How Payday Patterns and Bank Holidays Affect Subscription Payment Success Rates (May 2026)

Your recurring charges are failing because they're landing before your subscribers have money in their accounts. Subscription payment timing relative to payday windows, bank holiday payment processing delays, and end-of-month billing clusters drives payment success rates up or down by double digits every single month.

Insufficient funds declines spike predictably around the first, fifteenth, and last day of the month when rent, utilities, and payroll all collide in the same 72-hour window. Most of those failures are recoverable without any dunning if your retry logic accounts for real-world cash flow. When you align payday payment recovery attempts with actual payroll cycles and route around bank holidays, recurring billing optimization stops being guesswork and starts capturing the MRR you already earned.

TLDR:

- Payment success rates swing 10 to 15 percentage points based on when you charge relative to payday windows: the difference between capturing MRR you already earned and writing it off as involuntary churn.

- 15% of recurring payments fail on first attempt, with insufficient funds driving most soft declines because the charge hit before your subscriber's paycheck cleared, not because they canceled.

- Retry 3 to 5 days after the original decline, timed to land just after common paydays (1st, 15th, last business day), and you recover those payments without any customer contact or dunning sequences.

- Bank holidays delay ACH settlement by 2 to 3 business days; retry logic that ignores this calendar reality triggers duplicate charges and burns subscriber trust with false-alarm dunning.

- Slicker's Artificial Payments Intelligence ingests payday calendars, bank holiday schedules, and issuer behavior patterns to time each retry attempt when funds are most likely in the account, proven on your own data in an AABB test before you commit.

Why Subscription Payment Timing Matters for Revenue Recovery

Payment timing is one of the most overlooked variables in subscription billing. When a recurring charge lands relative to a subscriber's payday or a regional bank holiday directly affects whether that transaction clears on the first attempt.

Industry data suggests payment success rates can vary by as much as 10 to 15 percentage points depending on the day of the month a charge is attempted. For a subscription business processing thousands of recurring transactions, that gap translates directly into involuntary churn and lost MRR you had already earned.

The Payment Failure Reality: How Common Are Timing-Related Declines

Industry data shows roughly 15 percent of recurring payments are declined on any given attempt, with insufficient funds consistently leading as the primary cause of soft declines across subscription businesses.

For a business running 100,000 active subscribers, that translates to 15,000 failed attempts per billing cycle. Most of those customers are not canceling intentionally. The charge simply landed before their paycheck cleared.

Decline rates shift with billing cycle position, and timing-related failures are recoverable if you know when to retry.

How Payday Patterns Influence Account Balance Availability

Most subscription billing systems fire charges on a fixed schedule without any awareness of when subscribers actually get paid. The gap between charge date and payday is one of the quieter drivers of soft declines, with insufficient funds accounting for a large share of failed recurring payments across consumer-facing subscriptions.

