

- Regulatory frameworks vary by jurisdiction: India's RBI caps retry frequency directly, while the UK's Payment Systems Regulator works through scheme rulebooks that govern Direct Debit presentments.

- Consumer protection standards differ: Germany's strong debtor-rights culture means aggressive retry behavior can escalate into formal complaints or chargebacks faster than in other markets.

- Payment rail architecture matters: Direct Debit, UPI, SEPA, and card networks each expose different retry levers, so the same logic cannot be copied across rails without risking non-compliance or account-level penalties.

Getting this wrong costs more than a failed transaction. Scheme fines, issuer-imposed merchant ID (MID) restrictions, and rising chargeback ratios compound quickly at subscription volume.

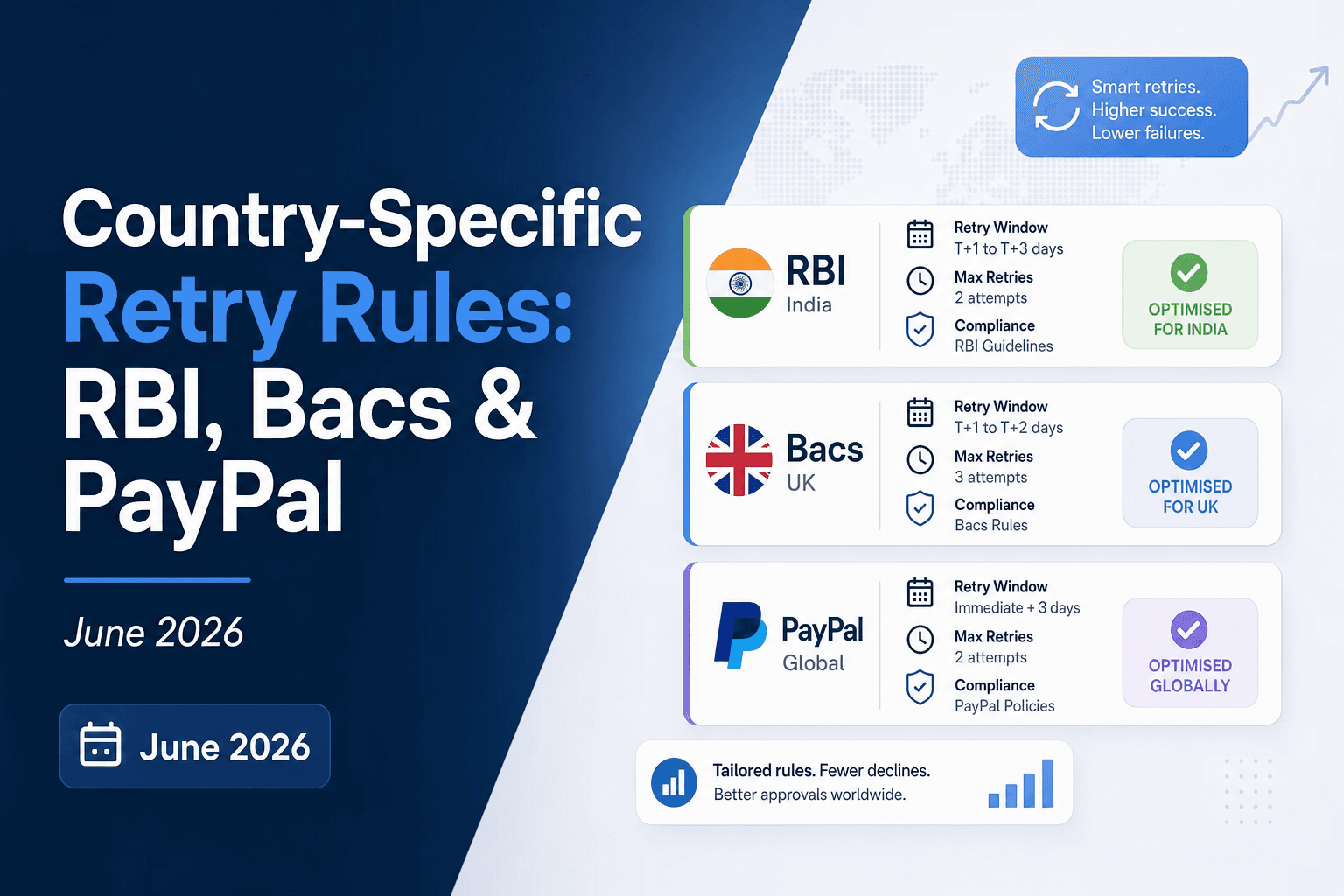

India RBI E-Mandate Framework: The 2026 Unified Rules

On April 21, 2026, the Reserve Bank of India issued the Digital Payments E-mandate Framework 2026, replacing eight prior circulars with one unified ruleset. As Mondaq's regulatory analysis notes, this consolidates seven years of fragmented recurring-payment guidance into a single architecture. Previously, recurring payment obligations were split across separate directives for cards, UPI, and prepaid payment instruments (PPIs), each carrying different requirements.

The consolidated framework changes how retry windows work in practice.

What changed for retry timing

Under the unified rules, failed e-mandate executions follow a single retry governance structure regardless of payment rail:

- Merchants must wait a minimum of 24 hours before the first retry attempt after a failed mandate execution, closing the door on same-day re-presentation.

- There is no hard cap on the number of retries per billing cycle, but each attempt must be preceded by a fresh 24-hour pre-debit notification window. For transactions above ₹15,000 INR, the customer must explicitly approve the charge before it can proceed. Getting the optimal retry cadence for soft declines right matters because every attempt requires that notification buffer to be respected before execution.

- Each retry requires a fresh pre-debit notification to the customer, sent at least 24 hours before execution, keeping the cardholder informed at every stage.

Ignoring these rules carries real cost. Non-compliant retries are rejected at the rail level, which means failed recovery attempts that also generate regulatory exposure. For high-volume subscription businesses billing into India, the retry budget is tight and every attempt must count.

Pre-Debit Notifications and AFA Thresholds Under RBI Rules

India's Reserve Bank of India (RBI) sets some of the strictest pre-debit rules of any major market. Merchants must send a pre-debit notification to the cardholder at least 24 hours before any recurring charge is attempted. This applies to all mandates registered under the e-mandate framework, regardless of amount.

Additional Factor Authentication (AFA) Thresholds

