How Many Times Should You Retry a Failed Subscription Payment? Data and Limits (June 2026)

Every failed subscription payment puts you at a fork in the road. Retry it and you might recover the revenue you already earned, or you might burn an attempt on a decline that was never recoverable and inch closer to card network penalties. Don't retry at all and you lose the subscriber to involuntary churn before they notice anything went wrong. The right number of payment retry attempts sits between those extremes, and it's not the same for every decline. Soft declines warrant multiple tries. Hard declines warrant zero. Getting the count right means understanding retry limits, timing your attempts around when customers actually have funds, and stopping before diminishing returns turn recovered MRR into expensive noise.

TLDR:

- Subscription payments fail at 15% per month; 3 to 6 retry attempts recover most soft declines.

- Visa caps retries at 15 attempts in 30 days, Mastercard at 10; fines start at $25 per breach.

- First retry recovers 40-60% of soft declines; gains drop fast after attempt three.

- Timing retries to payday cycles (1st and 15th in US, month-end in Europe) cuts attempts needed.

- Slicker's AI models analyze decline codes and issuer behavior to set retry counts per transaction.

Why Subscription Payments Fail More Often Than One-Time Transactions

Subscription payments carry a structural disadvantage that one-time transactions don't: they repeat automatically, without the cardholder actively re-confirming at checkout. That passive nature creates a gap between when a card was valid and when a charge actually runs.

Card details change constantly. Issuers reissue cards after fraud events, expiration cycles turn over, and spending limits fluctuate with account activity. roughly 15% of recurring payments are declined in any given billing cycle, compared to much lower rates for one-time purchases where the cardholder is present and engaged.

The failure modes split into two categories worth keeping separate:

- Soft declines are recoverable. The card exists and the account is in good standing, but something temporary blocked the charge: insufficient funds, a velocity limit, or a risk flag the issuer raised. These respond well to retries.

- Hard declines are not recoverable through retries. The card is stolen, the account is closed, or the issuer has issued a do-not-honor instruction. Retrying these wastes attempts and risks card network penalties.

Getting the retry count right starts with knowing which failure type you're dealing with. Retrying a hard decline isn't a recoverable situation, and treating it like one is where most retry strategies break down.

Soft Declines vs. Hard Declines: The Critical Distinction That Determines Whether to Retry

Before retrying any failed payment, you need to know whether the decline is recoverable. Soft declines are temporary, meaning the transaction was rejected due to conditions that may resolve on their own: insufficient funds, a bank timeout, or a generic processing error. Hard declines are permanent. The card is stolen, closed, or flagged as fraudulent. Retrying a hard decline accomplishes nothing and risks triggering issuer blacklists.

The retry math changes entirely based on this distinction. Soft declines warrant multiple attempts spaced strategically. Hard declines require zero retries and immediate customer outreach instead.

Card Network Retry Limits: Visa and Mastercard Rules You Cannot Ignore

Both Visa and Mastercard have published retry limits that override any internal dunning logic you've built.

Visa's rules cap excessive retries at 15 attempts in 30 days for a single card and merchant combination. Mastercard takes a stricter line: no more than 10 retries in 30 days for declined transactions. Breaching these limits triggers fines starting at $25 per transaction, and repeated violations can escalate to higher per-transaction fees or suspension of retry privileges on that merchant ID.

These aren't soft guidelines. They are enforceable rules, and processors monitor compliance automatically.

Card Network | Maximum Retry Attempts in 30 Days | Penalty for Breaching Limit | Recommended Safe Ceiling |

|---|---|---|---|

Visa | 15 attempts per card and merchant combination within 30 days | Fines starting at $25 per transaction, escalating penalties for repeated violations | Stay below 10 attempts to maintain headroom for legitimate recovery windows |

Mastercard | 10 attempts per declined transaction within 30 days | Fines starting at $25 per transaction, potential suspension of retry privileges | Build retry logic with 6 to 8 attempts maximum to avoid network scrutiny |

How This Applies to Your Retry Count

If you're running more than 10 attempts per billing cycle, you're at risk of a fine and likely deep into diminishing returns territory well before that ceiling. The network limits exist partly because the data already shows that repeat retries on the same decline rarely succeed after the first few attempts.

The practical guardrail here is to treat the Mastercard 10-attempt cap as your absolute ceiling, build your internal retry logic well below it, and reserve headroom for legitimate recovery windows like payday cycles or card refresh events.

