What Is a Good Involuntary Churn Rate? SaaS Benchmarks and How to Improve Yours (June 2026)

Most SaaS companies lose 1 to 3% of MRR every month to involuntary churn, and half of that is preventable with better retry logic. These aren't customers who decided to leave. Their payment failed because a card expired, an issuer flagged fraud, or funds were temporarily low. Voluntary churn meaning is different: that's an active cancellation tied to product dissatisfaction or changing needs. Your involuntary churn rate in 2026 works the same way it did in 2022. The forced churn meaning hasn't shifted either: subscribers lose access not because they chose to cancel, but because your billing system couldn't recover a soft decline or update an expired card before the subscription lapsed. The revenue impact compounds fast, because every involuntarily churned customer represents acquisition cost you'll never recover and lifetime value that just disappeared without a retention signal. Getting this number under control starts with measuring it separately from voluntary churn and applying smarter recovery strategies to the transactions that are actually retriable.

TLDR:

- Involuntary churn from failed payments accounts for 20 to 40% of total SaaS churn.

- A good involuntary churn rate sits below 1% of MRR monthly; B2B SaaS averages 0.3 to 1.0%.

- Intelligent retry logic timed to issuer behavior outperforms fixed schedules by 5+ points.

- Personalized dunning recovers 30 to 50% of failed payments when tailored to decline reason.

- Slicker uses AI models to decide retry timing per transaction, proving lift via AABB testing.

What Is Involuntary Churn Rate and Why It Matters

Involuntary churn rate measures the percentage of subscribers lost each period due to failed payments instead of a deliberate decision to cancel. A customer's card gets declined, the payment never processes, and the subscription lapses without anyone choosing to leave.

This is worth separating from voluntary churn, where a customer actively cancels. Involuntary churn is a billing problem, not a product problem, which means it responds to very different fixes.

The revenue impact is real: industry data suggests failed payments affect roughly 9% of all transactions, making involuntary churn one of the largest controllable sources of MRR loss for subscription businesses.

How to Calculate Involuntary Churn Rate

Divide your involuntary churn rate by taking the number of customers lost due to payment failures in a given period, then dividing by your total customers at the start of that period, and multiplying by 100.

For example, if you started the month with 2,000 subscribers and 40 left due to failed payments, your involuntary churn rate is 2%.

What to Track Alongside the Rate

The raw percentage alone won't tell you where revenue is leaking. Pair it with:

- Revenue lost per failed payment event, so you can quantify the dollar impact beyond just the subscriber count.

- Recovery rate after retry attempts, which shows how much involuntary churn you're preventing before it becomes permanent.

- Failure reason breakdown by decline code, since soft declines (retriable) and hard declines (non-retriable) require entirely different responses.

Tracking all three together reveals whether your recovery logic is working or quietly leaving money on the table.

