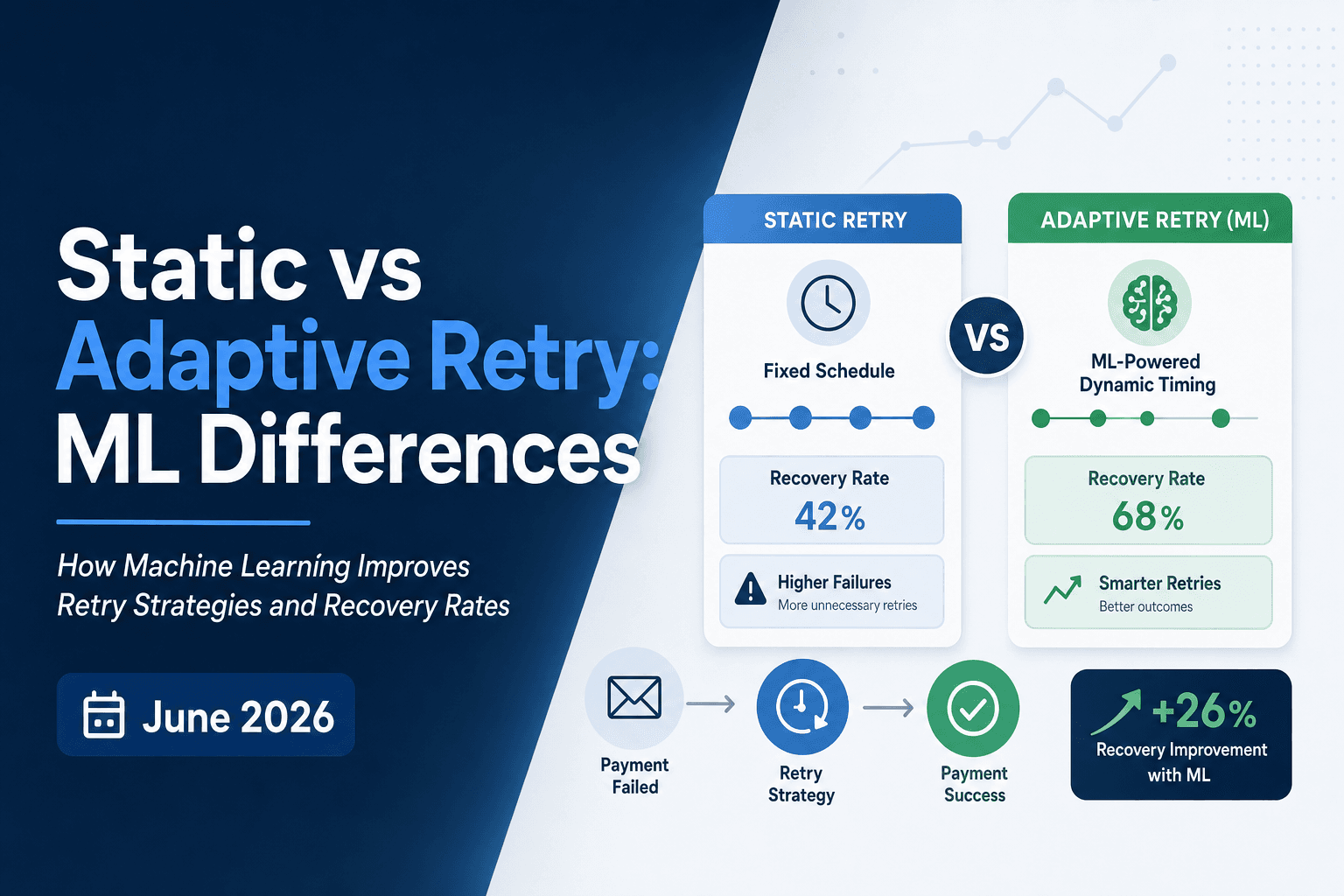

Static vs Adaptive Retry: ML Differences (June 2026)

When a payment fails, static retry logic fires on a fixed schedule: day 3, day 7, day 14. Every customer gets the same sequence regardless of why the payment failed, who their card issuer is, or what day of the month their paycheck lands. Adaptive payment retry changes that calculus. Instead of a fixed schedule, ML retry logic weighs dozens of signals per transaction: decline code, card type, issuer behavior, account history, time of day, and geography. The result is adaptive acceptance that reflects the actual probability of success for that specific card at that specific moment. The performance gap is measurable: static retry schedules recover roughly 20 to 30 percent of failed payments, while adaptive retry approaches push recovery rates into the 40 to 50 percent range for the same subscriber population.