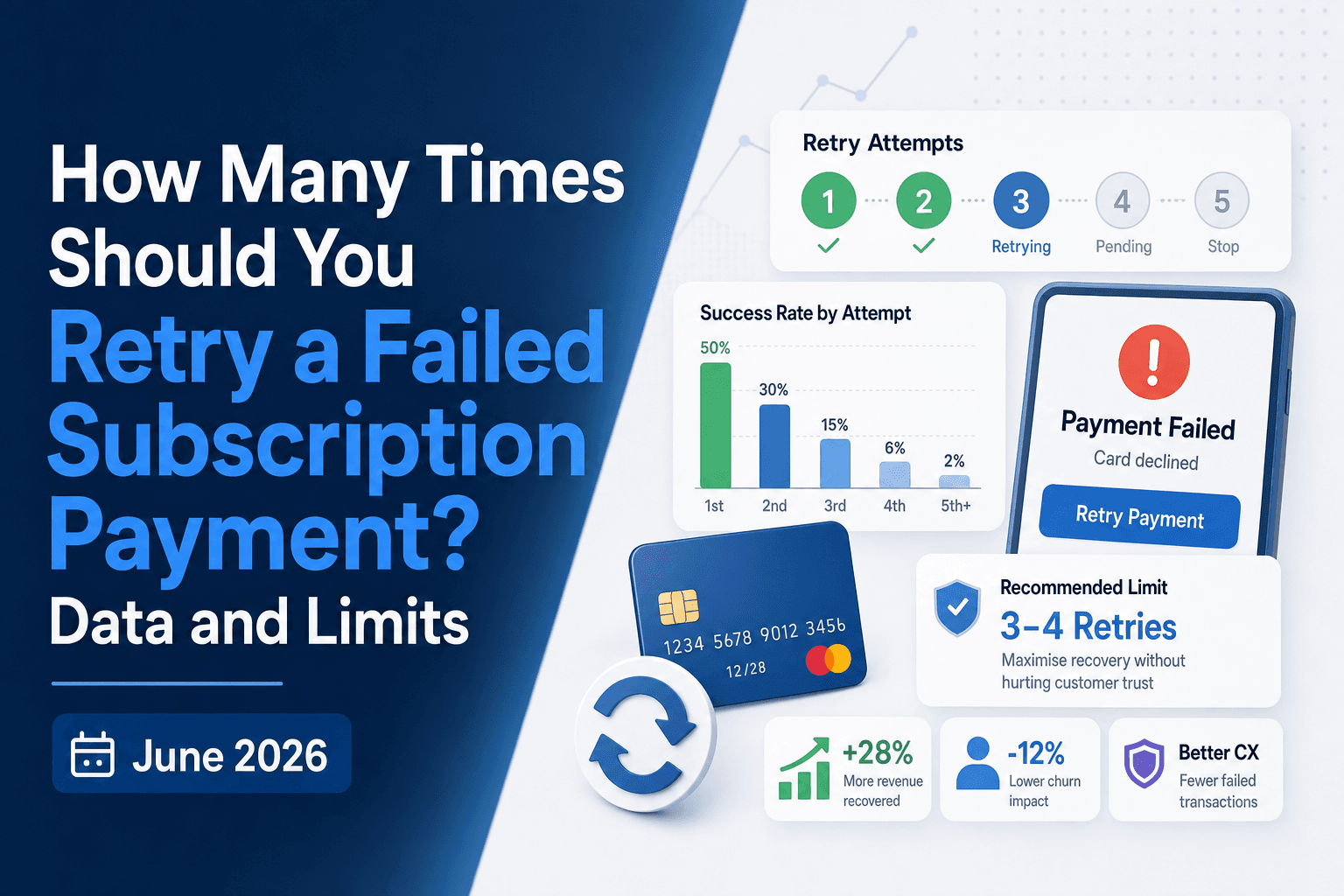

How Many Times Should You Actually Retry? The Practical Answer

Most subscription businesses should plan for 3 to 6 retry attempts per failed payment cycle before pausing outreach. Industry data suggests recovery rates drop sharply after the third attempt, with the majority of recoverable payments resolving within the first two retries. Beyond six attempts, the incremental recovery gain rarely outweighs the issuer relationship risk or the cardholder friction.

A practical retry window runs 5 to 14 days from the initial decline. Retrying too quickly signals desperation to issuers; waiting too long loses the customer to involuntary churn before they notice the problem.

The right number also depends on decline type:

- Soft declines (insufficient funds, temporary holds) warrant the full 3 to 6 spaced attempts to catch paydays and balance refreshes.

- Hard declines (stolen card, closed account) should stop after one attempt. Retrying these wastes authorization attempts and can flag your merchant ID for abuse.

Three to six retries is a starting point, not a rule. The actual ceiling for your business depends on your subscriber mix, average billing amount, and issuer relationships - variables that only live transaction data can answer.

