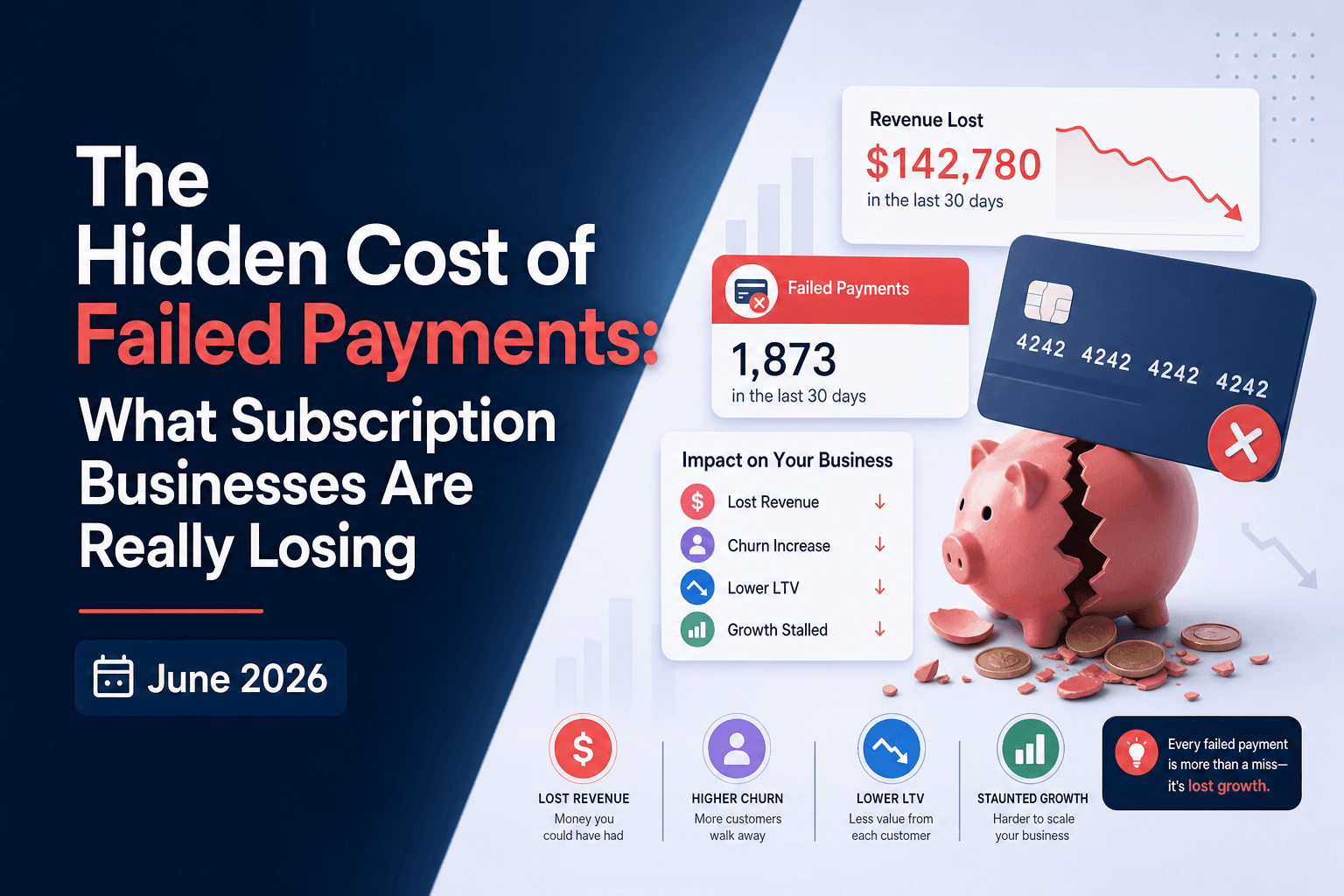

The Hidden Cost of Failed Payments: What Subscription Businesses Are Really Losing (June 2026)

