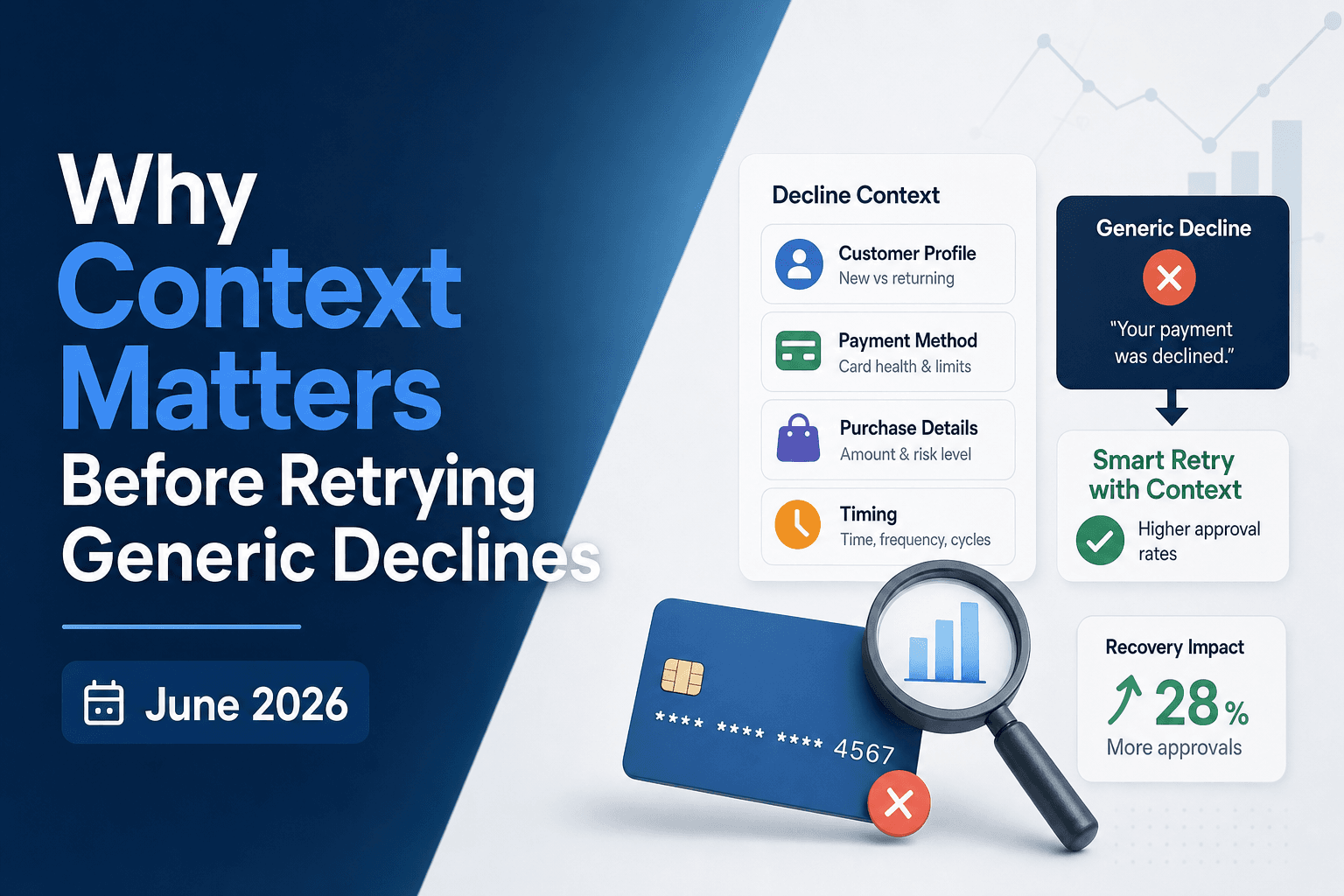

Why Context Matters Before Retrying Generic Declines (June 2026)

You get a generic_decline code back from the issuer. No detail. No hint about whether this is a temporary glitch or a permanent block. Your retry logic fires anyway, because that's what it's built to do. But here's the issue: a generic decline can hide dozens of distinct root causes, and each one calls for a different retry strategy. Insufficient funds on a prepaid card that gets refilled weekly is retryable. A fraud flag that the issuer won't move on is not. Treating every vague payment error the same way means you're either leaving recoverable revenue on the table or hammering cards that will never clear and pushing your account into higher decline-velocity territory. The difference between recovering a payment and losing a subscriber is reading the context before you retry.