Recovery Rate Benchmarks: What You Should Expect From Your Retry Strategy

Industry benchmarks give you a useful sanity check before you fine-tune your own retry logic. First-attempt recovery rates on soft declines typically land between 20% and 40%, depending on your subscriber base, average order value, and billing model. A well-structured retry sequence across three to five attempts can push cumulative recovery to 60% or higher for accounts with soft-decline history.

What Drives the Spread?

Results vary widely because the inputs vary widely. Three factors account for most of the gap between a 25% recovery rate and a 60% one:

- Retry timing relative to the customer's pay cycle matters more than raw retry count. Hitting a card two days before a known payday consistently outperforms hitting it the morning after a decline.

- Decline code specificity changes everything. Generic "do not honor" codes require a different cadence than insufficient-funds codes, which have a predictable resolution window you can target.

- Issuer behavior by card type and geography changes recovery odds meaningfully. A debit card tied to a paycheck-to-paycheck account behaves differently from a premium travel card with a high credit limit.

Subscription businesses that account for all three factors in their retry logic tend to land in the upper half of that benchmark range. Those running fixed schedules without code-level logic typically cluster at the lower end. The dollars separating those two outcomes compound fast when you're processing thousands of failed payments each month.

Timing Your Retries: When Matters More Than How Many

Retry timing shapes recovery rates as much as retry count does. Industry data shows that most recoverable soft declines resolve within 24-72 hours; spacing retries too tightly wastes attempts and may trigger issuer-side blocks.

A few timing principles hold up across high-volume subscription data:

- Retry within 24 hours of a soft decline for the best recovery odds, since many insufficient-funds declines clear quickly after payroll or account top-ups.

- Space subsequent attempts 3-5 days apart to avoid pattern flags that some issuers use to deprioritize repeated failures from the same merchant.

- Align retries to known pay cycles where possible, particularly for weekly-paid or bi-weekly-paid customer segments.

Timing your retries well means fewer total attempts are needed to hit the same recovery rate.

Merchant Advice Codes: Reading the Network's Instructions on Whether and When to Retry

Merchant Advice Codes (MACs) are standardized instructions card networks send back with a decline, telling you exactly what to do next. Ignoring them is one of the most common retry mistakes subscription businesses make.

What MACs Actually Tell You

Each code maps to a specific action:

- MAC 01 means the card has been replaced; retrying is pointless until the customer updates their payment method.

- MAC 02 means try again later, a genuine soft decline where a retry can succeed.

- MAC 03 signals the customer has cancelled; retrying here risks complaints and disputes.

Why This Matters for Retry Limits

Your retry count should not be a flat number applied universally. A MAC 02 warrants further attempts. A MAC 01 or 03 means no retry count is appropriate at all; the right move is immediate customer outreach or cancellation handling. Treating all declines the same wastes attempts on unrecoverable transactions while potentially missing recoverable ones, directly eroding your recovered MRR.

Payday-Aligned Retry Windows: Geographic and Employment Pattern Optimization

Timing retries around when customers actually have money in their accounts is one of the most underutilized levers in payment recovery. Payday cycles vary widely by country and employment type, so a one-size-fits-all retry schedule leaves recoverable revenue on the table.

Here are concrete retry windows by region:

- US: retries on the 1st and 15th for salaried employees, and Fridays for hourly workers paid weekly or biweekly. Avoid the 25th-31st window when accounts are typically at their lowest.

- Western Europe: Most salaried workers receive pay on the last working day of the month. Concentrate retry attempts in the first three days of the new month when balances are freshest.

- Australia: Fortnightly pay cycles are standard, with most deposits landing on Thursdays. Schedule retries for Thursday afternoons through Friday mornings to catch funds before weekend spending clears accounts.

Aligning retry timing to these windows reduces the number of attempts needed to recover a payment, which in turn lowers the risk of triggering issuer fraud flags from repeated declines. Fewer retries with better timing recover more revenue at less reputational cost to your merchant ID.

The Revenue Impact: Quantifying What Failed Payment Retries Actually Recover

10 to 15% of payments fail in any given month. For a business with $10M in monthly recurring revenue, that means $1 to 1.5M in revenue is immediately at risk every 30 days.

Not all of that is lost permanently. A well-structured retry sequence recovers a meaningful share before a subscriber ever knows there was a problem. But the size of that recovery window depends heavily on how many attempts you make and when.

Research from subscription billing providers suggests that the first retry attempt recovers approximately 40 to 60% of initially declined soft declines. Each subsequent attempt yields diminishing returns, with second attempts recovering an additional 15 to 25% of the remaining pool, and third attempts capturing another 10 to 15%.

How This Applies to Your MRR

The math compounds quickly across your subscriber base. If you run no retries at all, involuntary churn absorbs the full 10 to 15% monthly failure rate. Add a single retry and you recover the majority of recoverable soft declines. Add two more well-timed attempts and you close the gap further, with each incremental retry requiring less effort for smaller gains.