Failed payments cost subscription businesses far more than the missed transaction. The visible hit is immediate MRR loss, but that's only the first layer. When a recoverable subscriber churns because their payment failed and no one caught it in time, you lose every future renewal plus the customer acquisition cost you already spent. Then there's the execution cost: support tickets, manual retry attempts, and accounting overhead that quietly erode margin on every recovery. Industry data shows roughly 9% of all recurring payments fail, and at scale, the compounding cost of failed payments across these three layers can dwarf what shows up on a standard churn report. Here's what finance teams miss when they only track the decline itself.

TLDR:

- Roughly 9% of subscription payments fail, costing you the missed transaction plus lifetime value and CAC (often 5 to 7x monthly price).

- Involuntary churn strips revenue from customers who still want your product; a company processing 50,000 renewals monthly sees 4,500 failures before anyone cancels.

- Support costs ($5 to $35 per contact) and manual recovery workflows quietly erode margin at scale.

- Smart retry logic schedules attempts based on decline code, card type, and issuer behavior instead of fixed intervals, lifting recovery rates by 20 to 50%.

- Slicker uses AI models to retry failed payments on autopilot and proves results through AABB testing on your own data before you pay.

The Financial Impact of Failed Payments on Subscription Businesses

Every failed payment is a revenue leak, but the full cost runs deeper than the missed transaction. For subscription businesses, the financial damage compounds across three distinct layers.

The most visible hit is immediate revenue loss. Industry data shows roughly 9% of all subscription payments fail, and each one chips away at monthly recurring revenue (MRR) before recovery even begins. Research shows roughly half of subscription churn stems from failed card payments, with most of those failures unrelated to customer intent. But the harder losses are what follow.

When a payment fails and a subscriber churns as a result, you lose that month's revenue plus every future renewal. Given that SaaS CAC typically ranges $400 to $900, and often runs 5 to 7x the monthly subscription price, that loss is substantial.

The third layer is execution drag. Recovery workflows, support tickets, and manual retry attempts consume real headcount. These costs rarely show up on a failed payments report, but they quietly erode margin on every recovery you do make.

Taken together, the true cost of failed payments is a multiple of the declined transaction itself, and most finance teams are only measuring the tip of it.

Involuntary Churn: The Silent Revenue Killer

When a subscriber's payment fails and they lose access without ever intending to cancel, that's involuntary churn. Unlike voluntary cancellation, it's a purely mechanical failure, one that strips revenue from customers who still want your product.

The scale of the problem is substantial. Roughly 9% of recurring payments fail on the first attempt, and for high-volume subscription businesses, those failed transactions accumulate fast. A company processing 50,000 renewals monthly could see 4,500 payments fail before a single customer decides to leave.

What makes involuntary churn particularly costly is how quietly it compounds. Each failed payment represents a recoverable customer, but without the right recovery logic in place, those customers silently lapse. The revenue lost goes beyond one month's subscription to the full remaining lifetime value of a subscriber who never got the chance to stay.

For finance leaders monitoring subscription metrics, involuntary churn creates a persistent, underreported drag on growth that rarely surfaces in standard churn dashboards the way voluntary cancellations do.

Execution Costs Beyond Lost Revenue

Failed payments don't just cost you the lost transaction. Each one generates downstream work that eats into margins quietly and consistently.

When a payment fails, your support team absorbs the fallout. Customers call in confused, dispute charges, or request manual billing corrections. These interactions cost real agent time, and at scale, they compound fast. Each contact carries a measurable cost in agent time and tooling, meaning a high failure rate can translate to significant support overhead monthly.

There's also the accounting burden. Finance teams must match and settle failed transactions, reprocess invoices, and track down accounts in arrears. For businesses processing thousands of subscriptions, that's not a rounding error in headcount or tooling costs.