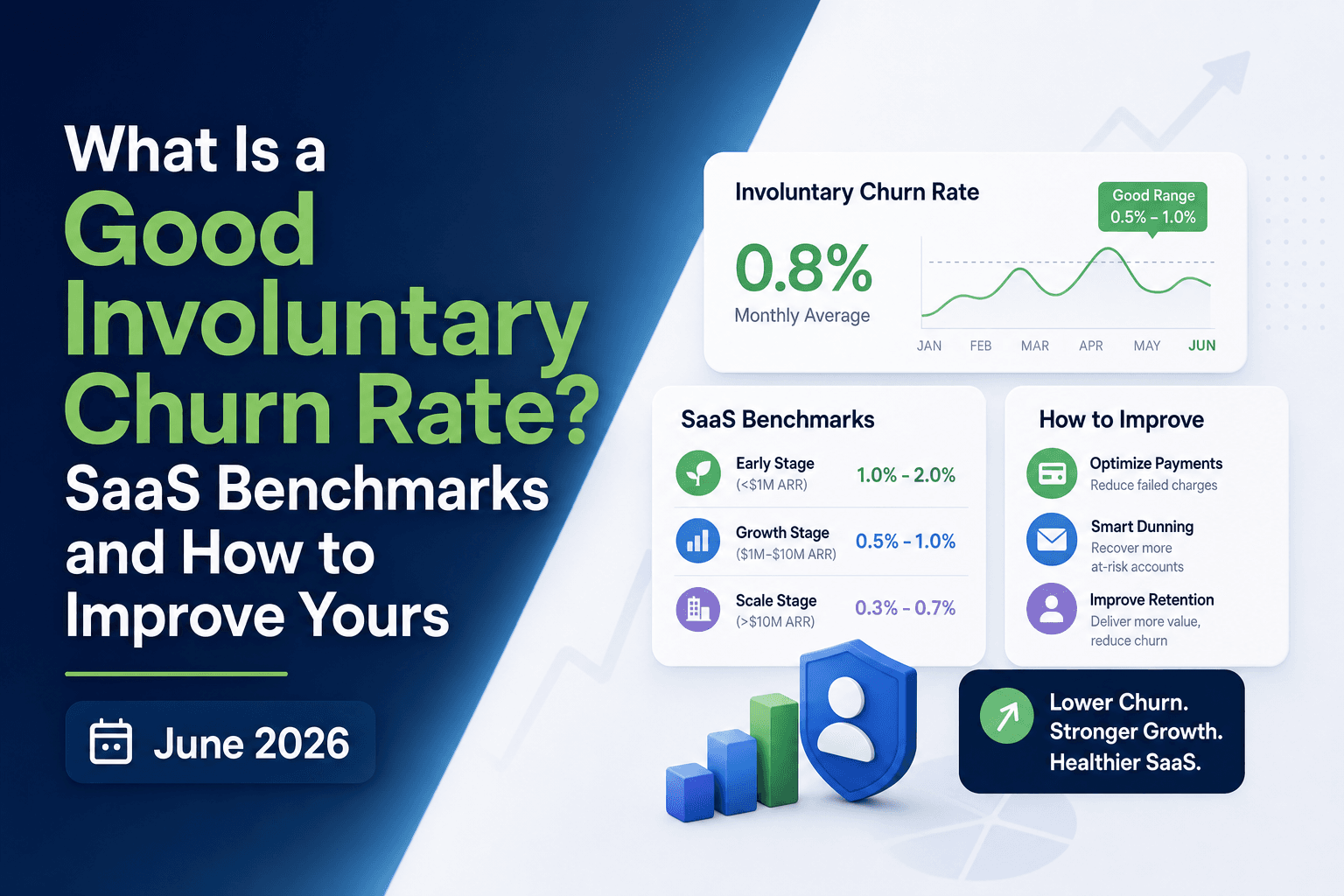

Involuntary Churn Rate Benchmarks for SaaS in 2026

Across SaaS companies, failed payments typically account for 20 to 40% of total churn. Most benchmarks put a healthy involuntary churn rate below 1% of MRR per month, though rates vary by business model, price point, and customer segment.

What the Data Shows

Industry data points to a few consistent patterns worth tracking against:

- Companies processing higher volumes of recurring transactions tend to see involuntary churn rates between 1% and 3% of MRR monthly, with the top quartile holding below 0.5%.

- Consumer-facing SaaS products see higher involuntary churn than B2B products, largely due to prepaid and debit card usage, which carry higher decline rates.

- Roughly 15% of all recurring payments are declined on the first attempt, according to industry data, making retry logic a direct lever on your involuntary churn rate.

Segment | Typical Involuntary Churn Rate |

|---|---|

B2B SaaS | 0.3% to 1.0% of MRR/month |

Consumer SaaS | 1.0% to 3.0% of MRR/month |

Top-performing (any segment) | Below 0.5% of MRR/month |

If your involuntary churn rate sits above 1% of MRR monthly, there is measurable revenue walking out the door that smarter retry logic and dunning sequencing could recover before it becomes permanent loss.

What Causes Involuntary Churn

Involuntary churn happens when a customer's subscription lapses not because they chose to leave, but because their payment failed. The causes tend to fall into a few recurring categories.

- Expired or outdated card details are the most common trigger. Cards expire, get replaced after fraud, or are reissued with new numbers, and the billing system never receives the update.

- Soft declines occur when an issuer temporarily blocks a charge due to insufficient funds, daily spending limits, or fraud flags. These are often recoverable with a retry at the right moment.

- Hard declines happen when a card is permanently blocked, stolen, or reported lost. These require the customer to act directly.

- Processing errors from banks or payment networks can reject valid transactions for technical reasons unrelated to the customer's account standing.