TLDR:

- Generic decline codes mask dozens of causes (fraud flags, velocity limits, insufficient funds). Retrying blind wastes attempts and risks triggering issuer velocity flags that make future recovery harder.

- Merchant Advice Codes (MACs) turn vague errors into directives. MAC 21 bans retries; MAC 03 requires customer contact. Ignoring these risks fraud flags and account damage.

- Retry timing by cause: 24-48 hours for issuer congestion, payday windows (1st/15th US, Fridays UK/AU) for insufficient funds, 3-5 days for unknown card issues.

- Silent retry resolves technical failures without customer friction. Dunning only works when customer action is required (expired or stolen card).

- Slicker reads card type, BIN, geography, and decline history to assign confidence scores before scheduling retries or routing to dunning.

What Generic Decline Error Codes Actually Mean

When a payment fails with a generic decline, the issuing bank is deliberately withholding the real reason. Codes like generic_decline or do_not_honor are catch-all responses from payment processors that can mask dozens of distinct underlying causes: insufficient funds, velocity limits, fraud scoring, BIN restrictions, or issuer-side technical failures.

The problem with retrying these blind is that each underlying cause calls for a different response. Retrying a card flagged for fraud triggers additional fraud scoring. Retrying during a temporary issuer outage just burns retry attempts against a hard cap.

Why Generic Declines Are Harder to Diagnose Than Specific Error Codes

When a payment fails with a code like do_not_honor or insufficient_funds, you have a clear signal. Generic declines give you nothing actionable.

A generic_decline or a generic error typically means the issuing bank rejected the transaction without explaining why. It could be a temporary system hiccup, a fraud flag, a velocity check, or a card that's simply been flagged for unrelated activity. Retrying blindly treats all of those situations the same way, which is exactly the wrong approach. Smart dunning uses context to distinguish between these scenarios.

Most failed payment systems don't hold context between attempts, so each retry hits the issuer cold.

The Critical Difference Between Retryable and Non-Retryable Generic Declines

When a payment comes back as a generic decline, the instinct to retry immediately is understandable, but acting without context is where revenue leaks start. Not every generic_decline error is the same, and the retryable versus non-retryable distinction is what separates a recovered payment from a churned subscriber.

A raw generic_decline code alone tells you nothing about whether you're looking at a temporary issuer hiccup or a permanently blocked card. Getting that wrong costs you in two directions: miss a retryable decline and you lose a subscriber who wanted to stay; hammer a non-retryable one and you burn retry budget while risking velocity flags that make future attempts harder.

There are two broad categories that a vague payment error like generic_decline can hide.

Retryable generic declines

These reflect temporary issuer-side conditions: network timeouts, processor overload, or momentary insufficient funds on a card that gets replenished on payday. Timing and retry interval matter here, but the underlying intent to pay is still intact.

Non-retryable generic declines

These point to something more durable: a flagged account, a blocked card, or a risk threshold the issuer will not move on. More retries will not change the outcome and can actively worsen it by triggering velocity flags on the account.

Without behavioral signals, issuer patterns, and account history, every retry on a generic decline error is a guess. That context is exactly what needs to precede any retry decision.

How Merchant Advice Codes Add Context to Generic Bank Responses

When a bank sends back a generic decline, it often includes a secondary signal that most retry logic ignores entirely: a Merchant Advice Code (MAC). Visa and Mastercard issue these codes alongside certain decline responses to tell merchants exactly what to do next.