The ceiling matters too. Beyond three to four attempts, recovery rates flatten and risks rise. The optimal retry count sits in a range where recovered revenue outweighs the cost of failed attempts, chargebacks, and account suspensions.

The revenue math here is straightforward. Industry data shows roughly 10-15% of recurring subscription payments fail each month. For a business with $10M in monthly recurring revenue, that puts $1-1.5M at risk every 30 days.

A well-structured retry sequence recovers a meaningful share before a subscriber notices anything. Research from subscription billing providers shows the first retry attempt recovers approximately 40-60% of soft declines. A second attempt picks up another 15-25% of the remaining pool, and a third captures an additional 10-15%.

Where Diminishing Returns Set In

The gains compress fast. Beyond three to four attempts, recovery rates flatten while the risk of card network penalties and issuer friction climbs. Recovered revenue has to outweigh the cost of failed attempts, chargebacks, and potential account suspensions. Get the count wrong in either direction and you leave money on the table or invite consequences that cost more than the revenue you were chasing.

Slicker's Evidence-Based Approach to Retry Limits and Recovery

Slicker treats retry limits as an evidence-based question instead of a fixed rule. Rather than applying a one-size-fits-all number, Slicker's AI analyzes each failed payment individually, weighing signals like decline code, issuer behavior, card type, and customer history to decide whether a retry has a realistic chance of success.

The result is that retry counts vary by situation. Some accounts recover on the first retry; others warrant more attempts spread across a longer window. The AI sets the limit based on evidence, not convention.

This matters because unnecessary retries carry real costs: higher decline rates, issuer flags, and involuntary churn that could have been avoided with better timing. Slicker's approach keeps retry attempts within ranges that protect your relationship with issuers while recovering the MRR you've already earned.

Final Thoughts on Retry Limits That Balance Recovery and Risk

You need enough attempts to catch recoverable soft declines without crossing into territory where issuers start flagging your merchant ID or card networks fine you for excessive retries. Three to six attempts spaced across 5 to 14 days gives you the recovery window without the risk, as long as you're reading Merchant Advice Codes and stopping immediately on hard declines. Get in touch if you want to see how Slicker's AI determines whether each failed payment warrants one retry or five based on decline code, issuer behavior, and your customer's payment history.

FAQ

How many retries failed payment should I attempt before stopping?

Plan for 3 to 6 retry attempts per failed payment cycle. Recovery rates drop sharply after the third attempt, with most recoverable payments resolving within the first two retries. Beyond six attempts, incremental recovery gains rarely outweigh the issuer relationship risk or cardholder friction.

Can I build a payment retry strategy without hitting Visa or Mastercard limits?

Yes, but you need to stay well below the published caps. Mastercard limits you to 10 retries in 30 days per card, and Visa caps at 15 attempts. Build your retry logic with fewer attempts than these ceilings to avoid fines and maintain headroom for legitimate recovery windows like payday cycles or card refresh events.

What's the difference between soft declines and hard declines for retry attempts subscription?

Soft declines are recoverable failures like insufficient funds or temporary holds that warrant 3 to 6 retry attempts spaced across your payment window. Hard declines are permanent blocks like stolen cards or closed accounts that should stop after one attempt, since additional retries waste authorization attempts and can flag your merchant ID for abuse.

Should I retry payments on the same schedule regardless of decline code?

No. Merchant Advice Codes tell you exactly what to do next. MAC 02 means try again later and warrants further attempts. MAC 01 signals the card has been replaced, making retries pointless until the customer updates their payment method. MAC 03 means the customer has cancelled, so retrying risks complaints and disputes. Your retry count should vary based on these network instructions.

When should I time my retries to maximize recovery rates?

Align retries to customer pay cycles by geography. In the US, target the 1st and 15th for salaried employees and Fridays for hourly workers. Western Europe sees most salary payments on the last working day of the month, so concentrate retries in the first three days. Australia's fortnightly cycles hit Thursdays. Fewer retries with better timing recovers more revenue at less reputational cost.

Related Articles

Code 51 Declines: Insufficient Funds Recovery Playbook (August 2026)

Not every failed payment means a lost customer, and code 51 is probably the clearest example of that. Your subscriber's card is fine; their balance was just...

Failure Reason Dunning Cadence: Route Every Decline Right (August 2026)

A payment failure is a signal, and the signal means something different depending on the decline code behind it. Treating them all the same way, one email...

What to Send in Payment Failure Emails at Each Attempt (July 2026)

A recurring payment failure email on attempt 1 should feel like a friendly heads-up. By attempt 5, that same friendly tone reads as if you're not paying...

Stop losing revenue to failed payments

Join leading subscription businesses using Slicker to recover failed payments automatically.

Get Started