Then consider customer acquisition cost (CAC). When involuntary churn goes unrecovered, you lose a subscriber you already paid to acquire. Replacing that subscriber means spending CAC again, often $100 to $500 or more in competitive categories, to recover revenue you had already earned.

The execution drag compounds every month failed payments go unaddressed, making recovery speed as financially relevant as recovery rate itself.

Why Recurring Payments Fail: Root Causes and Patterns

Recurring payment failures fall into two broad categories: soft declines and hard declines. Soft declines are temporary, meaning the card is valid but the transaction was rejected for reasons like insufficient funds, issuer timeouts, or suspected fraud flags. Hard declines signal a permanent issue, such as a cancelled or stolen card, where retrying is futile.

15% of recurring payments are declined on the first attempt. Of those, a meaningful share are recoverable through smarter retry logic, yet most billing systems treat every failure the same way and retry on a fixed schedule regardless of the decline reason.

Failure Type | Decline Category | Root Cause | Recovery Approach |

|---|---|---|---|

Insufficient funds at billing date | Soft decline | Timing problem where funds are temporarily unavailable | Retry with intelligent scheduling based on customer payment patterns |

Expired card | Hard decline | Customer forgot to update card details before renewal date | Send dunning communication requesting updated payment method |

Issuer fraud flag | Soft decline | Unusual billing patterns, geography, or transaction velocity triggered security alert | Retry after brief delay or route through alternate processor |

Network timeout | Soft decline | Processor errors unrelated to customer account health | Immediate retry as issue has no connection to customer ability to pay |

Stolen or cancelled card | Hard decline | Card reported as compromised or account closed by issuer | Customer communication required to obtain new valid payment method |

Several patterns drive the bulk of failures:

- Insufficient funds at the billing date, which is often a timing problem instead of a true inability to pay

- Expired cards that customers simply forgot to update before the renewal date

- Issuer-side fraud flags triggered by unusual billing patterns, geography, or transaction velocity

- Network timeouts and processor errors that have nothing to do with the customer's account health

The failure type matters because the right recovery path depends entirely on the root cause. A timeout calls for a retry; a stolen card calls for a customer communication. Conflating these failure modes is where most subscription businesses quietly lose recoverable revenue.

How Merchant Advice Codes Impact Recovery Strategy

When a payment fails, the card network often sends back more than a decline code. Merchant Advice Codes (MACs) are explicit instructions from issuers telling you whether to retry, how long to wait, or when to stop attempting recovery altogether. Mastercard publishes over a dozen of these codes, ranging from "retry in one hour" to "do not retry under any circumstances."

Ignoring them carries a direct cost. Mastercard charges $0.10 per retry attempt when a merchant proceeds despite a "do not retry" instruction, and Visa applies equivalent penalties for excessive retries on certain decline categories.

Following MACs rigidly creates its own problem. A code prescribing a 10-day wait is worthless if your dunning window closes in five. The gap between network guidance and actual recovery opportunity is where most static retry systems quietly lose revenue.

Smart Retry Logic and Recovery Strategies

When a payment fails, the window to recover it without losing the customer is narrow. Smart retry logic works by analyzing signals like decline code, card type, issuer behavior, and historical timing patterns to schedule each retry at the moment it has the highest probability of success. Retrying too soon hits the same decline; waiting too long lets the subscriber churn or notice the disruption.

Smart retry logic works by analyzing signals like decline code, card type, issuer behavior, and historical timing patterns to schedule each retry at the moment it has the highest probability of success. Industry data suggests optimized retry timing alone can lift recovery rates meaningfully compared to fixed-interval approaches.

What separates recovery strategies that work

The gap between basic and advanced recovery comes down to a few concrete differences:

- Retry scheduling based on decline code, not a fixed clock. A soft decline from insufficient funds on a prepaid card warrants a different timing window than a network timeout.

- Subscriber-level pattern recognition, so retry logic accounts for individual payment histories instead of applying one schedule to all accounts.

- Escalation to customer communication only when the error genuinely requires action, like an expired or stolen card, keeping friction low for recoverable failures.

