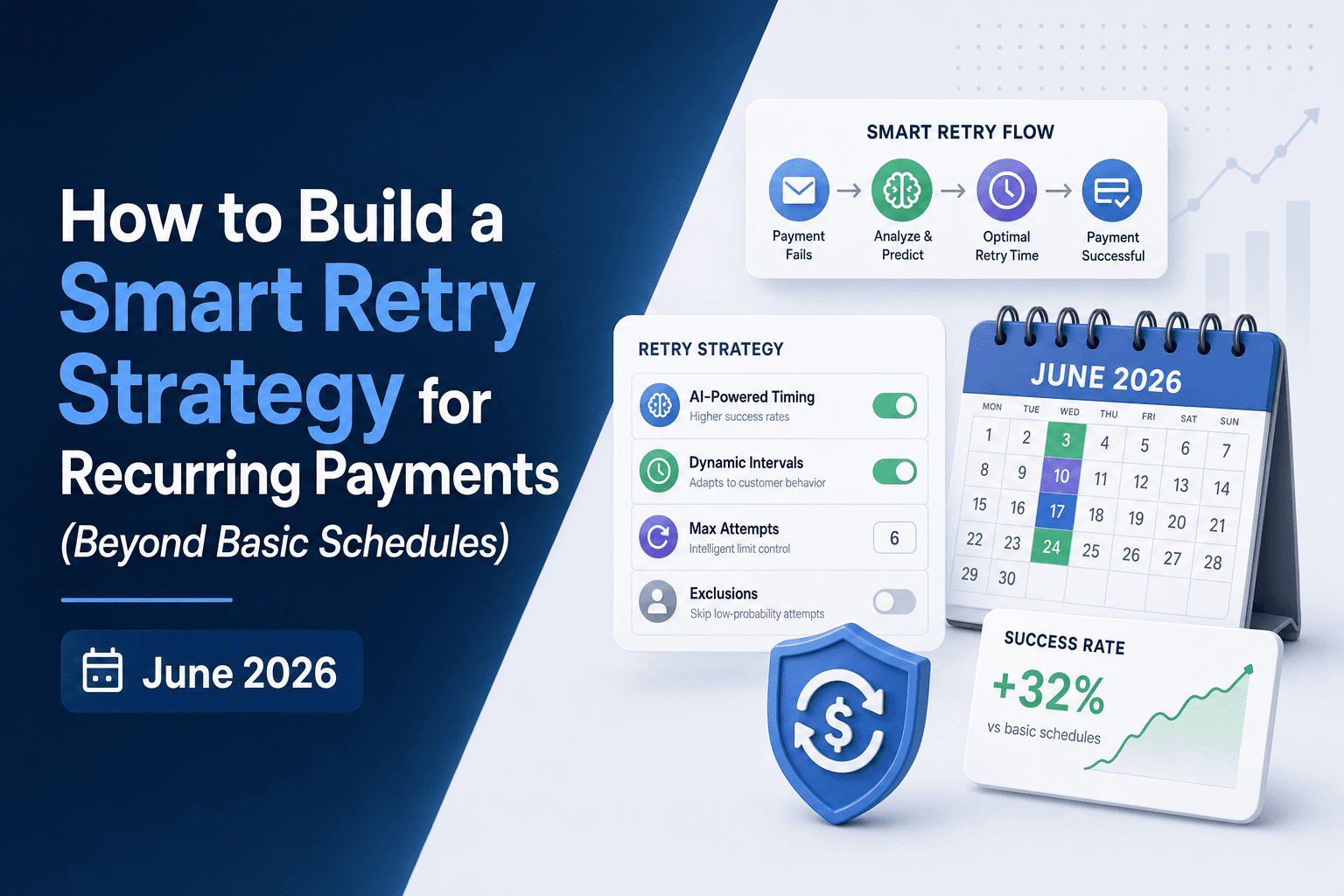

How to Build a Smart Retry Strategy for Recurring Payments (Beyond Basic Schedules) (June 2026)

Failed payments cost you more than the lost transaction. Every decline that sits in a generic retry queue is a subscriber you already earned, slipping into involuntary churn because your retry logic didn't read the decline code. Some failures are temporary and will clear in two days if you wait for the next payroll deposit. Others are permanent, and retrying them just burns your attempt budget and triggers card network penalties. A smart retry strategy treats each decline as a different recovery problem, routing based on issuer signals, payday timing, and card type, so the payments that can be saved actually get saved.