Transactions above ₹15,000 require Additional Factor Authentication (AFA) at the point of mandate registration. Below that threshold, subsequent debits can proceed without re-authentication, provided the pre-notification window is respected.

Rule | Requirement |

|---|---|

Pre-debit notice window | Minimum 24 hours before charge |

AFA threshold | ₹15,000 per transaction |

Mandate registration | AFA required at setup for all amounts |

Retry attempts that skip the notification window are rejected outright, not soft-declined, so failed retries here carry a different recovery profile than in Western markets. A clear soft decline retry playbook helps separate these cases before scheduling. Your retry schedule must account for the 24-hour buffer before each attempt, or the transaction will never reach the issuer.

UK Direct Debit Retry Rules: How Bacs Re-Presentation Works

Bacs governs UK Direct Debit through a two-presentation rule: if the first collection attempt fails, you get one re-presentation. That's it. No third attempt is permitted under the scheme rules. Under UK Direct Debit re-presentation rules, the amount being collected must also match the original presentation exactly.

The re-presentation must occur within 30 days of the original due date, and you must notify the payer at least two working days before the second attempt. Most failures in this scheme are soft declines tied to temporary insufficient funds, so timing the re-presentation around a customer's payday window matters.

Timing Your Re-Presentation

A few practical considerations worth building into your retry logic:

- UK paydays cluster around the 25th to last working day of the month, so a re-presentation after payday recovers more than one attempted mid-month on a low-balance account.

- The two-working-day notice requirement means you need to plan the re-presentation window in advance, not reactively after a failure lands.

- Hard failures such as account closed or payment stopped require customer action and should not consume your one re-presentation attempt.

With only two attempts allowed, wasting the second on a case that requires customer action directly costs you recovery. Routing those cases to a dunning flow before re-presenting preserves your scheme entitlement for the recoverable soft-decline population.

The Re-Presentation Constraint: Timing, Notice, and Maximum Attempts

Re-presentation rules vary by country, but three principles show up across nearly every regulatory regime: how much notice a merchant must give before retrying, how long a gap must exist between attempts, and how many total attempts are permitted before a payment is considered definitively failed.

In the UK, Bacs rules for Direct Debit require advance notice of collection dates, and re-presentations after an initial unpaid return are limited in both frequency and count. In India, the RBI's mandate framework requires a pre-debit notification at least 24 hours before any retry attempt. Germany's SEPA Direct Debit scheme sets its own return timeframes that affect when a re-presentation is even technically valid.