Each layer compounds. Businesses that treat retry logic as a set-and-forget rule typically recover a fraction of what a continuously optimized approach captures, leaving real MRR on the table every billing cycle.

How Slicker Recovers Failed Payments for Subscription Businesses

Slicker sits on top of your existing billing infrastructure with no engineering work required. Setup takes roughly five minutes, and from there, recovery runs on autopilot.

The core engine is an ensemble of AI models that analyzes each failed payment individually, weighing variables like card type, issuer behavior, geography, decline code, and historical retry patterns to decide whether to retry, when, and at what amount. Instead of running payments through a fixed schedule, the system adapts to what actually works for each subscriber.

When a failed payment genuinely requires customer action, such as a stolen or expired card, Slicker sends hyper-personalized dunning communications from your own domain and brand, framed around the value the subscriber would lose, not the transaction itself.

Every decision is measured through clinical-grade AABB testing, splitting traffic to prove recovery lift against a control group on your own data before you commit to anything. If Slicker does not beat your existing results at p < 0.05, you do not pay.

Final Thoughts on the Cost of Failed Payments

The true cost of a failed payment is a multiple of the declined transaction: lost MRR, wasted CAC when subscribers churn involuntarily, and the execution cost of manual recovery attempts. Most subscription businesses measure only the surface loss and treat every decline with the same fixed retry schedule. Recovering what's actually recoverable requires matching retry timing to the decline reason, routing customer communication only when the error genuinely requires action, and proving the lift with your own data. If you're ready to see what intelligent recovery looks like on your subscriber base, run an AABB test on your data.

FAQ

What's the best way to retry failed payments automatically?

Smart retry logic analyzes decline codes, card types, issuer behavior, and timing patterns to schedule each attempt when it has the highest probability of success. Standard billing platforms apply fixed retry schedules to every failure type, treating a network timeout the same as insufficient funds, which leaves recoverable revenue on the table every billing cycle.

How does AI improve failed payment recovery rates?

Slicker's AI weighs variables like card type, issuer behavior, geography, decline code, and historical retry patterns to decide whether to retry, when, and at what amount for each failed payment individually. Industry data shows this approach lifts recovery rates by 20 to 50% compared to fixed-interval retry schedules that ignore the reason a payment failed.

Can you build payment recovery without engineering resources?

Yes. Slicker integrates with existing billing platforms like Stripe, Chargebee, Recurly, and Zuora in roughly five minutes with no code required, and recovery runs on autopilot from there. Your engineers stay focused on your product while recovery logic operates through your existing payment infrastructure.

What data is needed to start reducing failed payments with AI?

AI-powered recovery requires access to your billing system's failed payment events, decline codes, card metadata, and historical retry outcomes. Most modern billing platforms (Stripe, Chargebee, Recurly, Zuora) expose this data through standard APIs, making setup fast with no custom integration work required.

When should dunning emails go out vs automated retries?

Automated retries are the primary recovery method for failures that do not require customer action, such as network timeouts or temporary insufficient funds. Dunning emails should only trigger when the decline genuinely requires the customer to act, like an expired or stolen card, keeping friction low while maintaining recovery speed.

Related Articles

How AI Rewrites Dunning Logic: Playbooks & Testing (July 2026)

If your dunning window is whatever your billing tool shipped with, and your retry timing is day 3, day 7, day 14, you're leaving recoverable revenue on the...

Smart Dunning & Personalized Recovery Emails Explained: July 2026

Your subscribers aren't all failing to pay for the same reason, so your dunning emails probably shouldn't all say the same thing. A temporary overdraft, an...

Why Your Dunning Emails Need Your Domain, Not the Vendor's (July 2026)

Most failed payments recover silently. Automated retries handle the majority of soft declines without any customer contact. But when a payment failure...

Stop losing revenue to failed payments

Join leading subscription businesses using Slicker to recover failed payments automatically.

Get Started