TLDR:

- Route failed payments by decline code first: soft declines (insufficient funds, network timeouts) recover with smart retry timing; hard declines (stolen cards, closed accounts) waste attempts and trigger card network penalties if retried.

- Read Merchant Advice Codes to decide retry strategy: MAC 02 means retry in 2-3 days, MAC 03 means stop immediately and escalate to dunning, MAC 21 signals customer-initiated stop payment requiring contact first.

- Align retry timing with regional payday cycles: US subscribers have funds on the 1st and 15th, Europe end-of-month, Russia the 5th and 20th. Retrying when accounts are funded lifts recovery rates 20-50%.

- Avoid card network penalty fees by staying inside retry limits: Visa and Mastercard cap excessive attempts on hard declines, with escalating penalties that compound into margin loss.

- Measure recovery with three metrics: recovery rate percentage (high-performing strategies hit 50%+), time to recovery in days (faster collection cuts involuntary churn), and net recovered dollars per month after costs.

Why Failed Recurring Payments Cost More Than You Think

Roughly 9% of recurring payments fail on the first attempt, and most of that revenue doesn't recover itself. Each failed charge triggers a chain reaction: customer frustration, support tickets, and involuntary churn (subscribers lost not because they cancelled, but because billing broke down). For payments that can't be recovered silently, smart dunning becomes the fallback (subscribers lost not because they cancelled, but because billing broke down). Unlike voluntary churn, these are customers who already said yes. The revenue was earned. A weak retry approach lets it walk out the door quietly, and the cumulative MRR impact compounds faster than most finance teams realize until they run the numbers.

Hard Declines vs. Soft Declines: Why Your Retry Logic Must Know the Difference

Retry logic that ignores decline type is one of the most common and costly mistakes in recurring billing. Soft declines signal temporary conditions like insufficient funds or network timeouts, where retrying after a short wait has a real chance of success. Hard declines signal permanent blocks: stolen cards, closed accounts, card numbers flagged for fraud. Retrying a hard decline wastes a transaction attempt, risks triggering issuer fraud flags, and can permanently damage your merchant standing with that issuer. Your retry logic needs to branch immediately on decline type, not treat every failed payment as the same problem waiting for the same fix.

How Merchant Advice Codes Tell You Exactly When (and When Not) to Retry

Merchant Advice Codes (MACs) are issuer-sent signals attached to decline responses that tell you precisely why a payment failed and what to do next. Ignoring them means retrying blindly; reading them means retrying intelligently.

There are two main code sets to know:

- Visa MACs (e.g., code 03) indicate the issuer will never approve this card again, making any retry a guaranteed failure that burns your retry budget and risks MID flagging.

- Code 21 signals a customer-initiated stop payment, where retrying without customer contact first violates network rules.

- Code 02 confirms the decline is temporary, and a retry in 2-3 days has a high probability of success.

A smart retry strategy routes each failed payment based on the MAC received, not a fixed calendar schedule.

MAC | Meaning | Retry Action |

|---|---|---|

02 | Try again later | Retry in 2-3 days |

03 | Do not retry | Stop; escalate to dunning |

21 | Stop payment order | Stop; require customer action |

Without MAC routing, every decline gets the same treatment regardless of recoverability, which leaves recoverable revenue on the table while wasting attempts on payments that will never clear.

Payday-Aligned Retry Timing: The Geography of When Customers Have Money

Retry timing isn't uniform across geographies, and ignoring that reality leaves recoverable revenue on the table. A subscriber in the US is most likely to have funds available around the 1st and 15th of the month, when direct deposits typically land. Retry windows should cluster around those dates.