Because none of these involve a customer's intent to cancel, they represent revenue you've already earned. The payment infrastructure simply failed to collect it. That distinction matters: voluntary churn requires a product or experience fix, while involuntary churn requires a payments fix.

The Revenue Impact of Involuntary Churn

Involuntary churn quietly drains revenue that your business has already earned. Unlike voluntary cancellations, these are customers who wanted to stay but lost access because a payment failed. The financial damage compounds fast.

Industry data suggests that failed payments account for roughly 20 to 40% of total churn at most SaaS companies. On a $1M MRR business, even a 1% involuntary churn rate represents $10,000 in lost monthly recurring revenue, and that figure multiplies when you factor in the lifetime value of each cancelled subscription.

The cost goes beyond the immediate lost MRR. Consider what each involuntarily churned customer actually represents:

- Acquisition cost already spent to win them, now unrecoverable since they leave without any cancellation signal that would trigger a save flow.

- A gap in your retention data, because payment failures blend into dashboards the same way voluntary cancellations do, which makes the problem easy to underestimate.

- Compounding ARR erosion, since each month of unaddressed involuntary churn stacks on the previous month's losses.

Getting this number under control starts with measuring it accurately and separately from voluntary churn.

Smart Payment Retry Strategies to Reduce Involuntary Churn

Retry logic is the first line of defense against involuntary churn. When a payment fails with a soft decline, the transaction can often succeed on a second attempt if timed and structured correctly.

Static vs. Intelligent Retry Schedules

Basic retry schedules attempt payment again on fixed intervals, say day 3, day 7, and day 14. The problem is that a card declined for insufficient funds on a Tuesday behaves differently than one flagged for a suspected fraud hold on a Friday before a holiday.

Intelligent retry systems factor in:

- Issuer behavior patterns, so retries land when approval probability is statistically higher based on historical data for that bank.

- Decline code context, since a "do not honor" code warrants a different retry cadence than a temporary hold.

- Day-of-week and time-of-day signals, because consumer account balances and issuer processing queues follow predictable rhythms.

Why Timing Matters More Than Volume

Hammering a declined card with rapid retries does not improve recovery. It raises the risk of hard decline escalation and can trigger fraud flags at the issuer level. well-timed retries outperform poorly-timed ones, keeping your merchant standing intact while recovering revenue more cleanly.

The measurable difference between static and intelligent retry logic compounds at scale: across thousands of subscribers, even a 5-percentage-point lift in retry success moves real MRR off the lost-revenue column.

Dunning Management Best Practices

Effective dunning strategies can recover 30% to 50% of failed payments, but generic "please update your card" messaging leaves most of that potential unrealized. The failure reason determines everything about how you communicate.

An expired card needs a different call-to-action than a stolen one. Insufficient funds calls for timing sensitivity; a fraud block requires the subscriber to contact their bank directly. Personalized multi-channel notifications combining email with SMS or in-app alerts reduce involuntary churn by up to 34% compared to single-channel email flows, according to industry data.

A few principles worth following:

- Send the first message within 24 hours of the failure, before access lapses and urgency fades.

- Tailor each email to the specific decline reason so subscribers know exactly what action is required.

- Only reach out when customer action is genuinely needed. Silent retries should always come first; outreach is the fallback.

- Frame every message around what the subscriber stands to lose, not around the mechanics of the payment failure itself.

Account Updater Services and Card Refresh Automation

Most recovery strategies are reactive. Account updater services work earlier in the process, eliminating the most predictable failure category before a charge ever gets declined.

Visa Account Updater and Mastercard Automatic Billing Updater push refreshed credentials to merchants automatically when a card expires or gets reissued. Updated details arrive ahead of the next billing attempt, so the payment processes cleanly without falling into a retry queue or triggering a dunning sequence the subscriber never needed to receive.

Industry data puts expired or reissued cards behind 10 to 15% of all recurring payment failures. Catching those proactively means fewer retries, less dunning outreach, and a structurally lower involuntary churn rate before any recovery logic even comes into play.

How Slicker Uses AI to Recover Failed Payments and Reduce Involuntary Churn

Slicker sits directly in the recovery layer between your billing system and your payment processor, working silently before a customer ever knows a payment failed.