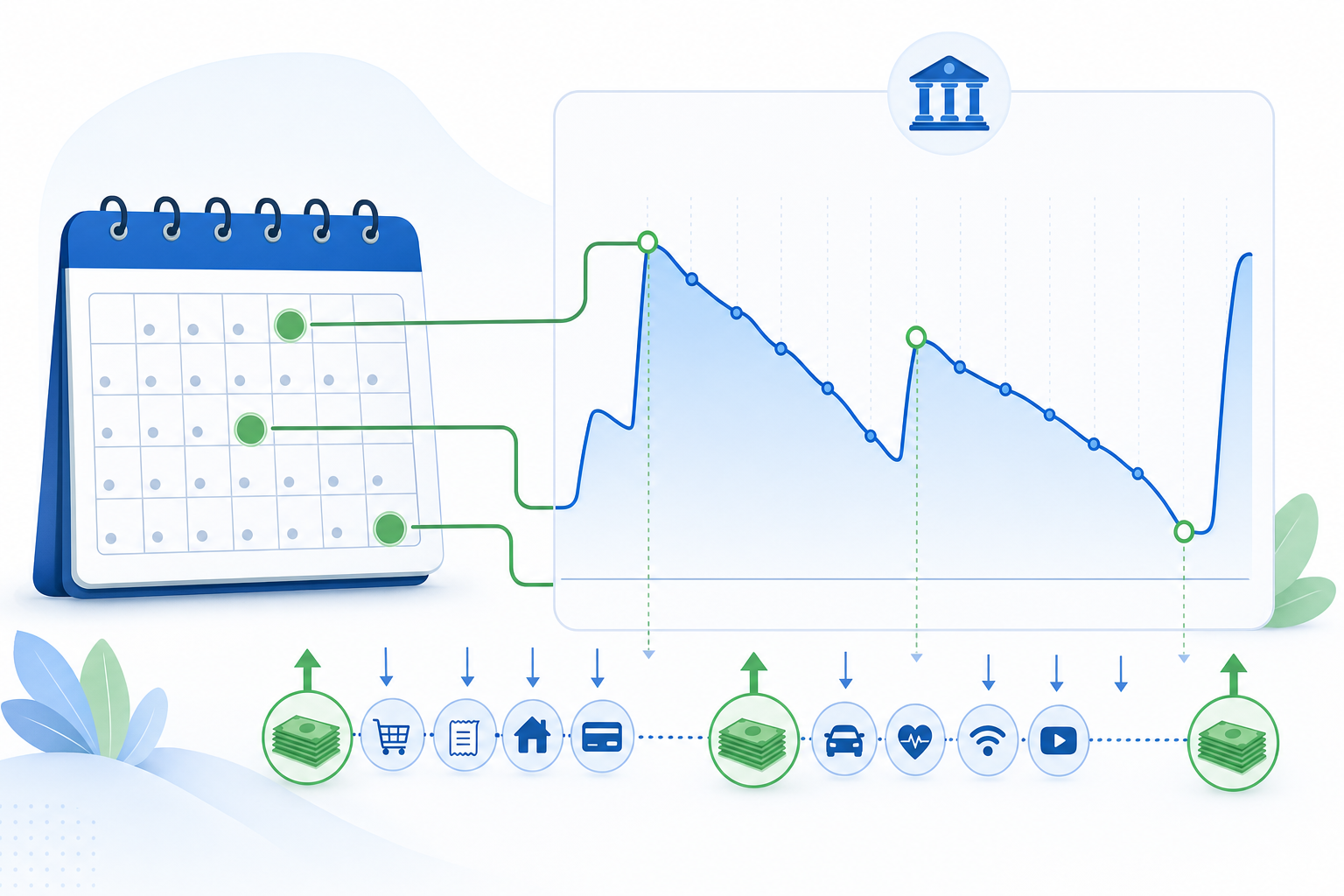

Paydays cluster heavily around the 1st, 15th, and last business day of each month. Billing runs that land two to four days before those dates catch accounts that haven't cleared yet, producing avoidable failures that a simple timing shift could prevent.

The Payday Window Effect

Recovery logic that accounts for payday proximity performs measurably better than fixed-interval retries. Retrying a soft decline three to five days after the original attempt, timed to land just after a common payday, increases the probability that funds are available without requiring any customer action.

- Insufficient funds declines are recoverable without customer contact in the majority of cases, making them a prime target for smart retry timing instead of dunning outreach.

- Payroll cycles vary by employer type: weekly for hourly workers, biweekly for salaried employees, and monthly for many public-sector and contract workers, so a single retry window won't fit every subscriber.

- Segmenting retry timing by subscriber cohort, where data allows, captures more recoveries than a uniform retry schedule applied across the entire billing run.

Connecting retry timing to real-world cash flow patterns is one of the clearest ways to lift payment success rates without touching the subscriber experience at all.

End-of-Month Payment Clustering and the Insufficient Funds Problem

Subscription payments cluster heavily at month-end. When rent, utilities, and loan repayments all hit within the same 72-hour window, available balances drop fast, and recurring billing charges run directly into that crunch.

The result is a predictable spike in insufficient funds declines every month. For subscription businesses processing high volumes, this pattern repeats reliably enough to plan around.