The pattern varies by region:

- US and Canada: target retries within 1-3 days after the 1st and 15th, when payroll deposits are freshest

- Western Europe: salary cycles tend to run end-of-month, so retries in the final 2-3 business days of the month or the first 2 days of the next perform better

- Russia and Eastern Europe: monthly salary disbursements cluster tightly around the 5th and 20th, making those narrow windows worth targeting

- Australia: weekly and fortnightly pay cycles mean retry windows recur more frequently, but spacing attempts to align with Thursday or Friday deposit timing improves hit rates

A smart retry strategy bakes these windows into scheduling logic instead of firing at arbitrary intervals. The revenue impact is straightforward: retrying when a customer's account is statistically more likely to be funded recovers payments that a flat schedule would miss entirely.

Card Network Retry Limits: How to Stay Compliant and Avoid Penalty Fees

Card networks set strict retry limits after a decline, and exceeding them triggers penalty fees that quietly compound into serious costs. Visa and Mastercard both cap excessive retry attempts on hard declines, with penalty fees that escalate per transaction once you breach the threshold.

A smart retry strategy keeps you inside those limits by categorizing declines correctly before scheduling any follow-up attempt. Hard declines (stolen cards, closed accounts) should not be retried at all. Soft declines, where the issue is temporary, are where compliant retry logic actually applies.

Staying compliant protects margin. Every penalty fee is recovered revenue walking back out the door.

Building a Smart Retry Schedule: Static vs. Adaptive Timing Strategies

Retry timing isn't arbitrary. When you attempt a failed payment matters almost as much as whether you attempt it at all.

Static schedules retry at fixed intervals regardless of why a payment failed. Adaptive timing reads the decline reason and adjusts accordingly. A soft decline from a temporarily frozen card calls for a short wait; a decline tied to a monthly budget reset calls for payday-aligned retry timing.

Why Static Schedules Leave Money Behind

Fixed retry windows ignore two variables that drive recovery: the subscriber's cash flow cycle and the issuer's behavioral patterns. Retrying too soon on an insufficient-funds decline burns an attempt before the account replenishes. Retrying too late means a competitor charge has already claimed that balance.

What Adaptive Timing Actually Uses

A well-built adaptive schedule factors in:

- Decline code category (soft vs. hard, temporary vs. permanent) to decide whether a retry is worth attempting at all

- Day-of-week and pay-cycle data, since recovery rates on insufficient-funds declines spike on paydays

- Issuer-level patterns, because some banks batch authorization approvals at specific hours

- Prior retry history for that subscriber, so you're not repeating a window that already failed twice

The business outcome is straightforward: fewer wasted attempts, higher recovery on each retry window used, and less involuntary churn from accounts that would have recovered with better timing.

Account Updater Services: Preventing Failures Before They Happen

Account Updater services quietly solve a category of failures that retry logic alone cannot fix: expired or replaced card credentials. When a card is reissued, the old number becomes permanently invalid. No retry timing or intelligent scheduling recovers that payment. The card networks run Account Updater programs that push refreshed credentials to merchants before the next billing cycle, so the charge succeeds on the first attempt. Enrolling in these programs cuts a measurable slice of hard declines before they ever enter your retry queue.

Network Tokenization: How Updated Credentials Improve Retry Success Rates

When a card is reissued after theft or expiration, the underlying account often stays open. Network tokenization replaces the raw PAN with a network-managed token that updates automatically when credentials change, so a retry that would have hit a hard decline instead finds a valid credential already in place.

Visa and Mastercard both operate token services that push updated account information to participating merchants. For subscription businesses, the result is fewer preventable declines on renewals where the customer never intended to cancel.

A smart retry strategy should check for token-based credential updates before queuing a retry attempt, effectively converting what looked like a hard decline into a recoverable one.

Multi-Gateway Routing: Retrying Through Different Payment Processors

Not every decline is a card problem. Some failures are processor-specific: a gateway with weaker authorization rates for certain card types, or a regional issuer that routes poorly through one acquirer but approves readily through another. The same card, the same cardholder, a different outcome depending on which processor touches the transaction.

