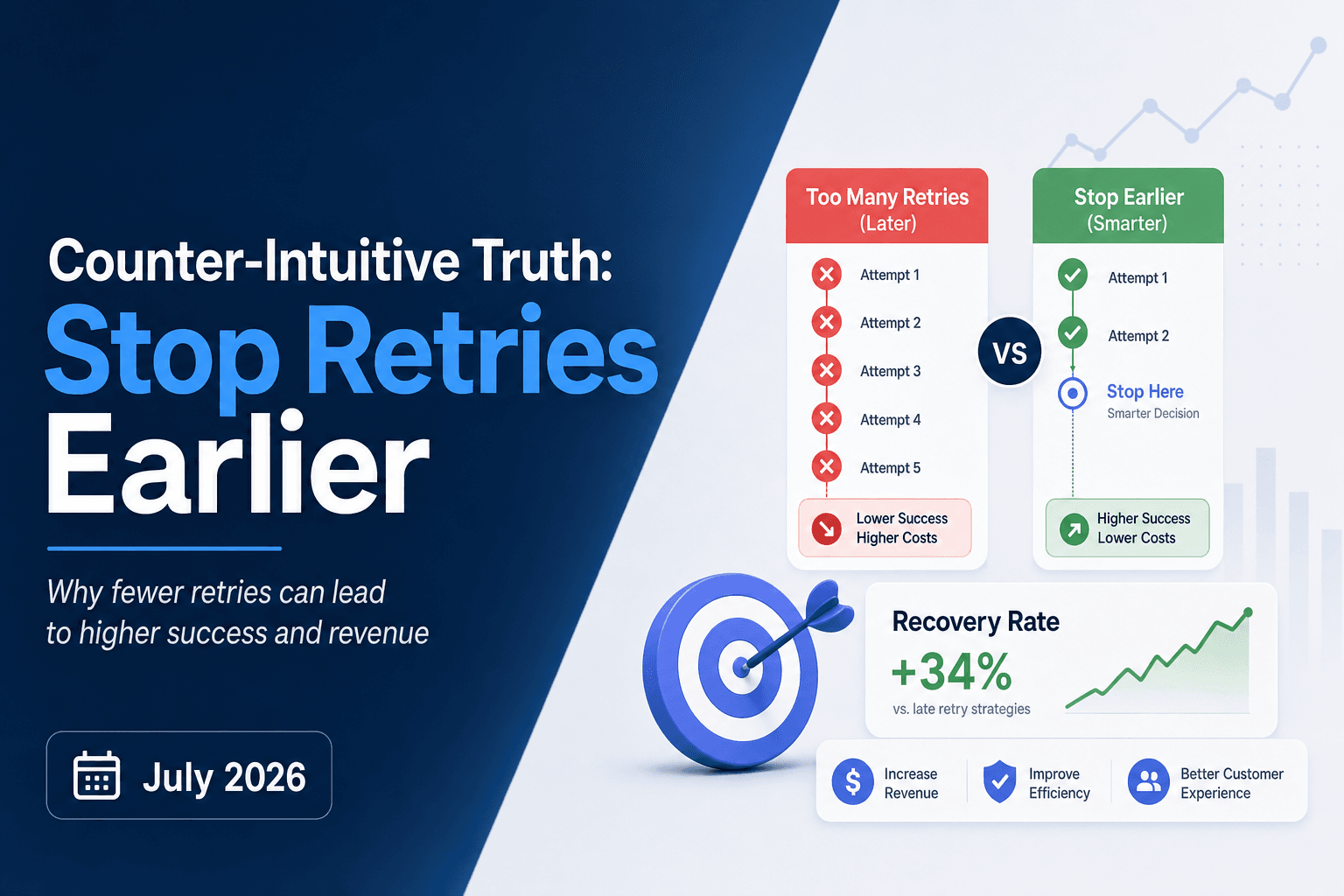

Counter-Intuitive Truth: Stop Retries Earlier (July 2026)

Most billing teams treat more retries as a safer bet. Run the full sequence, exhaust every attempt, and at least you know you tried. But retry exhaustion has a real cost that rarely shows up in the recovery report: eroded issuer standing, accumulated processing fees, and a merchant ID that gets quietly flagged for excessive retry behavior. Stopping payment retries early, before the recoverable window closes, is where the math actually works in your favor.

TLDR:

- Stop retrying after attempt 3 or 4; recovery likelihood drops sharply while issuer friction compounds.