TLDR:

- Static retry schedules recover 20 to 30 percent of failed payments; adaptive AI-driven approaches push recovery into the 40 to 50 percent range for the same subscriber base.

- AI models weigh card type, issuer behavior, decline code, subscriber tenure, and timing context per transaction to decide whether to retry, when, and how often.

- Retry timing matters more than frequency: aligning attempts with payday cycles and issuer-specific windows lifts recovery rates without increasing total retry attempts.

- Following Merchant Advice Codes keeps you compliant with issuers, but adaptive logic treats MACs as one input among many to pick the path with the highest probability of success.

- Slicker's ensemble of AI models analyzes each failed payment individually and proves impact through AABB testing with statistical significance before you pay.

Why Static Retry Schedules Leave Revenue on the Table

Static retry schedules operate on fixed rules: retry on day 3, day 7, day 14. Every customer gets the same sequence regardless of why the payment failed, who their card issuer is, or what day of the month their paycheck lands.

The problem is that decline reasons vary widely. A soft decline from insufficient funds on a Thursday before payday is a very different situation than a card flagged for suspected fraud. Retrying both with the same timing and frequency is no better than guessing.

The financial cost of that guessing adds up. Industry data shows roughly 15% of recurring payments are declined, and a meaningful share of those are recoverable soft declines that static logic simply misses by retrying at the wrong time.

What Static Logic Gets Wrong

- Timing is generic, not issuer-aware: card networks and individual issuers have different authorization windows, but static schedules ignore that entirely and retry at arbitrary intervals.

- No account is taken of cardholder pay cycles: a retry on day 3 after a paycheck-timing failure often lands before funds are available, burning an attempt unnecessarily.

- Every failed payment looks the same: static logic cannot separate recoverable soft declines from hard declines that will never succeed, so it wastes retries on unrecoverable failures.

Each missed recovery is MRR you already earned, from a customer who already said yes.

What Makes a Retry Strategy Adaptive

A static retry strategy runs on rules someone wrote once: wait three days, try again, repeat. It doesn't know whether the decline was a soft temporary hold or a hard network rejection. It doesn't know the cardholder's pay cycle, the issuer's processing patterns, or whether a prior retry attempt already triggered a fraud flag.

Adaptive retry logic works differently. It reads the decline code, the transaction history, the card type, the issuer behavior, and the timing context before deciding whether to retry at all, and if so, exactly when.

There are a few properties that separate a genuinely adaptive approach from one that just adds more variables to a static schedule:

- The retry decision is made per-transaction, not per-segment. Each failed payment gets its own analysis based on its own signal set through smart dunning.

- The system learns from outcomes. A retry that succeeds on a Tuesday morning for a particular issuer feeds back into the model's next decision.

- Timing is treated as a variable, not a constant. Retry windows shift based on geography, card type, and issuer behavior instead of a fixed interval.

When these properties are in place, the retry logic stops being a schedule and starts behaving more like a decision engine, one that gets more accurate as it processes more data.

How AI Models Decide When to Retry

When a payment fails, the system has to make a decision: retry now, wait, or stop entirely. Static retry logic answers that question the same way every time. AI models don't.

The decision tree in an adaptive retry system weighs a range of inputs simultaneously. Card type, issuer behavior, decline code, time of day, subscriber tenure, geography, and historical recovery patterns for that specific BIN (bank identification number) all factor in. A soft decline on a debit card from a regional bank on a Friday afternoon carries a different probability of recovery than the same code on a premium credit card mid-month.

Here's what that looks like in practice:

- Soft declines flagged as insufficient funds get routed toward end-of-month retry windows, when balances are more likely to have refreshed after payroll cycles.