Retry logic that ignores this clustering tends to fail repeatedly on the same accounts. Spacing retries past the typical account-replenishment window, usually 2 to 4 days after a paycheck posts, recovers a measurable share of those soft declines without any customer contact required.

Bank Holidays and ACH Processing Delays

In the US, ACH transactions don't settle on federal holidays, which creates compounding delays for subscription businesses that process high volumes of recurring charges. When Memorial Day, Independence Day, or Labor Day falls mid-billing-cycle, a payment initiated the day before may not settle for two to three additional business days.

For subscription companies, this creates a false failure window. A charge that appears unresolved isn't necessarily declined; it's simply queued. Retry logic that fires too aggressively during this window can trigger duplicate charges or unnecessary dunning sequences, both of which damage subscriber trust.

The practical implication: your retry schedules need calendar awareness baked in, not bolted on.

Geographic Variations in Payday Timing and Payment Success

Payroll frequency varies widely by country. Deel's country-by-country pay comparison shows most European countries default to monthly pay cycles, while US employers skew biweekly. Russia legally mandates semi-monthly pay. The United Kingdom follows monthly cycles similar to continental Europe.

For subscription businesses serving international customers, the optimal retry window changes depending on where a subscriber lives. A retry timed three days after payday captures funds in Germany but lands at the wrong point in the cycle for a US subscriber paid every two weeks. CloudPay's global pay frequency data reinforces this: one retry schedule applied across geographies leaves recoverable revenue uncaptured every billing cycle.

Concrete retry windows by region:

- United States (biweekly): Retry 2 to 3 days after the 1st or 15th, and again 2 to 3 days after the midpoint between those dates, to catch both common payroll cadences.

- Western Europe and UK (monthly): Most employers pay on the last working day of the month. Retry within 48 hours of that date, then hold until the same window next month rather than retrying mid-cycle.

- Russia (semi-monthly): Labor law requires pay by the 15th and the last day of the month. Retry windows should bracket both dates, targeting the 2-day window following each.

- Australia (weekly or fortnightly): Broader pay frequency distribution means a short 3 to 5 day retry interval after the original decline catches most payroll cadences without waiting a full two-week cycle.

Optimal Retry Timing Strategies Based on Payment Patterns

Retry timing that ignores payroll cycles and bank holidays leaves recoverable revenue on the table. The core principle is simple: retry when your subscriber is most likely to have funds available.

Payday-Aligned Retry Windows

Most salaried subscribers see funds clear within 24 hours of their payroll date. Scheduling retries on common payday windows can lift success rates meaningfully compared to arbitrary retry intervals.

Bank Holiday Avoidance

Retrying on a bank holiday introduces settlement delays and issuer routing gaps. Queue those attempts for the next business day instead.

A Practical Timing Framework

For soft declines near a known payday, retry within 24 to 48 hours after funds typically clear. Mid-cycle soft declines perform better when retried at the next payday window instead of on an arbitrary fixed schedule. When a decline collides with a bank holiday, defer the attempt to the next business day to avoid settlement delays. Hard declines should skip retry logic entirely and route directly to dunning, since the underlying issue requires cardholder action.

Getting this timing right is the difference between a recovered payment and an involuntary churn event that costs you the full customer lifetime value.

Card Network Rules and Merchant Advice Codes for Retry Timing

Visa, Mastercard, American Express, and other major networks each publish retry rules that govern how and when merchants can resubmit declined transactions. Violating these rules risks fines and increased decline rates, so understanding them is foundational to any retry strategy.

Data-Driven Recovery: Measuring Timing Impact on Success Rates

Knowing when to retry matters. Knowing whether your timing choices are actually working matters more.

Four metrics are worth tracking directly:

- Recovery rate by retry attempt number (first vs. second vs. third), so you can see where diminishing returns set in for your specific subscriber base.

- Recovery rate by day of week and time of day, mapped against your actual payment volume, not industry averages.

- Days since initial failure versus recovery probability, which shows how quickly your window closes.