- Hard declines (stolen card, closed account) warrant zero retries; soft declines warrant a finite window closing within 48 to 72 hours.

- Visa caps retries at 15 over 30 days with fines starting at $25 per violation; Mastercard charges after a single same-day retry failure.

- MAC codes 01, 03, and 21 are explicit issuer stop signals; burning retries against them erodes your merchant ID standing.

- Slicker halts retry sequences immediately on hard stop signals and reads issuer response patterns to stop soft-decline sequences earlier than fixed schedules allow.

Why Stopping Retries Early Outperforms Retrying to Exhaustion

Most retry logic is built around persistence. Keep trying until the card works or the account is flagged as unrecoverable. The intuition seems sound, but the math tells a different story.

Each failed retry after the optimal window carries a cost: issuer friction compounds, the customer's bank registers repeated declines, and your sender reputation with payment networks erodes quietly. By the time retry exhaustion hits, you've spent processing fees on attempts that had little chance of succeeding.

Where the Revenue Actually Leaks

Knowing when to stop retrying is just as valuable as knowing when to start. Issuers interpret repeated failed attempts as a signal that something is wrong, and that signal makes future approval less likely, not more.

The recoverable window for most soft declines closes within 48 to 72 hours of the initial failure. Attempts beyond that window see materially lower authorization rates, and the processing costs accumulate regardless of outcome.

Stopping early preserves issuer goodwill, reduces unnecessary spend, and frees the retry budget for accounts that fall into genuinely recoverable windows. That's not a philosophical position; it's where the dollars are.

Hard Declines vs. Soft Declines: The Classification That Drives Every Stop Decision

Not all declines carry the same signal, and misreading that signal is where retry exhaustion begins.

Hard declines are terminal. A stolen card, a closed account, a card flagged for fraud: the issuer has made a permanent decision. Retrying these transactions wastes processing attempts and, in some cases, triggers fraud alerts that put your merchant account at risk.

Soft declines are different. Insufficient funds, temporary holds, network timeouts: these are transient conditions where a well-timed retry has a real chance of recovery.

Why This Classification Is the Foundation of Every Stop Decision

Getting the category wrong in either direction has a cost:

- Retrying a hard decline repeatedly signals poor transaction hygiene to issuers, which can erode your authorization rates over time across your entire merchant account.

- Stopping too early on a soft decline means leaving recoverable revenue on the table from a customer who never intended to churn.

The classification also shapes how quickly you should stop. Hard declines warrant an immediate stop. Soft declines warrant a measured retry window, though still a finite one. A soft decline retry playbook spells out exactly when to retry and when to stop: issuers track attempt frequency, and repeated failures on the same card can cause the issuer to progressively downgrade how it scores future transactions from your merchant ID (MID).

Knowing which category you are dealing with is the prerequisite to knowing when stopping is the right business call.

Card Network Retry Limits: Where the Rules Force a Hard Stop

Card networks set hard retry limits that remove any guesswork about when to stop. The Visa and Mastercard payment retry rules cap merchants at a maximum of 15 retries over 30 days on a declined transaction. Exceed that, and you risk fines starting at $25 per violation.

Mastercard goes further. Their excessive retry fees apply after just a single same-day retry failure, a policy that makes late-stage retry exhaustion genuinely expensive.

These aren't soft guidelines. They're enforceable limits backed by real financial penalties:

- Retrying beyond network limits exposes you to per-transaction fines that compound quickly at high volume.

- Processors can flag your MID (Merchant ID) for excessive retry behavior, which can trigger additional review or account holds.

- The costs hit before you've recovered a single dollar more.

The networks, in effect, have already answered the "when to stop retrying" question for the worst cases. The smarter business question is why so many retry strategies wait until they're forced to stop, when cutting losses far sooner is the better move.

The Diminishing Returns of Extended Retry Windows

Each retry attempt after a failed payment carries a cost: processing fees, issuer scrutiny, and the gradual erosion of your account's standing with card networks. Most billing teams assume more retries equal more recoveries. The data tells a different story.

Recovery rates drop sharply after the first two or three attempts. By attempt four or five, you are spending real money to chase payments that issuers have already flagged. Worse, repeated declines on the same card can trigger fraud scoring at the issuer level, making future legitimate charges harder to process.