- Declines tied to suspected fraud holds get deprioritized for immediate retry, since hammering the card can trigger a hard block from the issuer.

- High-tenure subscribers with strong payment history get more retry attempts, because their lifetime value warrants the increased retry spend.

The result is a retry schedule that varies by customer, card, issuer, and timing instead of applying a fixed cadence to every failed payment. That specificity is what separates adaptive acceptance from static dunning logic, and where recovered revenue actually comes from.

The Performance Gap Between Static and Adaptive Retries

Static retry logic operates on a fixed schedule: attempt payment on day 1, day 3, day 7, and so on, regardless of what caused the decline. Every account gets the same treatment whether the failure was a soft decline from a temporarily frozen card or a hard decline from a closed account.

Adaptive payment retry changes that calculus. Instead of a fixed schedule, AI-driven retry logic weighs dozens of signals per transaction: decline code, card type, issuer behavior, account history, time of day, and geography. The result is a retry decision that reflects the actual probability of success for that specific card at that specific moment.

The performance gap is measurable. Industry data shows static retry schedules recover roughly 20 to 30 percent of failed payments. Adaptive acceptance approaches, which route each retry based on real-time signal weighting, push recovery rates into the 40 to 50 percent range for the same subscriber population.

Characteristic | Static Retry Schedules | Adaptive Payment Retry (AI-Driven) |

|---|---|---|

Recovery Rate | 20 to 30% of failed payments | 40 to 50% of failed payments |

Retry Timing | Fixed intervals (day 3, 7, 14) regardless of context | Per-transaction timing based on card type, issuer behavior, decline code, and payday cycles |

Decision Logic | Same sequence for every customer | Dozens of signals weighed simultaneously per transaction |

Issuer Awareness | Generic timing, no issuer-specific optimization | Aligns with issuer-specific authorization windows and behavior patterns |

Adaptation Over Time | Degrades silently as issuer behaviors shift | Recalibrates continuously based on outcome data |

Treatment of Decline Codes | All soft declines treated identically | Insufficient funds vs. fraud holds vs. frozen accounts routed differently |

Why the Gap Widens Over Time

Static schedules degrade silently. Issuer behaviors shift, card portfolios age, and the fixed rules that worked at launch become less accurate without anyone noticing.

Adaptive retry logic recalibrates continuously against incoming outcome data, so the model stays current with issuer-level changes without drifting behind them. For a subscription business processing tens of thousands of renewals monthly, that compounding accuracy difference translates directly into recovered MRR.

Merchant Advice Codes and the Limits of Following Network Guidance

Merchant Advice Codes (MACs) give issuers a way to signal exactly why a payment failed and what the merchant should do next. In theory, following that guidance should recover the transaction. In practice, MAC compliance is a floor, not a ceiling.

The codes themselves are static. They tell you what happened, not what will work for this specific subscriber, on this card, at this issuer, given what your retry history already looks like. A MAC might say "retry in 72 hours." But if that subscriber's card has failed three times in the past two weeks, a fourth retry inside that window will almost certainly fail again, and may push the issuer toward a hard block.

This is where adaptive payment retry and ML retry logic pull ahead. Instead of treating MAC guidance as the complete answer, an AI-powered system treats it as one input among many. The model weighs the MAC alongside card type, issuer behavior patterns, subscriber tenure, and historical retry outcomes to pick a path with a higher probability of success.

The gap between MAC compliance and actual recovery rates is where lost revenue sits. Following network guidance keeps you out of trouble with issuers; adaptive acceptance is what gets the money back.

Why Timing Matters More Than Frequency

Retry timing is one of the most overlooked variables in payment recovery. Most static systems operate on a fixed cadence: attempt on day 1, day 3, day 7. That schedule was designed for average behavior, not your actual subscriber base.

The problem is that payment success rates shift throughout the month. Cardholders who get paid biweekly have funds available on specific days. Someone on a prepaid card may top it up on payday. A soft decline on a Tuesday morning looks very different from the same decline on Friday afternoon.