Multi-gateway routing treats your processor relationships as recovery diversification. A retry that fails on Gateway A may clear on Gateway B because each processor carries different approval logic with issuing banks. Regional and international card portfolios benefit most, where approval rate variance across processors is widest. Adding routing intelligence to your retry strategy expands the number of viable recovery paths per failed payment instead of exhausting attempts through a single point of failure.

Measuring What Matters: Recovery Rate, Time to Recovery, and Revenue Impact

Three metrics tell you whether your retry strategy is actually working.

Recovery rate is the starting point: what percentage of initially failed payments do you eventually collect? Industry data puts average recovery rates around 20-30%, but high-performing strategies can push that to 50% or beyond.

Time to recovery tracks how quickly you collect after the initial decline. Faster recovery reduces involuntary churn risk and shortens your days sales outstanding (DSO).

Revenue impact ties it all together: recovered dollars per month, net of any recovery costs. That's the number your CFO cares about.

How Slicker Builds Retry Intelligence Beyond Basic Schedules

Slicker's retry logic starts where basic schedules stop. Instead of firing retries on a fixed cadence, it runs an ensemble of AI models that weighs issuer behavior, card type, decline code, geography, and historical transaction patterns before deciding whether to retry, and when.

The result is hyper-personalized retry timing at the individual transaction level. A soft decline on a debit card in the UK gets a different retry window than an insufficient funds code on a prepaid card in the US, because the underlying recovery probability is genuinely different.

Every decision is validated through clinical-grade AABB testing on your own traffic, so recovered revenue is measured against a control group with statistical significance before you commit.

Final Thoughts on What Makes Retry Logic Intelligent

Your retry logic is either working with the information your payment processor sends, or it's guessing. Smart retry timing recovers revenue that fixed schedules miss, and the proof lives in your own data. Reach out if you want to measure what an intelligent retry approach would recover from your current decline volume, no trust required.

FAQ

What's the best way to retry failed payments automatically?

Read the decline code first, then route the retry based on whether it's soft (temporary) or hard (permanent). Soft declines should retry on a schedule tuned to payday timing and issuer behavior. Hard declines should skip retries entirely and escalate to dunning or require customer action.

How do smart retries affect customer churn and revenue?

Smart retries cut involuntary churn by recovering payments from subscribers who never intended to cancel. Recovery rate uplifts of 20-50% translate directly into retained MRR, shortened DSO, and fewer support tickets from billing failures that customers never knew about.

What is the best decline retry strategy?

The best strategy routes each decline based on Merchant Advice Codes, geography-specific payday windows, card type, and issuer patterns. MAC 02 declines retry in 2-3 days; MAC 03 stops immediately. Timing aligns with the 1st and 15th in the US, end-of-month in Europe, and the 5th and 20th in Russia.

Should I retry a hard decline from a stolen card?

No. Hard declines signal permanent blocks like stolen cards, closed accounts, or fraud flags. Retrying these burns your retry budget, risks triggering issuer fraud flags, and can damage your merchant standing with that issuer.

What recovery rate can subscription businesses expect from structured retry logic?

Industry averages sit around 20-30% recovery on initially failed payments. High-performing retry strategies that route on decline codes, payday timing, and issuer behavior push recovery rates to 50% or higher, measured on the business's own transaction data.

Related Articles

How AI Rewrites Dunning Logic: Playbooks & Testing (July 2026)

If your dunning window is whatever your billing tool shipped with, and your retry timing is day 3, day 7, day 14, you're leaving recoverable revenue on the...

Smart Dunning & Personalized Recovery Emails Explained: July 2026

Your subscribers aren't all failing to pay for the same reason, so your dunning emails probably shouldn't all say the same thing. A temporary overdraft, an...

Why Your Dunning Emails Need Your Domain, Not the Vendor's (July 2026)

Most failed payments recover silently. Automated retries handle the majority of soft declines without any customer contact. But when a payment failure...

Stop losing revenue to failed payments

Join leading subscription businesses using Slicker to recover failed payments automatically.

Get Started