Where the Curve Breaks Down

The relationship between retry volume and recovery is not linear. Consider what happens across a typical retry window:

Attempt | Relative Recovery Likelihood | Risk Added |

|---|---|---|

1st | Highest | Minimal |

2nd | Moderate | Low |

3rd | Low | Moderate |

4th+ | Negligible | High |

Continuing past the point of diminishing returns wastes processing budget and signals retry exhaustion to issuers, which can suppress approval rates on future transactions across your entire merchant ID (MID). Knowing when to stop retrying is as consequential to your recovery rate as knowing when to start.

Merchant Advice Codes as Explicit Stop Signals

Mastercard Merchant Advice Codes (MACs) are among the clearest stop signals in the payments stack. When an issuer returns a MAC indicating a card has been reported stolen, the account is closed, or the customer has explicitly requested no further charges, continuing to retry is not persistence. It is wasted spend and potential compliance exposure.

These codes exist precisely so merchants know when to stop. A stolen card will not suddenly become valid on retry four. A closed account will not reopen.

The MAC Codes That Mean Stop Immediately

Not every decline code carries the same weight. Some signal a temporary state worth retrying; others are definitive. When you see the following, stop payment retries early:

- MAC 01 (New account information available): The card on file is no longer valid. Retry logic should pause and route to a card update flow instead.

- MAC 03 (Do Not Try Again): The issuer has flagged this transaction as unrecoverable. Mastercard imposes a $0.10 per-retry fee for every attempt made after receiving this code, so burning retries here compounds direct processing costs with zero recovery upside.

- MAC 21 (Stop Recurring Payment): The issuer has explicitly instructed the merchant to halt recurring charges on this account. Retrying wastes processing costs and risks flagging your merchant ID for non-compliance.

Burning retries against these codes does not recover revenue. It erodes your standing with issuers and accelerates the kind of decline-rate signal that leads to MID-level consequences.

What Retry Exhaustion Actually Costs Your Merchant Account

Retry exhaustion is a term most billing teams know abstractly, but few have priced out concretely. When a payment fails and your system runs through every scheduled retry attempt without success, the subscription lapses. That lost MRR is the obvious cost. What gets missed is what happens to your merchant account in the process.

Card networks track your retry volume against your success rate. Flood a declined card with too many attempts and your processor flags the pattern. Enough flags and you face higher interchange fees, reserve requirements, or in severe cases, MID (Merchant ID) termination. Stopping retries early, before exhaustion, is not pessimistic. It protects the account infrastructure every future payment runs through.

When Retrying Again Is Wrong and Dunning Is Right

Not every failed payment is a retry candidate. Some decline codes are the processor's way of telling you the retry window has already closed.

Hard declines like stolen card, invalid account, or "do not honor" flags with no retry advisory are permanent rejections. Retrying them wastes authorization attempts, burns through your processor's tolerance thresholds, and risks triggering fraud flags that can get your merchant account reviewed.

When the card itself is the problem, dunning is the faster path

If the underlying issue requires customer action, such as a card reported stolen or an expired number, no retry logic fixes that. The right call is an immediate, targeted dunning management message.

- Stolen or blocked cards need a payment method update, not another authorization attempt against a flagged account.

- Expired cards are a known state; a well-timed email before the next billing cycle recovers more than repeated declines ever will.

- Account closed codes are hard stops. Any retry here is wasted spend with zero recovery upside.

Stopping retries early in these cases is not giving up. It's redirecting effort to the channel that can actually recover the revenue.

A Stop-Retry Decision Framework

When every retry fires on a fixed schedule regardless of decline context, you burn issuer goodwill and accelerate account flagging. The real skill is knowing precisely when to stop.

Read the Decline Code First

Not all declines are equal. Some signal a retriable condition; others are a hard stop.

- Soft declines (insufficient funds, temporary hold) may resolve within days and are generally worth retrying with appropriate spacing.

- Hard declines (stolen card, account closed, do not honor) should trigger zero retries. Continuing anyway damages your merchant standing with the issuer.

- Merchant Advice Codes (MACs), where available, give explicit issuer guidance on whether and when to retry. Ignoring them is a compliance and revenue risk.

A Simple Decision Table

Decline Signal | Retry? | Max Attempts |

|---|---|---|

Insufficient funds (soft) | Yes | 2 to 3, spaced by days |

Temporary hold (soft) | Yes | 1 to 2 |

Do not honor (hard) | No | 0 |

Stolen / lost card (hard) | No | 0 |

Account closed (hard) | No | 0 |

MAC: Do not retry | No | 0 |

Stopping earlier on hard declines and MAC-flagged accounts protects your merchant ID and preserves the issuer relationship for recoverable failures down the line.