Here is where adaptive retry logic changes the outcome. Instead of spacing retries evenly, an AI-driven system reads signals like:

- Decline code patterns that suggest a temporary cash shortfall vs. a frozen account

- Issuer-level behavior that hints at the most receptive retry window

- Historical success data tied to day-of-week and time-of-day for that card type

The result is retries that land when approval probability is highest, not simply when the calendar says to try again. For high-volume subscription businesses, that difference in timing alone can move recovery rates meaningfully without increasing total retry attempts or risking issuer flagging for excessive retries. Industry research on retry strategies confirms that timing adaptation based on issuer-specific behavior patterns consistently outperforms fixed-interval approaches.

Slicker's AI-Powered Payment Recovery for Subscription Businesses

Slicker is built for subscription businesses dealing with involuntary churn from failed payments. Where static retry logic fires on a fixed schedule regardless of context, Slicker's ensemble of AI models analyzes card type, issuer behavior, geography, decline code, and account history to decide whether to retry, when, and at what frequency. Machine learning approaches to authorization optimization have delivered measurable improvements over rule-based systems by processing transaction context in real time.

The result is adaptive payment retry that responds to each transaction's actual failure signal instead of a preset rule. A soft decline from a temporarily frozen account gets treated differently from a decline triggered by insufficient funds on a known payday cycle.

Recovery happens silently, without customer involvement. Dunning emails are reserved for cases where action is genuinely required, like an expired or stolen card, and those communications go out under your brand and domain.

Slicker proves its impact through clinical-grade AABB testing: your traffic splits 50/50, dollars recovered are measured directly, and results include a p-value. If Slicker's adaptive acceptance logic doesn't beat your control with statistical significance, you don't pay.

Final Thoughts on What Separates a Schedule From a Decision Engine

A retry fired three days after a soft decline isn't a strategy, it's a guess. The question isn't whether to retry, it's whether this specific card, at this issuer, on this day, will approve if you try again. Adaptive payment retry answers that question with transaction-level precision instead of applying the same rule to every failed payment. For subscription businesses processing tens of thousands of renewals monthly, that precision gap is the difference between recovering 30% and recovering 50%.

FAQ

Can I build adaptive payment retry without machine learning?

No. Rule-based retry schedules can add more variables (segment by plan type, add geography filters), but they still apply fixed logic to entire groups instead of making per-transaction decisions that learn from outcomes. Adaptive acceptance requires AI models that weigh dozens of signals simultaneously and recalibrate based on what actually succeeds.

Adaptive payment retry vs static retry: what's the actual revenue difference?

Static retry schedules recover roughly 20 to 30 percent of failed payments. Adaptive acceptance approaches, which route each retry based on real-time signal weighting, push recovery rates into the 40 to 50 percent range for the same subscriber population. That performance gap translates directly into recovered MRR.

Should I follow Merchant Advice Codes or optimize for recovery?

Both, selectively. Merchant Advice Codes tell you what the issuer recommends, not what will maximize recovery within your dunning window. When a MAC prescribes "retry in 10 days" but your dunning expires in 5, following network guidance means missing the recovery entirely. Adaptive retry logic weighs MAC recommendations against business constraints, historical recovery data, and dunning deadlines to find the optimal attempt within the time you actually have.

How does ML retry logic decide when to retry a soft decline?

AI models weigh card type, issuer behavior, decline code, subscriber tenure, geography, and historical recovery patterns for that specific BIN before picking a retry window. A soft decline on a debit card from a regional bank on a Friday afternoon gets a different timing decision than the same code on a premium credit card mid-month. The system learns from each outcome, so retry timing gets more accurate as it processes more data.

Related Articles

How to Build a Retry Allowlist and Blocklist From Declines (July 2026)

I'll be frank: most retry logic is built on assumptions, not data. A retry allowlist tells your system when to try again; a payment retry blocklist tells it...

Country Retry Rules: India RBI, UK Direct Debit & Germany PayPal July 2026

Failed payment recovery looks very different depending on where your customer is. India's RBI retry rules limit attempts and require pre-debit notifications...