What MACs Actually Tell You

A MAC gives you a concrete directive instead of forcing you to guess. Card networks like Mastercard use MACs to signal when retries are appropriate versus irreversible. A few examples:

- MAC 01 tells you the customer's account needs to be updated before any payment can succeed.

- MAC 03 indicates the issuer wants the customer to contact their bank before any retry is attempted.

- MAC 21 signals that retrying this transaction is not permitted, period.

Ignoring these codes and retrying anyway wastes a retry attempt and does more damage. It can trigger fraud flags, damage your merchant account standing, or push a soft decline into a hard one. The MAC turns a vague payment error into an actionable instruction, and reading it before retrying is the difference between a recovered payment and a permanently churned customer.

When to Retry Generic Declines (And When to Stop)

Retrying a generic decline without context is one of the more expensive guesses in subscription billing. The code tells you nothing about cause, so the decision tree has to rely on signals outside the code itself.

A few situations where a retry is worth attempting:

- The card is confirmed active and the account is in good standing, but network congestion or a processor timeout likely caused the failure.

- The customer recently updated their billing details, which suggests the prior decline was stale data.

- Issuer response patterns for that BIN suggest a temporary hold instead of a standing block.

A few situations where retrying will make things worse:

- Multiple sequential generic declines on the same card within a short window, which signals the issuer is actively blocking the merchant.

- No behavioral or account signal that separates this failure from a hard block dressed up in a soft-decline code.

- The account shows signs of involuntary churn (failed payment) layering on top of voluntary churn signals (low login activity, support complaints), where a customer-facing communication is the right move instead.

The underlying principle: generic declines require you to build a case from surrounding context before committing to a retry. Without that case, you are spending retry attempts and risking issuer flagging with no meaningful probability improvement over a coin flip.

Optimal Retry Timing for Different Generic Decline Scenarios

Timing your retry after a generic decline error isn't guesswork; it's a function of what's likely causing the failure underneath the vague code. Building a smart retry strategy requires understanding these underlying causes.

Retry Windows by Likely Cause

Before choosing a retry window, consider the probable root cause:

Likely Root Cause | Recommended Retry Window | Rationale |

|---|---|---|

Temporary issuer congestion or processing hiccup | 24-48 hours | Network timeouts and processor overload typically clear within this window; same-day or next-day retry is reasonable. |

Suspected insufficient funds | Align with payday cycles: 1st/15th (US), Fridays (UK/AU), bi-weekly (Canada) | Cards get replenished on predictable schedules; waiting until common payday windows maximizes recovery probability. |

Unknown card-level issues | 3-5 days | Gives the issuer time to resolve flags without triggering additional decline signals or velocity blocks. |

Why Blind Immediate Retries Hurt You

Retrying the same card seconds after a generic decline raises your decline velocity, which issuers track. High decline velocity can push subsequent attempts into harder decline territory, shrinking your recovery window on transactions that were recoverable in the first place.

Why Silent Recovery Beats Dunning for Generic Technical Failures

When a generic_decline comes back with no issuer detail, retrying blindly wastes attempts and risks triggering velocity filters. Silent retry logic handles this better because it acts without customer involvement, testing the transaction against issuer availability and timing patterns before escalating.

For generic technical failures, the retry itself is the diagnostic. A well-timed second attempt often resolves the error before the customer ever notices a problem.

Dunning is the right tool when customer action is required, like an expired card or a stolen credential. For vague payment errors with no actionable cause, it creates unnecessary friction and signals a payment problem the customer may not be able to fix.

The Hidden Cost of Retrying the Wrong Generic Declines

Retrying a declined payment without understanding why it failed can make recovery harder. Issuers track retry behavior, and excessive or poorly timed retries on the wrong decline type can trigger velocity flags that make future approvals less likely. A generic decline on a frozen account looks identical in your logs to one caused by a temporary network timeout, but the correct response is completely different. One requires customer action; the other just needs time. Treating them the same wastes retry attempts and risks card network rule violations.

Testing Your Generic Decline Recovery Strategy

The only reliable way to know whether your retry logic is working is to test it against a live control group. A vague payment error tells you nothing on its own, but your recovery rate over time tells you whether your context-gathering and retry sequencing are actually sound.