How Slicker Applies Early-Stop Logic in Practice

Slicker's retry logic is built around one guiding principle: a failed payment signal that clearly indicates no future attempt will succeed should stop the sequence immediately, not after a predetermined number of tries.

When a decline carries a hard stop signal (a stolen card flag, a do-not-retry instruction, or a confirmed account closure), Slicker halts the sequence on that transaction and redirects effort toward customer outreach where action is actually required. No further retries are queued. No processing fees accumulate on attempts that data already predicts will fail.

For soft declines, Slicker reads issuer response codes, timing signals, and account-level patterns before scheduling the next attempt. If the pattern suggests the account is deteriorating instead of facing a temporary condition, the sequence stops earlier than a fixed schedule would allow.

The result is a retry budget spent only on transactions where recovery remains statistically plausible, which translates directly into lower processing costs and higher recovered revenue per attempt.

Final Thoughts on Stopping Payment Retries at the Right Time

The cost of retry exhaustion shows up in processing fees, issuer friction, and a quietly eroding MID reputation long before it shows up in your MRR report. Hard declines, Merchant Advice Codes, and network retry limits all exist to tell you when to stop. Listening to those signals early is what keeps your retry budget working for you. Talk to the Slicker team to see how early-stop logic fits your billing setup.

FAQ

When should you stop payment retries early instead of running to exhaustion?

Stop retries early whenever decline signals confirm no future attempt will succeed. Hard declines (stolen cards, closed accounts, fraud flags) warrant an immediate stop; soft declines (insufficient funds, temporary holds) warrant a finite retry window of two to three attempts spaced by days. Running to exhaustion on either category erodes your merchant ID standing with issuers and compounds processing costs without recovering additional revenue.

What do Merchant Advice Codes like MAC 21 actually tell you about when to stop retrying?

MAC 21 ("Stop Recurring Payment") is an explicit issuer instruction to halt recurring charges on the account; continuing to retry risks flagging your merchant ID and accumulates processing fees with zero recovery upside. MAC 01 signals the card on file is no longer valid and should route to a card update flow instead of another authorization attempt. Slicker treats these codes as definitive hard stops, halting retry sequences immediately and redirecting to targeted dunning where customer action can actually resolve the failure.

How does retry exhaustion damage your merchant account beyond the lost subscription revenue?

Card networks track your retry volume against your success rate, and repeated failed attempts on the same card can trigger fraud scoring at the issuer level, making future legitimate charges harder to approve across your entire merchant ID. Visa caps retries at 15 attempts over 30 days per declined transaction; Mastercard imposes excessive retry fees after a single same-day retry failure. The account-standing damage accumulates before you recover a single additional dollar, making early stops a direct protection of the payment infrastructure every future charge runs through.

Can I build a stop-retry decision framework without hard-coding fixed attempt counts?

Yes. The foundation is decline classification: soft declines get two to three spaced attempts, hard declines get zero, and Merchant Advice Codes where present override both defaults. Slicker reads issuer response codes, MAC guidance, and account-level patterns per individual transaction instead of applying a fixed schedule across all failures, stopping sequences earlier when signals indicate the account is deteriorating and not temporarily held up.

When should dunning replace retries entirely for a failed payment?

Switch to dunning immediately when the underlying failure requires customer action that retry logic cannot resolve. Stolen or blocked cards need a payment method update; expired cards need replacement details before the next billing cycle; closed account codes are hard stops with no retry upside. Routing these failures to targeted, failure-specific dunning outreach recovers more revenue than burning authorization attempts against a card the issuer has already permanently rejected.

Related Articles

AI for Failed Payment Recovery in Subscription SaaS (July 2026)

I'll be frank: most of the failed payment recovery advice out there focuses on dunning, when the bigger win is usually in the retry logic that runs before a...

Failed Payment Recovery: Evaluating Categories and Vendors (July 2026)

Choosing failed payment recovery software gets complicated quickly. There are standalone retry engines, dunning tools, billing-native recovery, and full-stack...

What Differs Between Built-In and Add-On Retry Tools July 2026

Failed payments are not a billing problem. They're a revenue problem, and the auto retry tools you're using right now are either closing that gap or quietly...

Stop losing revenue to failed payments

Join leading subscription businesses using Slicker to recover failed payments automatically.

Get Started