At its core, Slicker runs an ensemble of AI models that analyzes each failed transaction across variables like card type, issuer, decline code, geography, and customer payment history. Instead of applying a fixed retry schedule, the AI decides whether to retry, when, and at what cadence based on what is most likely to recover that specific payment.

A few things set Slicker apart:

- Smart retries happen automatically, with zero engineering lift required. Setup takes roughly five minutes and requires no changes to your existing billing infrastructure.

- Every customer gets a recovery strategy tuned to their own transaction data, not a generic rule set borrowed from someone else's payment mix.

- When silent recovery is not enough, such as with expired or stolen cards, Slicker triggers hyper-personalized dunning emails sent from your own domain and brand, anchored to the specific failure reason instead of a generic "update your payment method" prompt.

- Performance is proven through clinical-grade AABB testing. Slicker splits your traffic, measures dollars recovered with statistical significance, and reports the results on your own data before you commit.

That last point matters most for a skeptical finance leader. You are not being asked to trust a vendor's aggregate recovery claims. You see the lift on your own customer base, with a p-value attached.

Frequently Asked Questions

What's the difference between involuntary churn and voluntary churn?

Involuntary churn results from failed payments, while voluntary churn occurs when a customer actively cancels. Involuntary churn is a billing infrastructure problem affecting customers who intended to stay, which means it requires payment-recovery fixes instead of product or experience improvements.

Can I reduce involuntary churn without adding engineering resources?

Yes. Payment recovery platforms like Slicker run on top of your existing billing infrastructure with no-code integration that takes roughly five minutes to complete. Smart retry logic and automated dunning operate without requiring any engineering build or ongoing maintenance from your team.

How much involuntary churn is normal for a SaaS business?

B2B SaaS companies typically see involuntary churn rates between 0.3% and 1.0% of MRR per month, while consumer-facing SaaS sees 1.0% to 3.0%. Top-performing companies in any segment hold involuntary churn below 0.5% of MRR monthly. If your rate sits above 1%, there is measurable revenue walking out the door that smarter retry logic could recover.

Should I send dunning emails immediately after a payment fails?

Not always. Silent automated retries should come first, since many soft declines succeed on a second attempt without requiring customer action. Send dunning emails only when the failure reason directly requires the customer to act, such as with expired or stolen cards. The first dunning message should go out within 24 hours if customer action is needed.

What's the difference between a soft decline and a hard decline?

A soft decline is a temporary block from the issuer (insufficient funds, a spending limit hit, or a fraud flag) and is often recoverable with a well-timed retry. A hard decline means the card is permanently blocked, stolen, or reported lost, and requires the customer to take direct action. Treating both the same way wastes retries on unrecoverable failures and misses recovery opportunities on retriable ones.

How does intelligent retry logic differ from building retries in-house?

Intelligent retry systems analyze issuer behavior patterns, decline codes, and time-of-day signals to determine the optimal retry moment for each specific transaction. Generic fixed-interval schedules miss the context that drives recovery probability. Building this capability in-house requires years of training data across diverse businesses and continuous model refinement, which is why most finance teams choose specialized recovery platforms that prove incremental lift through statistical testing on their own transaction data.

Final Thoughts on Involuntary Churn Recovery

Most involuntary churn never makes it into your retention dashboards, which means you're probably underestimating how much revenue walks out the door each month because a card expired or got flagged for fraud. The good news is that these customers didn't choose to leave. They're recoverable, and prove it on your own data. Recovery happens silently most of the time: your subscribers keep their access, you keep the MRR, and nobody has to think about a declined payment that never should have ended the subscription in the first place.

Related Articles

Merchant Advice Codes: Retry Guide (June 2026)

A payment declines, and your billing system sees both a response code and a Mastercard advice code in the authorization message. The response code tells you...

Soft Decline Retry Playbook: When to Retry, When to Stop, and What to Change (June 2026)

You retry soft declines because you know they're recoverable, but if your retry timing is the same for every decline reason, you're burning through attempts...

Smart Automatic Payment Retry Best Practices for Subscription Businesses in June 2026

Most subscription businesses lose 15% of their recurring revenue to payment declines, and the majority of that is recoverable if you retry at the right time...

Stop losing revenue to failed payments

Join leading subscription businesses using Slicker to recover failed payments automatically.

Get Started