Start by splitting traffic so one cohort gets your current retry logic and another gets the adjusted approach you built after diagnosing the generic_decline error properly. Measure recovered dollars, not retry attempts. When the difference hits statistical significance, you have proof, not a hypothesis.

How Slicker Turns Generic Declines Into Contextual Recovery Opportunities

When a generic_decline error lands in your retry queue with no issuer detail attached, retrying blind is a coin flip. Slicker reads the full transaction signal (card type, issuer BIN, geography, subscriber tenure, and prior decline history) before deciding whether to retry, when, and at what amount. That context turns a vague payment error into a structured recovery decision instead of a guess.

Slicker's ensemble of AI models assigns each generic decline a confidence score. High-confidence soft declines get scheduled retries. Low-confidence signals get routed to a human review queue or a targeted dunning sequence, keeping your retry rate healthy without burning card-network goodwill.

Final Thoughts on Turning Vague Payment Errors Into Recovery Opportunities

A generic decline retry succeeds or fails based on signals the decline code itself never shows you. Geography, BIN data, subscriber history, and timing windows separate a soft timeout from a permanently blocked card, but most retry logic treats them identically. Let us walk you through what happens when you split-test context-driven retry logic against your current approach and measure the difference in recovered dollars, not retry attempts.

FAQ

Can I retry a generic_decline error without knowing what caused it?

You can, but you're guessing. A generic_decline or do_not_honor code can hide dozens of distinct causes (insufficient funds, velocity blocks, fraud flags, issuer outages), and each requires a different response. Retrying blind wastes attempts, risks triggering velocity flags, and can push recoverable failures into permanent blocks.

What's the difference between a retryable and non-retryable generic decline?

Retryable generic declines reflect temporary issuer-side conditions (network timeouts, momentary insufficient funds, processor overload) where timing and retry interval matter but the customer's intent to pay remains intact. Non-retryable generic declines signal something durable (blocked account, flagged card, hard risk threshold) where additional retries will not change the outcome and can actively worsen it by triggering velocity flags.

When should I wait 24 hours versus retrying immediately after a generic decline?

Wait 24 to 48 hours when the failure likely stems from temporary issuer congestion or a processing hiccup. Retry immediately only when you have strong signals (recent billing update, confirmed active card, no prior decline history) that separate this from a standing block. If the card shows multiple sequential generic declines within a short window, the issuer is actively blocking you and immediate retries will make recovery harder.

How do Merchant Advice Codes help with vague payment errors?

Merchant Advice Codes (MACs) turn a vague payment error into an actionable directive. MAC 03 tells you the customer must contact their bank before any retry; MAC 21 signals retrying is prohibited; MAC 01 means the account needs updating before payment can succeed. Ignoring these and retrying anyway triggers fraud flags, damages your merchant standing, or converts soft declines into hard ones.

Generic decline retry logic vs silent recovery?

Silent recovery handles generic technical failures without customer involvement, testing the transaction against issuer availability and timing patterns before escalating to dunning. For vague payment errors with no clear root cause, the retry itself is the diagnostic. Dunning is the right tool when customer action is required (expired card, stolen credential), but for generic declines it creates unnecessary friction and signals a problem the customer may not be able to fix.

Related Articles

How to Build a Retry Allowlist and Blocklist From Declines (July 2026)

I'll be frank: most retry logic is built on assumptions, not data. A retry allowlist tells your system when to try again; a payment retry blocklist tells it...

Country Retry Rules: India RBI, UK Direct Debit & Germany PayPal July 2026

Failed payment recovery looks very different depending on where your customer is. India's RBI retry rules limit attempts and require pre-debit notifications...

Smart Retry Timing: Payday & Bank Holidays (June 2026)

You set your retry schedule years ago. Three attempts, maybe four, spaced out by some number of days that felt reasonable at the time. The system fires retries...

Stop losing revenue to failed payments

Join leading subscription businesses using Slicker to recover failed payments automatically.

Get Started