Getting these wrong carries real cost: failed re-presentations due to timing errors generate return fees, and repeated out-of-window attempts can trigger mandate cancellations that are far harder to recover from than the original payment failure. This is exactly why batch payment retries create compounding problems across multi-country subscriber bases.

Germany and PayPal: Why Billing Agreement Cancellations Create a Distinct Retry Problem

Germany sits in a unique position among major subscription markets. Most retry logic failures trace back to timing or frequency. In Germany, the failure mode is structural: PayPal's billing agreement system means a customer can cancel their agreement directly inside PayPal, bypassing your cancellation flow entirely. The payment doesn't decline with a soft error you can retry. It fails with a hard termination that no retry schedule can reverse.

This matters because Germany is one of Europe's largest subscription markets, and PayPal penetration among German consumers runs exceptionally high. When a billing agreement cancels, your retry engine needs to recognize the failure code as unretryable, suppress further attempts, and route the account to a payment method update flow instead.

The key distinction for retry logic:

- Soft declines signal insufficient funds or temporary issuer holds, making them candidates for rescheduled attempts within regulatory windows.

- Hard billing agreement cancellations signal a deliberate customer action, meaning retrying hard declines wastes attempts and risks flagging your merchant ID for excessive declines.

Getting this classification right protects both recovery rates and your standing with PayPal as a payment processor.

PayPal's Default Retry Schedule and the Subscription Suspension Threshold

PayPal processes subscription billing through its Billing Agreements framework, and when a payment fails, it follows a fixed retry schedule before suspending the subscription entirely.

By default, PayPal retries a failed recurring payment up to three times over a roughly two-week window. The first retry fires 24 hours after the initial decline, the second at day 5, and the third at day 8. If all three retries fail, PayPal suspends the billing agreement and stops attempting the charge.

That suspension threshold matters because reactivation requires explicit customer action. Once suspended, the subscriber must log in and manually approve the agreement again, which creates a meaningful drop-off point for involuntary churn.

What Merchants Can and Cannot Control

Merchants have limited flexibility within PayPal's native retry logic. The retry intervals and the three-attempt cap are set at the billing agreement level and cannot be reconfigured through standard merchant settings, which is one reason smart retries beat fixed retry schedules for subscription billing.

What merchants can control is how quickly they identify the suspension and trigger outreach. Key variables to watch:

- PayPal issues a

PAYMENT.SALE.DENIEDwebhook on each failed attempt, giving merchants a real-time signal to start dunning sequences before the agreement is suspended. - After suspension, the

BILLING.SUBSCRIPTION.SUSPENDEDevent fires, marking the point at which silent retry recovery is no longer possible and customer communication becomes the only path forward. - Reactivation rates drop sharply the longer a subscriber sits in a suspended state, so same-day outreach on the suspension event should be a top priority.

The practical implication: with PayPal subscriptions, the recovery window is short and the handoff from automated retry to customer-facing dunning happens faster than most merchants expect.

Payday Windows and Optimal Retry Timing by Country

Payday cycles vary meaningfully across markets, and retry timing that ignores local pay rhythms leaves recoverable revenue on the table.

In most markets, account balances are highest in the 24 to 72 hours following a paycheck deposit. Payday-aligned payment retries consistently outperform retries fired on a fixed calendar schedule.

Recommended Retry Windows by Region

Here is how pay cadences break down across key subscription markets:

- United States: biweekly pay is standard, with deposits landing on Fridays. The highest-probability retry window runs Friday through Sunday, when checking accounts are freshest.

- United Kingdom: monthly pay dominates, with most salaries hitting on the last working day of the month. Retry attempts in the first three days of the following month capture the strongest balance position.

- Germany: monthly pay arrives between the 25th and the 1st. Retries scheduled for the 26th through the 2nd of the following month align with peak fund availability.

- India: salary disbursement clusters around the 1st and the 7th of each month. Retrying within 48 hours of those dates fits most salaried subscribers.

- Australia: fortnightly pay cycles mirror the US pattern, with Thursday and Friday deposits making the following 48 hours the optimal retry window.

Syncing retry logic to these windows does not require overhauling your billing infrastructure. The timing layer sits on top of existing payment rails and fires based on subscriber location, not a one-size-fits-all schedule.