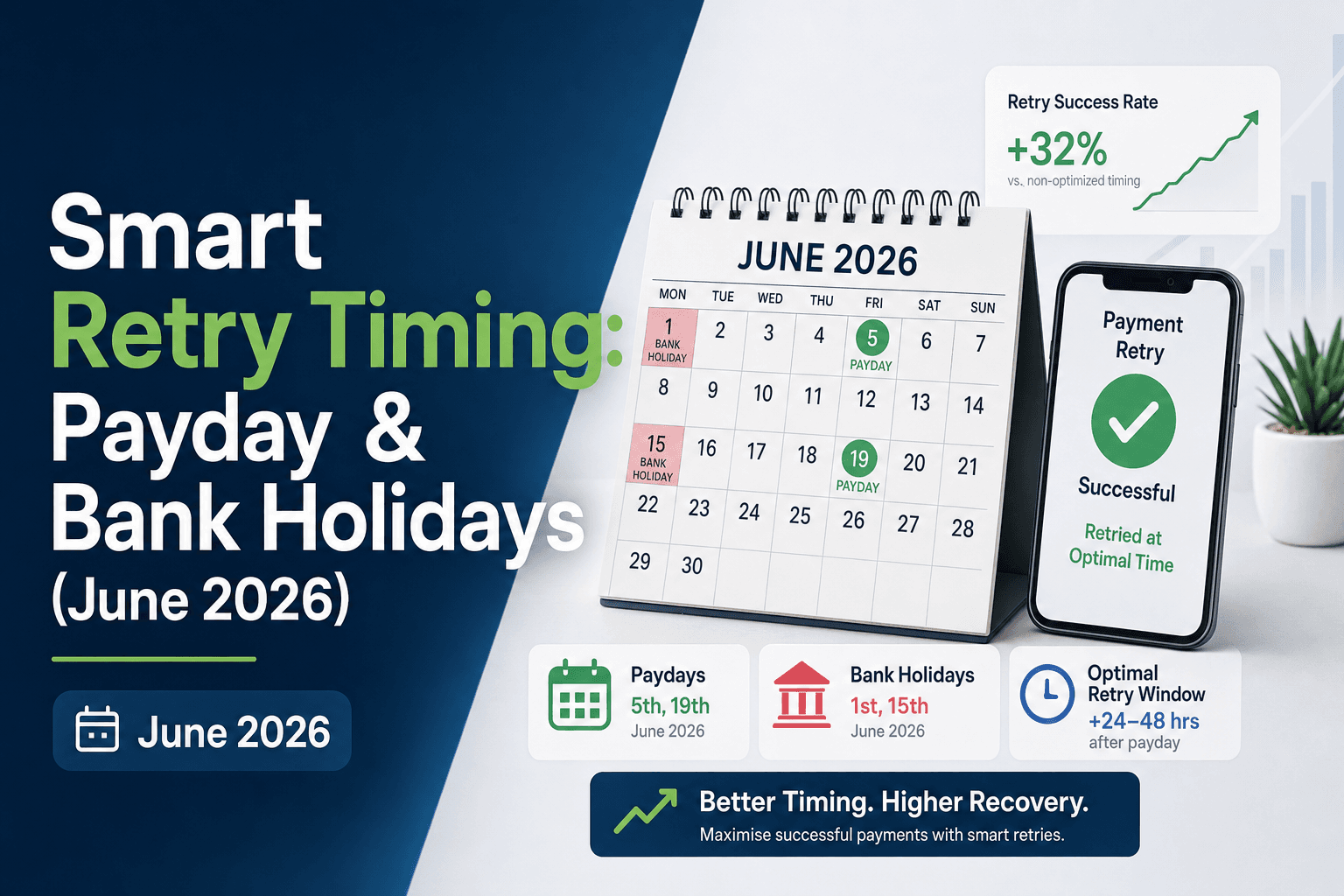

Smart Retry Timing: Payday & Bank Holidays (June 2026)

You set your retry schedule years ago. Three attempts, maybe four, spaced out by some number of days that felt reasonable at the time. The system fires retries...

Stop losing revenue to failed payments

Join leading subscription businesses using Slicker to recover failed payments automatically.

Get Started