- Recovery rate by billing cycle position, separating mid-cycle failures from those clustered around payday or bank holiday windows.

Without this breakdown, you're applying timing logic that works on average across other businesses. Consumer debit behavior at a regional bank differs from corporate card patterns, and your subscriber geography skews the picture further. Measuring these dimensions directly is the only reliable way to know which timing windows actually convert for your base.

How Slicker Uses Payment Pattern Intelligence to Optimize Recovery Timing

Slicker's Artificial Payments Intelligence layer ingests payday calendars, bank holiday schedules, and issuer behavior patterns to decide exactly when each subscriber's payment attempt is most likely to succeed.

Instead of retrying on a fixed schedule, the AI models weigh over 40 variables per transaction: the subscriber's historical payment timing, their issuer's processing behavior around public holidays, regional payday calendar data, and whether their account typically receives funds on weekly or monthly pay cycles. The result is retry timing that bends around the real world instead of ignoring it.

For subscription businesses, the result is fewer failed payments on bank holiday Fridays and higher recovery rates in the days immediately following payday.

Final Thoughts on Optimizing Recurring Payment Timing

Retry timing that ignores when your subscribers actually receive their paychecks leaves money on the table every billing cycle. The practical fix is simpler than most finance teams expect: stop retrying on arbitrary schedules and start retrying when account balances are most likely to support the transaction. We can measure the revenue difference in an AABB test on your own subscriber base, so you'll know exactly how much timing intelligence is worth before changing anything permanently.

FAQ

What's the best way to retry failed payments automatically?

Align retry attempts with payday windows (1st, 15th, and last business day) and account for bank holiday delays. Retrying 24-48 hours after common payday dates when accounts are replenished recovers 10-15 percentage points more revenue than fixed-interval retries that ignore cash flow patterns.

Can you time retries around paydays without knowing each subscriber's pay schedule?

Yes. Retry timing aligns with statistically common payday windows (1st, 15th, and last business day of each month) without tracking individual pay schedules. For US subscribers, biweekly pay cycles mean retrying 3-5 days after the original decline often catches the next paycheck, while European monthly cycles require different timing windows mapped to regional norms.

How do bank holidays affect subscription payment success rates?

ACH transactions don't settle on federal holidays in the US, creating 2-3 day settlement delays for charges initiated before the holiday. This produces false-failure windows where a payment appears declined but is simply queued. Retrying aggressively during this period risks duplicate charges and unnecessary dunning outreach that damages subscriber trust.

What are Merchant Advice Codes and when should you follow them?

Merchant Advice Codes (MACs) are issuer instructions that accompany declines and specify retry permissions and timing (e.g., "retry after 72 hours" or "do not retry"). Following them prevents network penalties (Mastercard charges $0.10 per non-compliant retry) and preserves merchant reputation. However, strict MAC compliance can conflict with dunning windows, so intelligent systems balance network guidance against recovery deadlines to maximize actual revenue capture.

Should I segment retry timing by subscriber geography?

Yes. Pay frequency varies by country (US biweekly, most of Europe monthly, Russia semi-monthly), so a single retry schedule applied globally misses recoverable revenue. Retries timed for a US biweekly cycle land at the wrong point for German monthly subscribers, leaving soft declines unrecovered every billing cycle.

Related Articles

AI for Failed Payment Recovery in Subscription SaaS (July 2026)

I'll be frank: most of the failed payment recovery advice out there focuses on dunning, when the bigger win is usually in the retry logic that runs before a...

Failed Payment Recovery: Evaluating Categories and Vendors (July 2026)

Choosing failed payment recovery software gets complicated quickly. There are standalone retry engines, dunning tools, billing-native recovery, and full-stack...

Counter-Intuitive Truth: Stop Retries Earlier (July 2026)

Most billing teams treat more retries as a safer bet. Run the full sequence, exhaust every attempt, and at least you know you tried. But retry exhaustion has a...

Stop losing revenue to failed payments

Join leading subscription businesses using Slicker to recover failed payments automatically.

Get Started