How Slicker Handles Country-Specific Retry Logic

Country-specific retry rules are not optional compliance overhead. They are a direct input to recovery rates, and ignoring them costs real revenue.

Slicker's AI models ingest regulatory constraints, issuer behavior, and regional payment timing by country before scheduling any retry attempt. For India, that means respecting the RBI's pre-debit notification requirement before each attempt and routing transactions above ₹15,000 INR through the explicit customer approval flow before any charge is executed. For UK Direct Debit, the model accounts for Bacs processing windows and the advance notice rules that govern when a retry can legally run. For Germany, where PayPal cancellations follow distinct dispute flows, the retry logic adjusts accordingly.

The result is a adaptive retry schedule that is compliant by default and tuned to local issuer patterns, not a generic global rule applied everywhere.

Final Thoughts on Country-Specific Retry Logic and Payment Recovery

The rules covered here are not edge cases. India, the UK, and Germany are major subscription markets, and each one sets hard limits on how and when you can retry a failed payment. Getting your retry logic right in each market protects your recovery rates and keeps your merchant standing intact. Talk to the Slicker team if you want to see how country-specific retry scheduling applies to your billing setup.

FAQ

What's the difference between RBI retry rules and UK direct debit retry rules for subscription businesses?

India's RBI framework does not cap the total number of retries, but every attempt must be preceded by a fresh 24-hour pre-debit notification window, and transactions above ₹15,000 INR require the customer to explicitly approve the charge before it can proceed. UK Direct Debit under Bacs gives you one re-presentation after the initial failed collection, with two working days' notice required before that second attempt. The key difference: India's framework is notification-driven with no attempt ceiling, while the UK framework imposes a strict one-re-presentation limit.

Can I use the same retry schedule across India, the UK, and Germany?

No. Each market has distinct rules that a single global schedule will violate in at least one jurisdiction. India's RBI framework requires a 24-hour pre-debit notification before every retry attempt, with no hard cap on attempts but an explicit customer approval requirement for transactions above ₹15,000 INR. UK Bacs limits you to one re-presentation within 30 days. Germany's PayPal billing agreement cancellations are hard terminations, not soft declines, so retrying them directly burns attempts and risks your merchant standing with PayPal.

How do I time a UK direct debit re-presentation to maximize recovery?

Schedule your re-presentation in the 25th-to-last-working-day window of the month, when UK salaries typically land. Because you must give two working days' advance notice before the second attempt, plan the timing proactively after the initial failure, not reactively. Reserve the re-presentation for soft declines tied to temporary insufficient funds; route hard failures like account closed or payment stopped to a dunning flow so you do not waste your one permitted attempt on an unrecoverable case.

What should my retry logic do when a German PayPal billing agreement is cancelled?

Classify the cancellation as a hard termination, suppress further retry attempts immediately, and route the account to a payment method update flow. Unlike a soft decline caused by insufficient funds, a cancelled billing agreement reflects a deliberate customer action that no retry schedule can reverse. Continuing to fire retries risks flagging your merchant ID for excessive declines with PayPal without any recovery upside.

How do country-specific retry rules affect recovery rates in practice?

Following local rules is not a compliance box to tick but a direct input to how many failed payments you recover. Out-of-window retry attempts are rejected at the rail level in India, generating regulatory exposure without any recovery. In the UK, wasting your single re-presentation on a hard failure eliminates all automated recovery for that subscriber. Aligning retry timing to local payday windows targets the 24 to 72 hour window after payroll deposits clear, when account balances are at their highest, and Slicker's AI does this by subscriber geography instead of applying a fixed calendar schedule globally.

Related Articles

How to Build a Retry Allowlist and Blocklist From Declines (July 2026)

I'll be frank: most retry logic is built on assumptions, not data. A retry allowlist tells your system when to try again; a payment retry blocklist tells it...

Smart Retry Timing: Payday & Bank Holidays (June 2026)

You set your retry schedule years ago. Three attempts, maybe four, spaced out by some number of days that felt reasonable at the time. The system fires retries...

Static vs Adaptive Retry: ML Differences (June 2026)

When a payment fails, static retry logic fires on a fixed schedule: day 3, day 7, day 14. Every customer gets the same sequence regardless of why the payment...

Stop losing revenue to failed payments

Join leading subscription businesses using Slicker to recover failed payments automatically.

Get Started